The recent pullback must have dismayed ZO Future Group (HKG:2309) insiders who own 68% of the company

Key Insights

- ZO Future Group's significant insider ownership suggests inherent interests in company's expansion

- A total of 2 investors have a majority stake in the company with 52% ownership

- Past performance of a company along with ownership data serve to give a strong idea about prospects for a business

To get a sense of who is truly in control of ZO Future Group (HKG:2309), it is important to understand the ownership structure of the business. With 68% stake, individual insiders possess the maximum shares in the company. In other words, the group stands to gain the most (or lose the most) from their investment into the company.

As market cap fell to HK$1.6b last week, insiders would have faced the highest losses than any other shareholder groups of the company.

In the chart below, we zoom in on the different ownership groups of ZO Future Group.

View our latest analysis for ZO Future Group

What Does The Lack Of Institutional Ownership Tell Us About ZO Future Group?

Small companies that are not very actively traded often lack institutional investors, but it's less common to see large companies without them.

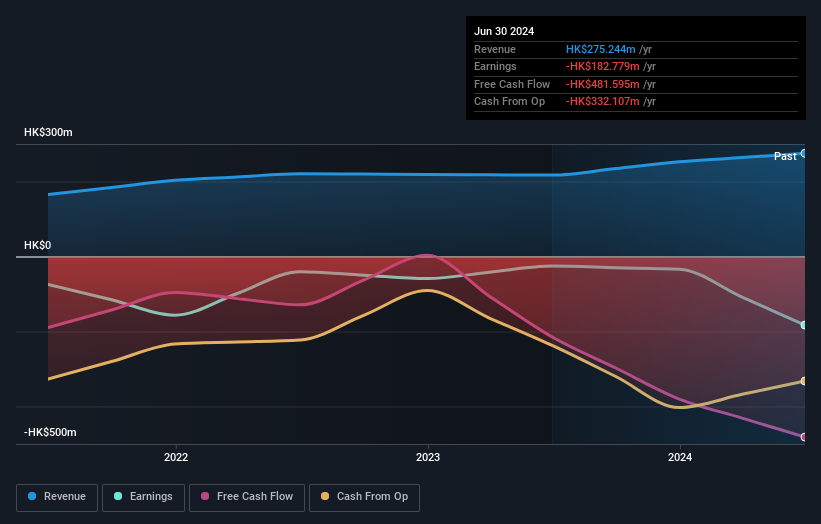

There are many reasons why a company might not have any institutions on the share registry. It may be hard for institutions to buy large amounts of shares, if liquidity (the amount of shares traded each day) is low. If the company has not needed to raise capital, institutions might lack the opportunity to build a position. Alternatively, there might be something about the company that has kept institutional investors away. Institutional investors may not find the historic growth of the business impressive, or there might be other factors at play. You can see the past revenue performance of ZO Future Group, for yourself, below.

ZO Future Group is not owned by hedge funds. Cho Hung Suen is currently the company's largest shareholder with 27% of shares outstanding. For context, the second largest shareholder holds about 25% of the shares outstanding, followed by an ownership of 16% by the third-largest shareholder.

After doing some more digging, we found that the top 2 shareholders collectively control more than half of the company's shares, implying that they have considerable power to influence the company's decisions.

Researching institutional ownership is a good way to gauge and filter a stock's expected performance. The same can be achieved by studying analyst sentiments. As far as we can tell there isn't analyst coverage of the company, so it is probably flying under the radar.

Insider Ownership Of ZO Future Group

The definition of an insider can differ slightly between different countries, but members of the board of directors always count. The company management answer to the board and the latter should represent the interests of shareholders. Notably, sometimes top-level managers are on the board themselves.

Most consider insider ownership a positive because it can indicate the board is well aligned with other shareholders. However, on some occasions too much power is concentrated within this group.

Our information suggests that insiders own more than half of ZO Future Group. This gives them effective control of the company. So they have a HK$1.1b stake in this HK$1.6b business. It is good to see this level of investment. You can check here to see if those insiders have been buying recently.

General Public Ownership

With a 32% ownership, the general public, mostly comprising of individual investors, have some degree of sway over ZO Future Group. This size of ownership, while considerable, may not be enough to change company policy if the decision is not in sync with other large shareholders.

Next Steps:

I find it very interesting to look at who exactly owns a company. But to truly gain insight, we need to consider other information, too. Case in point: We've spotted 2 warning signs for ZO Future Group you should be aware of, and 1 of them is a bit concerning.

Of course, you might find a fantastic investment by looking elsewhere. So take a peek at this free list of interesting companies.

NB: Figures in this article are calculated using data from the last twelve months, which refer to the 12-month period ending on the last date of the month the financial statement is dated. This may not be consistent with full year annual report figures.

Valuation is complex, but we're here to simplify it.

Discover if ZO Future Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

免責聲明:投資有風險,本文並非投資建議,以上內容不應被視為任何金融產品的購買或出售要約、建議或邀請,作者或其他用戶的任何相關討論、評論或帖子也不應被視為此類內容。本文僅供一般參考,不考慮您的個人投資目標、財務狀況或需求。TTM對信息的準確性和完整性不承擔任何責任或保證,投資者應自行研究並在投資前尋求專業建議。

熱議股票

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10