3 SEHK Dividend Stocks Yielding Up To 9.4%

The Hong Kong market has recently faced challenges, with the Hang Seng Index experiencing a notable decline amid concerns about Beijing's stimulus measures and global economic uncertainties. In this environment, dividend stocks can offer investors a measure of stability and income potential, making them an attractive option for those looking to navigate turbulent markets.

Top 10 Dividend Stocks In Hong Kong

| Name | Dividend Yield | Dividend Rating |

| China Hongqiao Group (SEHK:1378) | 8.73% | ★★★★★☆ |

| Chongqing Rural Commercial Bank (SEHK:3618) | 7.01% | ★★★★★☆ |

| Chow Tai Fook Jewellery Group (SEHK:1929) | 7.99% | ★★★★★☆ |

| Bank of China (SEHK:3988) | 7.00% | ★★★★★☆ |

| Playmates Toys (SEHK:869) | 8.70% | ★★★★★☆ |

| China Construction Bank (SEHK:939) | 7.18% | ★★★★★☆ |

| PC Partner Group (SEHK:1263) | 9.20% | ★★★★★☆ |

| Tianjin Development Holdings (SEHK:882) | 7.03% | ★★★★★☆ |

| Sinopharm Group (SEHK:1099) | 4.82% | ★★★★★☆ |

| China Electronics Huada Technology (SEHK:85) | 8.54% | ★★★★★☆ |

Click here to see the full list of 92 stocks from our Top SEHK Dividend Stocks screener.

Here we highlight a subset of our preferred stocks from the screener.

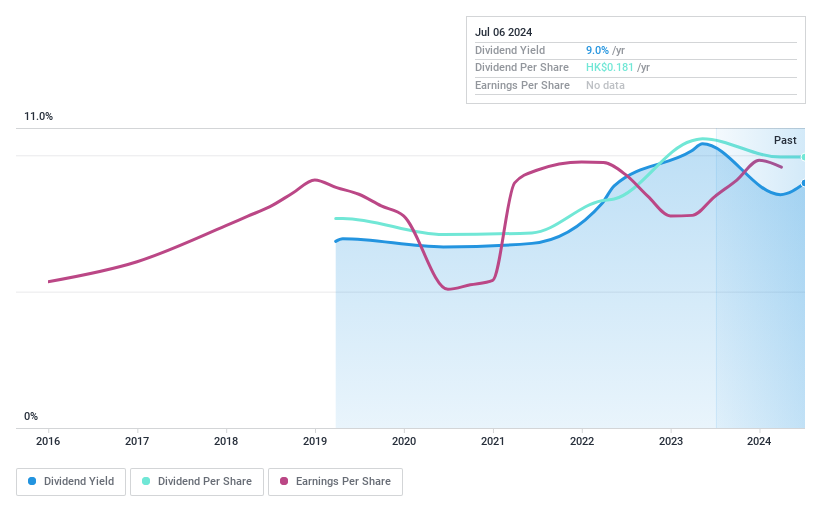

Lion Rock Group (SEHK:1127)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: Lion Rock Group Limited is an investment holding company offering printing services to international book publishers and media companies, with a market cap of HK$1.06 billion.

Operations: Lion Rock Group Limited generates revenue through its Printing segment, which accounts for HK$1.84 billion, and its Publishing segment, contributing HK$931.82 million.

Dividend Yield: 8%

Lion Rock Group's dividend profile shows a mixed picture. Despite an unstable track record, the company declared a special dividend of HK$0.015 and an interim dividend of HK$0.03 per share for the first half of 2024, supported by earnings growth to HK$79.1 million on sales of HK$1.26 billion. The dividends are well-covered by both earnings (payout ratio: 42.5%) and cash flows (cash payout ratio: 38.7%), but past volatility in payments raises reliability concerns for investors seeking stable income streams.

- Get an in-depth perspective on Lion Rock Group's performance by reading our dividend report here.

- Our valuation report here indicates Lion Rock Group may be undervalued.

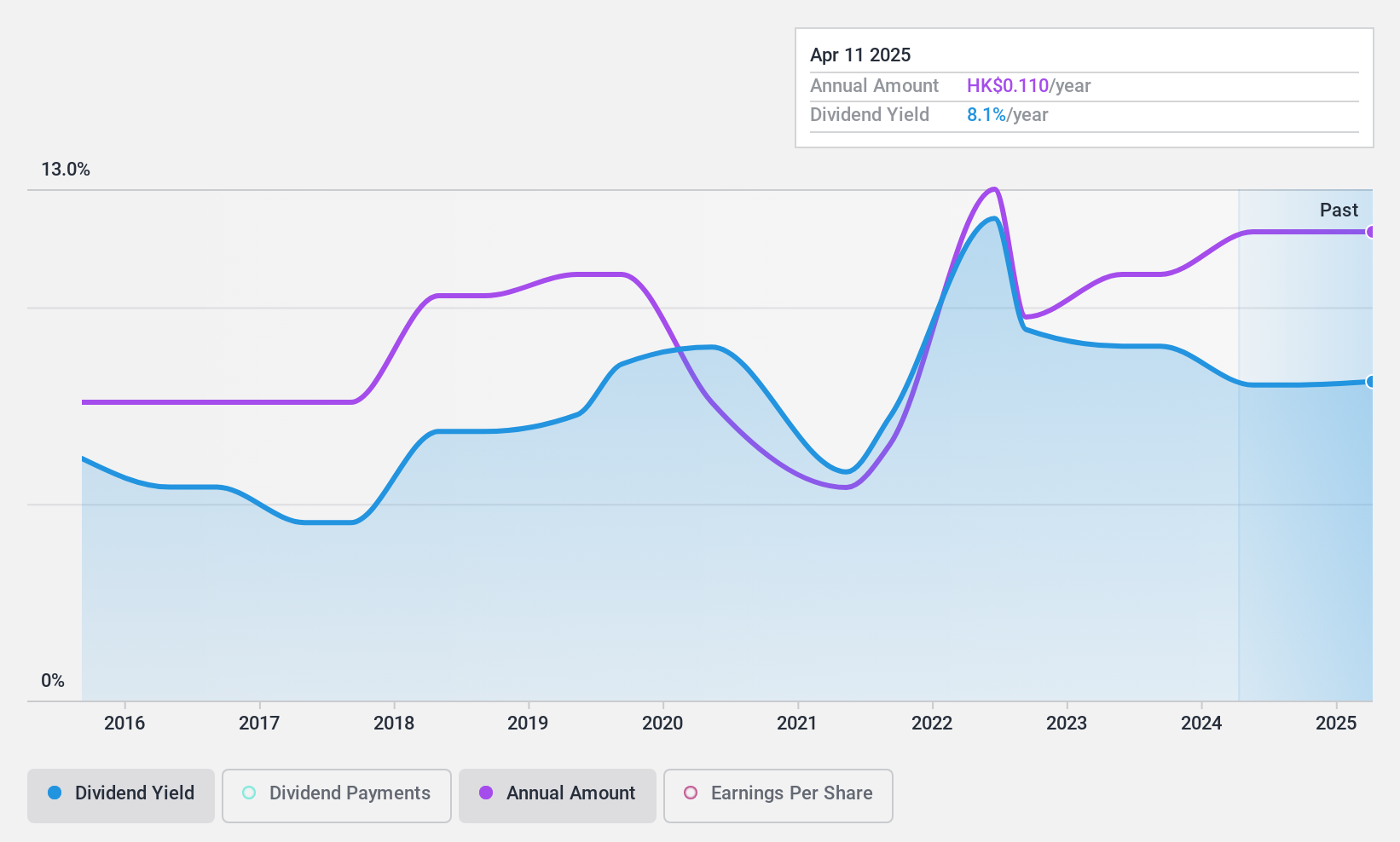

Chengdu Expressway (SEHK:1785)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: Chengdu Expressway Co., Ltd. focuses on the development, operation, and management of expressways in Chengdu, Sichuan province, China, with a market cap of HK$3.74 billion.

Operations: Chengdu Expressway Co., Ltd. generates revenue primarily from its expressway operations (CN¥1.59 billion) and energy segment (CN¥1.32 billion).

Dividend Yield: 8.1%

Chengdu Expressway's dividend profile is supported by a solid earnings coverage, with a payout ratio of 47.1% and cash payout ratio of 31.9%, indicating dividends are well-covered by both earnings and cash flows. Despite only six years of dividend history, payments have been stable, though the track record remains short for some investors. Recent half-year results show sales at CNY 1.41 billion and net income at CNY 291.3 million, reflecting slight declines in profitability compared to the previous year.

- Click here and access our complete dividend analysis report to understand the dynamics of Chengdu Expressway.

- Insights from our recent valuation report point to the potential undervaluation of Chengdu Expressway shares in the market.

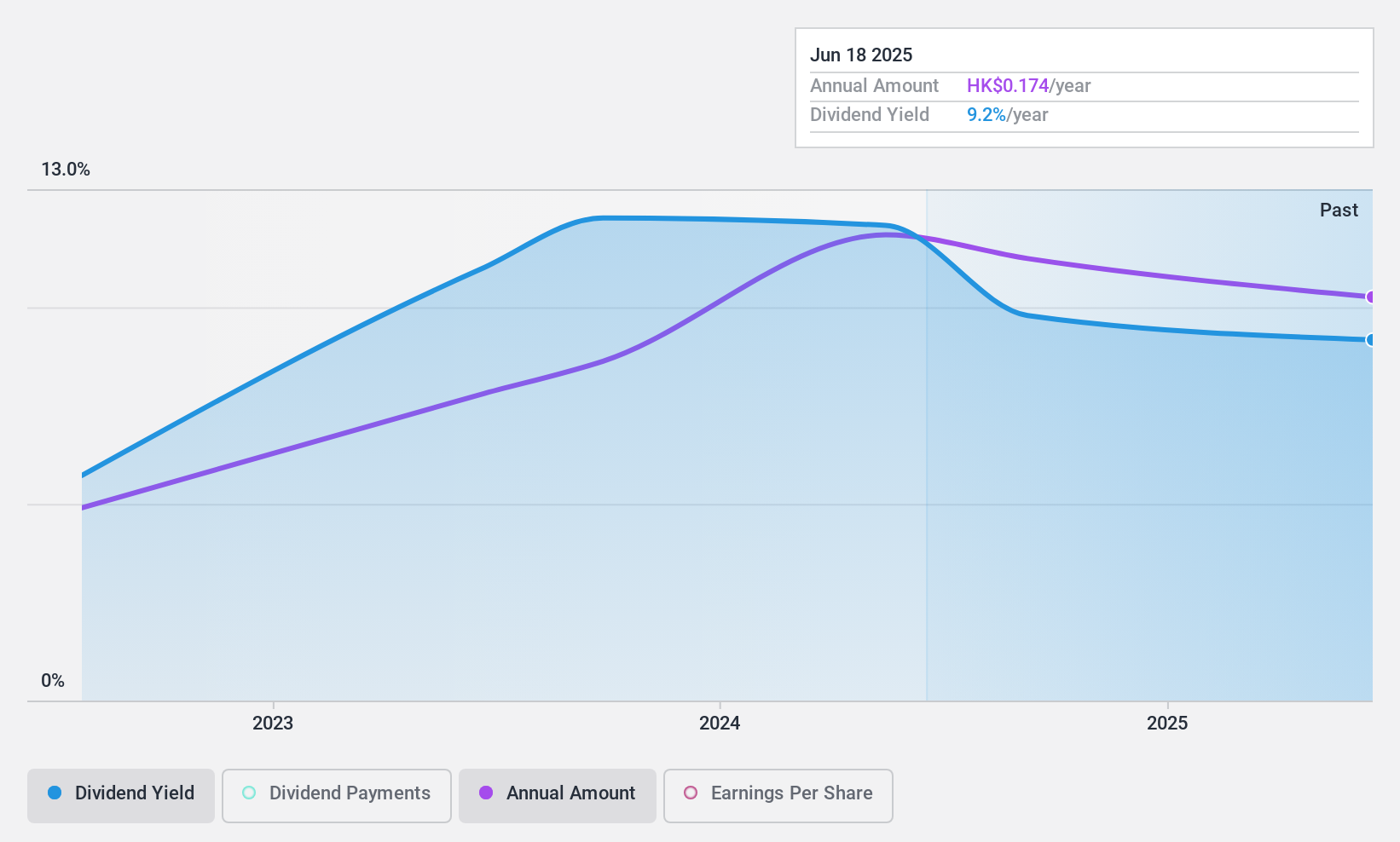

New Hope Service Holdings (SEHK:3658)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: New Hope Service Holdings Limited offers property management, value-added services, commercial operations, and lifestyle services with a market cap of HK$1.61 billion.

Operations: New Hope Service Holdings Limited generates revenue from four main segments: Lifestyle Services (CN¥325.85 million), Property Management Services (CN¥734.92 million), Commercial Operational Services (CN¥146.34 million), and Value-Added Services to Non-Property Owners (CN¥162.85 million).

Dividend Yield: 9.5%

New Hope Service Holdings recently announced an interim dividend of HK$0.09 per share, maintaining a stable payout despite a short dividend history. With earnings and cash flow coverage ratios both at 63.3%, the dividends are well-supported financially. The company's dividend yield is among the top 25% in Hong Kong, though it has only been paying dividends for three years. Recent half-year results showed sales growth to CNY 709.02 million and net income improvement to CNY 118.14 million, indicating solid financial performance underpinning its dividend strategy.

- Navigate through the intricacies of New Hope Service Holdings with our comprehensive dividend report here.

- According our valuation report, there's an indication that New Hope Service Holdings' share price might be on the cheaper side.

Seize The Opportunity

- Unlock our comprehensive list of 92 Top SEHK Dividend Stocks by clicking here.

- Got skin in the game with these stocks? Elevate how you manage them by using Simply Wall St's portfolio, where intuitive tools await to help optimize your investment outcomes.

- Simply Wall St is your key to unlocking global market trends, a free user-friendly app for forward-thinking investors.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if New Hope Service Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

免責聲明:投資有風險,本文並非投資建議,以上內容不應被視為任何金融產品的購買或出售要約、建議或邀請,作者或其他用戶的任何相關討論、評論或帖子也不應被視為此類內容。本文僅供一般參考,不考慮您的個人投資目標、財務狀況或需求。TTM對信息的準確性和完整性不承擔任何責任或保證,投資者應自行研究並在投資前尋求專業建議。

熱議股票

沒有相關數據