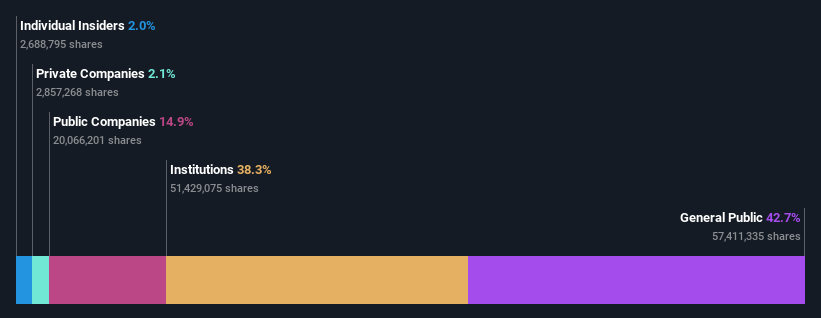

retail investors who own 43% along with institutions invested in Baby Bunting Group Limited (ASX:BBN) saw increase in their holdings value last week

Key Insights

- Baby Bunting Group's significant retail investors ownership suggests that the key decisions are influenced by shareholders from the larger public

- The top 8 shareholders own 50% of the company

- 38% of Baby Bunting Group is held by Institutions

To get a sense of who is truly in control of Baby Bunting Group Limited (ASX:BBN), it is important to understand the ownership structure of the business. With 43% stake, retail investors possess the maximum shares in the company. Put another way, the group faces the maximum upside potential (or downside risk).

While retail investors were the group that benefitted the most from last week’s AU$24m market cap gain, institutions too had a 38% share in those profits.

Let's take a closer look to see what the different types of shareholders can tell us about Baby Bunting Group.

View our latest analysis for Baby Bunting Group

What Does The Institutional Ownership Tell Us About Baby Bunting Group?

Institutional investors commonly compare their own returns to the returns of a commonly followed index. So they generally do consider buying larger companies that are included in the relevant benchmark index.

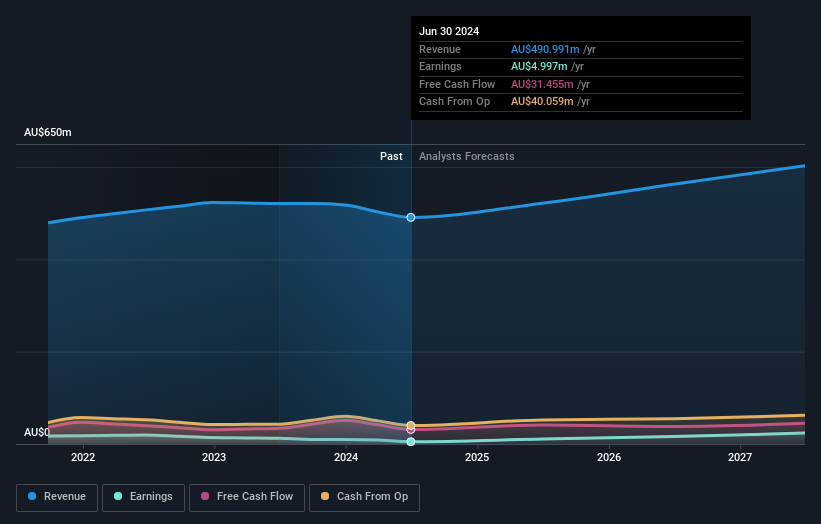

As you can see, institutional investors have a fair amount of stake in Baby Bunting Group. This implies the analysts working for those institutions have looked at the stock and they like it. But just like anyone else, they could be wrong. It is not uncommon to see a big share price drop if two large institutional investors try to sell out of a stock at the same time. So it is worth checking the past earnings trajectory of Baby Bunting Group, (below). Of course, keep in mind that there are other factors to consider, too.

Baby Bunting Group is not owned by hedge funds. HMC Capital Limited is currently the largest shareholder, with 15% of shares outstanding. In comparison, the second and third largest shareholders hold about 13% and 6.1% of the stock.

On further inspection, we found that more than half the company's shares are owned by the top 8 shareholders, suggesting that the interests of the larger shareholders are balanced out to an extent by the smaller ones.

Researching institutional ownership is a good way to gauge and filter a stock's expected performance. The same can be achieved by studying analyst sentiments. Quite a few analysts cover the stock, so you could look into forecast growth quite easily.

Insider Ownership Of Baby Bunting Group

The definition of an insider can differ slightly between different countries, but members of the board of directors always count. The company management answer to the board and the latter should represent the interests of shareholders. Notably, sometimes top-level managers are on the board themselves.

Most consider insider ownership a positive because it can indicate the board is well aligned with other shareholders. However, on some occasions too much power is concentrated within this group.

We can see that insiders own shares in Baby Bunting Group Limited. As individuals, the insiders collectively own AU$4.8m worth of the AU$242m company. It is good to see some investment by insiders, but we usually like to see higher insider holdings. It might be worth checking if those insiders have been buying.

General Public Ownership

The general public-- including retail investors -- own 43% stake in the company, and hence can't easily be ignored. While this group can't necessarily call the shots, it can certainly have a real influence on how the company is run.

Public Company Ownership

It appears to us that public companies own 15% of Baby Bunting Group. This may be a strategic interest and the two companies may have related business interests. It could be that they have de-merged. This holding is probably worth investigating further.

Next Steps:

While it is well worth considering the different groups that own a company, there are other factors that are even more important. Be aware that Baby Bunting Group is showing 1 warning sign in our investment analysis , you should know about...

If you are like me, you may want to think about whether this company will grow or shrink. Luckily, you can check this free report showing analyst forecasts for its future.

NB: Figures in this article are calculated using data from the last twelve months, which refer to the 12-month period ending on the last date of the month the financial statement is dated. This may not be consistent with full year annual report figures.

Valuation is complex, but we're here to simplify it.

Discover if Baby Bunting Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

免責聲明:投資有風險,本文並非投資建議,以上內容不應被視為任何金融產品的購買或出售要約、建議或邀請,作者或其他用戶的任何相關討論、評論或帖子也不應被視為此類內容。本文僅供一般參考,不考慮您的個人投資目標、財務狀況或需求。TTM對信息的準確性和完整性不承擔任何責任或保證,投資者應自行研究並在投資前尋求專業建議。

熱議股票

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10