PostNL And 2 Other Promising Penny Stocks For Your Watchlist

As global markets navigate a complex landscape of mixed index performances and geopolitical developments, investors are increasingly exploring diverse opportunities. Penny stocks, despite their somewhat outdated moniker, continue to captivate attention due to their potential for growth and affordability. These smaller or newer companies can offer intriguing prospects when they exhibit financial resilience, making them worthy of consideration in today's market climate.

Top 10 Penny Stocks

| Name | Share Price | Market Cap | Financial Health Rating |

| DXN Holdings Bhd (KLSE:DXN) | MYR0.51 | MYR2.54B | ★★★★★★ |

| Embark Early Education (ASX:EVO) | A$0.765 | A$140.36M | ★★★★☆☆ |

| Datasonic Group Berhad (KLSE:DSONIC) | MYR0.43 | MYR1.2B | ★★★★★★ |

| Hil Industries Berhad (KLSE:HIL) | MYR0.885 | MYR293.77M | ★★★★★★ |

| ME Group International (LSE:MEGP) | £2.145 | £808.16M | ★★★★★★ |

| Bosideng International Holdings (SEHK:3998) | HK$4.14 | HK$45.59B | ★★★★★★ |

| LaserBond (ASX:LBL) | A$0.55 | A$64.47M | ★★★★★★ |

| Begbies Traynor Group (AIM:BEG) | £1.01 | £159.32M | ★★★★★★ |

| Lever Style (SEHK:1346) | HK$0.87 | HK$539.57M | ★★★★★★ |

| Secure Trust Bank (LSE:STB) | £3.58 | £68.28M | ★★★★☆☆ |

Click here to see the full list of 5,707 stocks from our Penny Stocks screener.

We'll examine a selection from our screener results.

PostNL (ENXTAM:PNL)

Simply Wall St Financial Health Rating: ★★★★☆☆

Overview: PostNL N.V. offers postal and logistics services to businesses and consumers across the Netherlands, Europe, and internationally, with a market cap of €527.22 million.

Operations: PostNL N.V. has not reported specific revenue segments.

Market Cap: €527.22M

PostNL N.V. recently reported a net loss of €21 million for Q3 2024, despite sales growth to €753 million from the previous year. Although earnings have declined by an average of 42.2% annually over the past five years, PostNL has become profitable in the last year, complicating comparisons with historical performance. The company trades significantly below its estimated fair value and has improved its financial position from negative shareholder equity five years ago to positive now. However, it carries a high debt level with short-term assets not fully covering short-term liabilities, while long-term liabilities are adequately covered.

- Unlock comprehensive insights into our analysis of PostNL stock in this financial health report.

- Gain insights into PostNL's outlook and expected performance with our report on the company's earnings estimates.

Atlas Consolidated Mining and Development (PSE:AT)

Simply Wall St Financial Health Rating: ★★★★☆☆

Overview: Atlas Consolidated Mining and Development Corporation, with a market cap of ₱15.12 billion, operates in the Philippines through its subsidiaries focusing on the exploration and mining of metallic mineral properties.

Operations: The company generates revenue of ₱19.65 billion from its operations in the Philippines.

Market Cap: ₱15.12B

Atlas Consolidated Mining and Development Corporation has shown robust earnings growth of 33% over the past year, surpassing both its industry peers and its own five-year average. The company's debt management is commendable, with a reduced debt-to-equity ratio from 95.7% to 35.6% in five years and satisfactory net debt coverage by operating cash flow. Despite these strengths, Atlas reported a Q3 net loss of ₱939.32 million due to short-term asset insufficiencies against liabilities and low return on equity at 2.9%. Nevertheless, it remains undervalued relative to fair value estimates with stable weekly volatility.

- Get an in-depth perspective on Atlas Consolidated Mining and Development's performance by reading our balance sheet health report here.

- Understand Atlas Consolidated Mining and Development's track record by examining our performance history report.

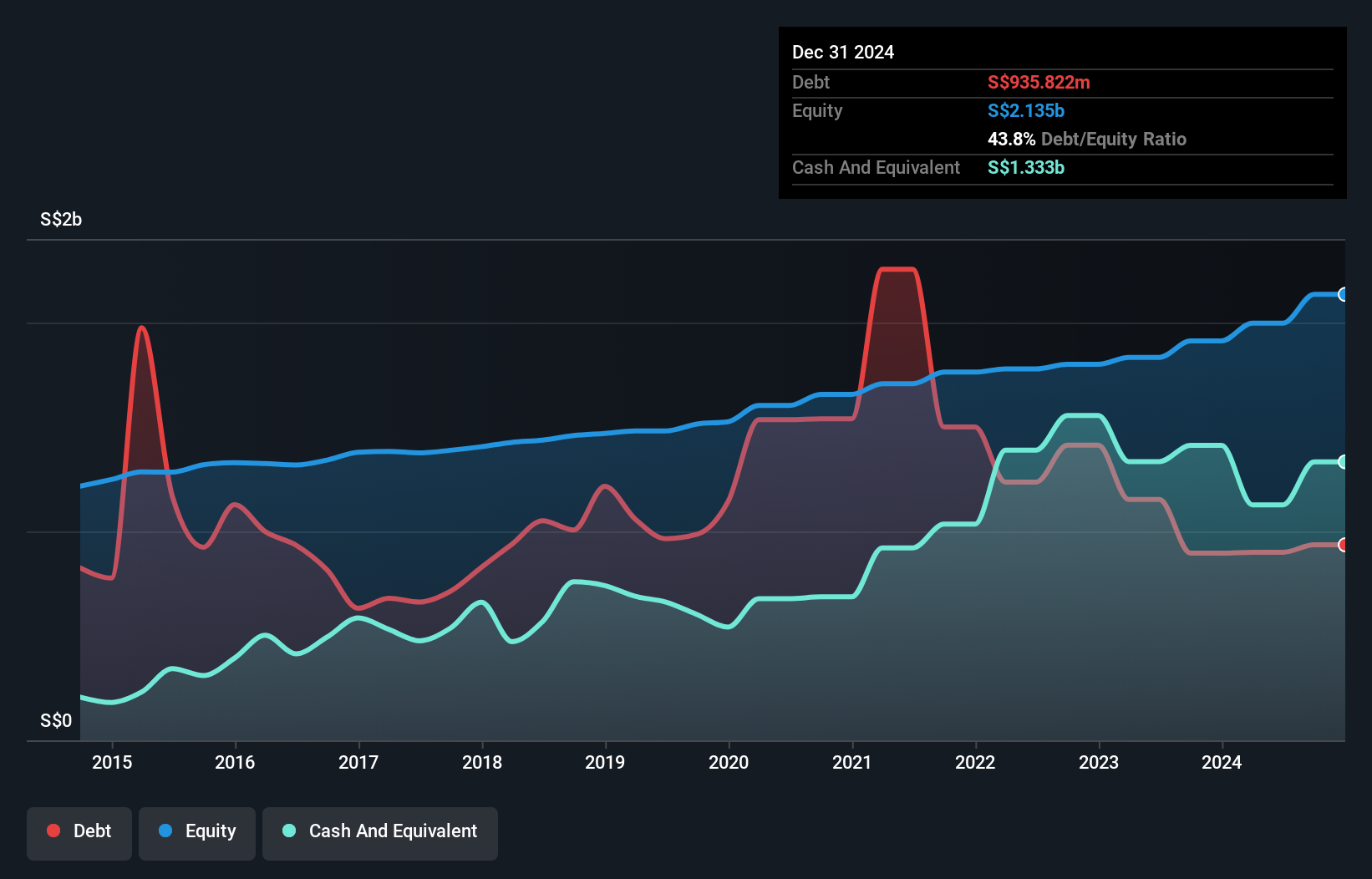

UOB-Kay Hian Holdings (SGX:U10)

Simply Wall St Financial Health Rating: ★★★★☆☆

Overview: UOB-Kay Hian Holdings Limited is an investment holding company offering stockbroking, futures broking, structured lending, investment trading, margin financing, and nominee and research services across Singapore, Hong Kong, Thailand, Malaysia and internationally with a market cap of SGD1.57 billion.

Operations: The company generates SGD581.07 million in revenue from its securities and futures broking and related services.

Market Cap: SGD1.57B

UOB-Kay Hian Holdings Limited has demonstrated significant earnings growth of 80% over the past year, outpacing the industry average. The company's short-term assets substantially cover both its short and long-term liabilities, indicating strong liquidity. It trades at a discount to estimated fair value, suggesting potential undervaluation. However, its dividend coverage by free cash flow is weak, and recent shareholder dilution may concern investors. While debt levels are manageable with more cash than total debt, interest payment coverage by EBIT remains unclear due to insufficient data. Management's lack of experience could pose operational challenges moving forward.

- Click here to discover the nuances of UOB-Kay Hian Holdings with our detailed analytical financial health report.

- Gain insights into UOB-Kay Hian Holdings' past trends and performance with our report on the company's historical track record.

Key Takeaways

- Embark on your investment journey to our 5,707 Penny Stocks selection here.

- Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

- Streamline your investment strategy with Simply Wall St's app for free and benefit from extensive research on stocks across all corners of the world.

Ready To Venture Into Other Investment Styles?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Jump on the AI train with fast growing tech companies forging a new era of innovation.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)• Undervalued Small Caps with Insider Buying• High growth Tech and AI CompaniesOr build your own from over 50 metrics.

Explore Now for FreeHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

免責聲明:投資有風險,本文並非投資建議,以上內容不應被視為任何金融產品的購買或出售要約、建議或邀請,作者或其他用戶的任何相關討論、評論或帖子也不應被視為此類內容。本文僅供一般參考,不考慮您的個人投資目標、財務狀況或需求。TTM對信息的準確性和完整性不承擔任何責任或保證,投資者應自行研究並在投資前尋求專業建議。

熱議股票

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10