MGF: There Is A Time To Buy And There Is A Time To Hold (Rating Downgrade)

Zolak

Thesis

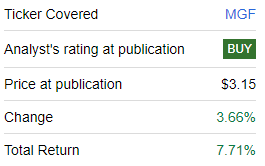

We last covered the MFS Government Markets Income (NYSE:MGF) at the beginning of 2024, when we highlighted the benefits of the fund despite its unsupported yield. The name is a closed end fund that focuses on fixed income.

In our original piece, we were of the opinion retail investors should buy MGF as an NAV accreting play given the outlook for interest rates. The CEF has healthily delivered since:

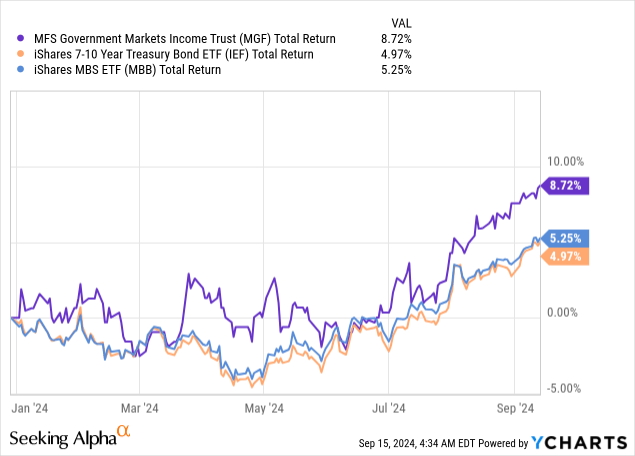

Performance (Seeking Alpha)

The fund has delivered a total return in excess of 7% since our rating, mainly driven by the shift lower in the yield curve in the past few months.

In today's article, we are going to revisit MGF, its risk factors and composition, and outline why we do not believe the name offers an attractive entry point anymore.

Robust performance in 2024

The entire suite of products in the IG / Treasury space has exhibited a robust performance in 2024:

An investor can clearly see from the above chart when rates started moving lower in 2024: the June-July period is when all the total return charts started to move robustly higher, and coincides with the market pricing in the first Fed rate cut. As we stated in our original piece, MGF is a play on treasuries and Agency MBS bonds, thus represents a turbo-charged version of the iShares 7-10 Year Treasury Bond ETF (IEF) and iShares MBS ETF (MBB). All three names are up in 2024, but MGF has posted almost double the total returns here.

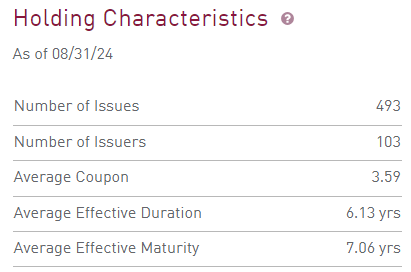

Duration-driven NAV accretion

Despite the low 3.59% coupon of the underlying holdings, the fund has a 6.13 years duration, which has driven gains:

Characteristics (Fund Website)

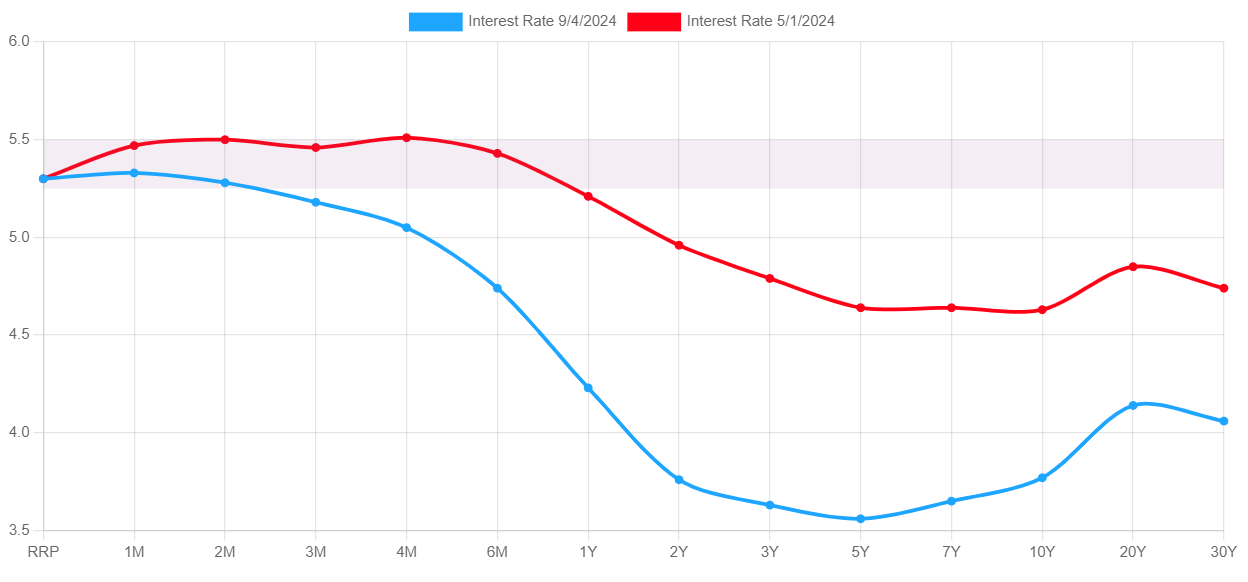

A 6-year duration means that for every 100 bps narrowing in rates, the fund gains +6% in its NAV. This year has seen a significant contraction in intermediate rates:

Yield Curve (UsTreasuryYieldCurve)

The 6-year tenor point in the yield curve has moved lower by more than 100 bps, accounting for the vast majority of gains in the CEF. If the curve remains fairly stable for this duration point going forward, the fund will end up just clipping the yield of the underlying holdings, with some smaller gains from an active management possible. The point to take home for a retail investor is that MGF was a rates play rather than a dividend play, and with the bulk of the curve move now behind us, and investors should hold this fund rather than buy it.

While we acknowledge that further gain are possible down the road if the yield curve shifts even lower, we are of the belief the market has priced in a very aggressive rate cut scenario, and there is scope for disappointment if the Fed is not as hawkish as expected.

Collateral composition - overweight Treasuries and MBS

The CEF has remained a rates play via its collateral composition, which is overweight Treasuries and MBS bonds:

- Treasuries: 64% of holdings

- Mortgage Backed: 44% of holdings

- IG bonds: 8%

- Others: 10%

- Short positions: -26%

Please note, the CEF takes a very active approach to its composition, using futures and other derivatives in making shorter term plays on the shape of the yield curve and its moves. Currently, it has large positions in 2Y / 5Y and 10Y treasury futures.

However, the main point to take away for a retail investor is the fact that the CEF is a rates play. Only IG bonds have a credit component, with treasuries and Agency MBS bonds representing pure rates plays. Therefore, the fund will be driven by moves in interest rates mostly.

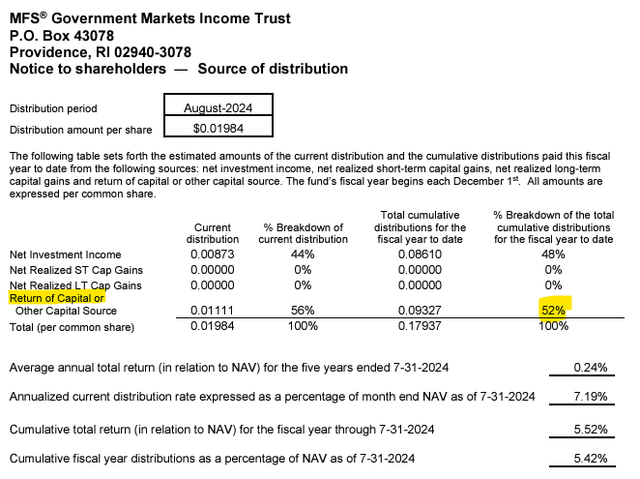

Distribution is not supported

As we have seen from the above analysis, the weighted average coupon of the underlying holdings is only 3.6%. However, the fund has a 7.4% current distribution rate. Where is the difference coming from? You guessed it, from return of capital:

Section 19a (Fund Website)

As of the August 2024 payment date, over 50% of the distribution came from ROC, which checks out with the simple math performed above. The fund does not run leverage, but takes active positions via futures. Expect a distribution which is more or less in line with its cash flow from underlying assets, with the rest made up in ROC. It is unfortunate the fund chooses to use such a high ROC figure, but the name is appealing during an easing cycle given its active approach to the markets.

What is next for MGF?

The CEF will perform in a tightening rates environment as the Fed eases rates. However, please keep in mind that nothing is linear, and we are of the opinion the bulk of the move in yield curves is now behind us for this stage of the cycle. The yield curve is pricing intermediate rates at 3.5% now, and with the Fed neutral rate at 2.75%, the term premium theory states that we are at fair value. A sudden spike in unemployment and the possibility of a recession can narrow rates even further, but we feel these are items reserved for 2025. For now, we are of the opinion that most of the NAV accretion for the year is behind us, and holders will just get dividends for the next few months. 2025 might be a different story, but we might see a slight reversal here first in rates. We are therefore downgrading the name to 'Hold' from 'Buy' given the move already embedded in the pricing.

Conclusion

MGF is a fixed income CEF. The fund is overweight treasuries and MBS bonds with an intermediate duration of 6 years. Although the fund does not run outright leverage, the name uses futures to take shorter-term positions, thus providing for a very active management and additional return potential. The CEF is up over 7% since our buy rating, helped by the significant narrowing in intermediate rates in the past few months. With most of the curve move now behind us, we see only limited upside for the rest of the year in the CEF, with the potential for a slight reversal. We are therefore downgrading the name to a 'Hold'.

免責聲明:投資有風險,本文並非投資建議,以上內容不應被視為任何金融產品的購買或出售要約、建議或邀請,作者或其他用戶的任何相關討論、評論或帖子也不應被視為此類內容。本文僅供一般參考,不考慮您的個人投資目標、財務狀況或需求。TTM對信息的準確性和完整性不承擔任何責任或保證,投資者應自行研究並在投資前尋求專業建議。

熱議股票

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10