Penumbra (NYSE:PEN) Sees 24% Price Jump Despite Net Income Drop To US$34 Million

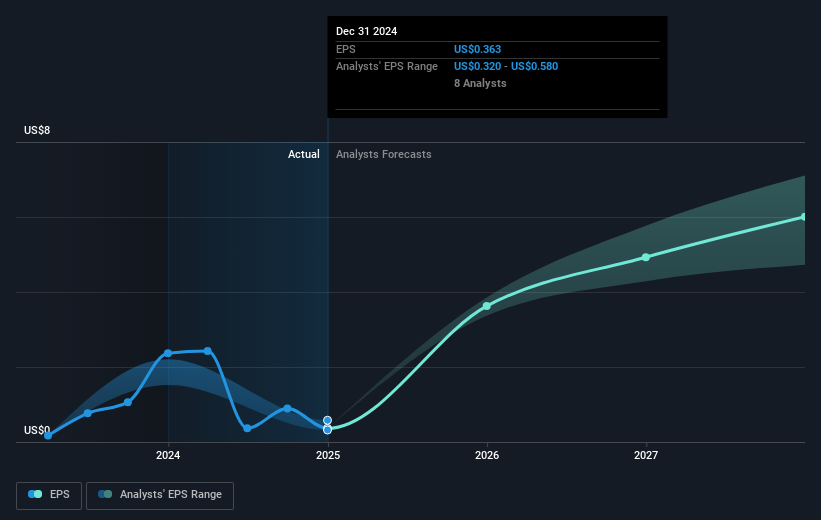

Penumbra (NYSE:PEN) recently reported its fourth-quarter earnings, revealing a sales increase to USD 316 million up from USD 285 million, yet a net income drop to USD 34 million from USD 54 million. Despite these mixed financial results, the company's stock experienced a 24% price increase over the last quarter, aligning with the optimistic corporate guidance projecting a 12% to 14% revenue growth for 2025. This optimism may have encouraged investor confidence, driving the price upward. This move occurred amidst a broader market context where the Dow experienced declines due to issues in the healthcare sector, particularly UnitedHealth's DOJ probe. Yet, the S&P 500 remains a touch below record highs, indicating mixed sentiment across sectors. The market's overall stability and potential economic growth forecasts make Penumbra’s upward trajectory notable, highlighting investor responsiveness to its forward-looking statements despite the backdrop of fluctuating market indexes.

Dig deeper into the specifics of Penumbra here with our thorough analysis report.

Penumbra's shares have delivered a total return of 73.46% over the last five years. This period saw significant growth, with earnings increasing substantially by 22.5% annually. However, recent one-off losses, including a US$110.3 million hit, have impacted financial results, altering the profit landscape. Over the past year, despite underperforming the US market, Penumbra managed to outperform its industry, the US Medical Equipment sector.

Corporate actions also shaped this trajectory, with the company completing a share buyback program worth US$100 million in late 2024, which likely supported the stock's performance. Furthermore, the company's forward-looking revenue guidance has consistently shown optimism, projecting considerable growth, which may have bolstered investor sentiment. Despite challenges, Penumbra's revenue forecasts surpass the broader market, indicating potential future momentum.

- Analyze Penumbra's fair value against its market price in our detailed valuation report—access it here.

- Discover the key vulnerabilities in Penumbra's business with our detailed risk assessment.

- Have a stake in Penumbra? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency• Be alerted to new Warning Signs or Risks via email or mobile• Track the Fair Value of your stocks

Try a Demo Portfolio for FreeHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

免責聲明:投資有風險,本文並非投資建議,以上內容不應被視為任何金融產品的購買或出售要約、建議或邀請,作者或其他用戶的任何相關討論、評論或帖子也不應被視為此類內容。本文僅供一般參考,不考慮您的個人投資目標、財務狀況或需求。TTM對信息的準確性和完整性不承擔任何責任或保證,投資者應自行研究並在投資前尋求專業建議。

熱議股票

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10