Abbott Laboratories (NYSE:ABT) Declares 405th Consecutive Quarterly Dividend of US$0.59 Per Share

Abbott Laboratories (NYSE:ABT) recently declared a dividend of 59 cents per share, marking its 405th quarterly dividend, underscoring its consistent shareholder return approach since 1924. This announcement coincides with a remarkable price increase of about 15% for Abbott's shares over the last quarter, potentially strengthened by positive earnings figures for Q4 2024 and full-year 2024, showcasing rising sales and net income. The market context, with a broad downturn including a 2.2% weekly decline in indexes like the Dow and S&P 500, adds to the significance of Abbott's performance against these backdrops. Its guidance for 2025 predicting a growth in organic sales boosts investor confidence. Furthermore, product advancements such as the inclusion of its FreeStyle Libre 2 in Alberta's Drug Benefit List may have positively influenced market perception despite broader market volatility and economic challenges.

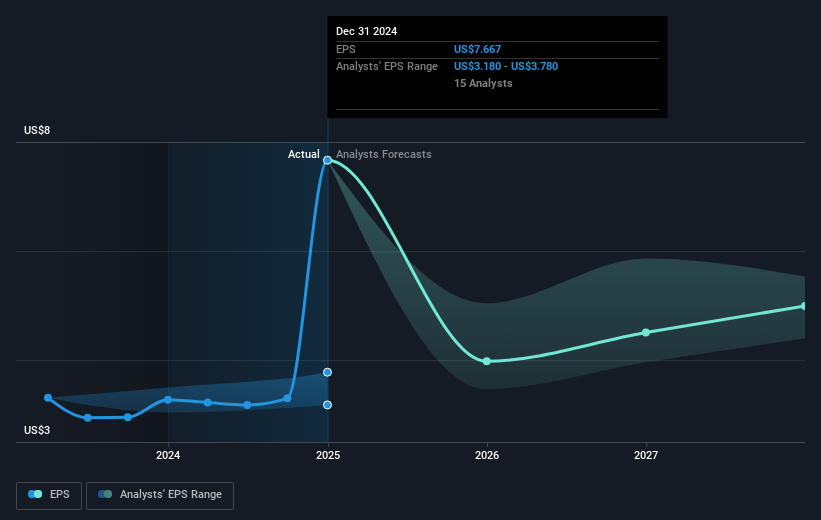

See the full analysis report here for a deeper understanding of Abbott Laboratories.

Over the past five years, Abbott Laboratories has achieved a total shareholder return of 91.30%, indicating strong performance in both share price appreciation and dividend payouts. Several factors contribute to this result. The company demonstrated impressive profit growth in the past year, with earnings surging at a rate that exceeded the medical equipment industry. Notably, Abbott has consistently grown its dividends, achieving 53 consecutive years of dividend increases, reflecting a commitment to rewarding shareholders.

In addition, during the past year, Abbott reported a very large increase in net income, up to US$9.23 billion in Q4 2024, significantly higher than prior years. The inclusion of its FreeStyle Libre 2 on Alberta’s Drug Benefit List and successful trials of its TAVI system and AVEIR pacing device reflect product innovation that may positively impact long-term growth. Furthermore, its valuation appears attractive compared to its peers, providing a potential draw for investors seeking value in a competitive market.

- Discover whether Abbott Laboratories is fairly priced, undervalued, or overvalued in our comprehensive valuation breakdown.

- Assess the potential risks impacting Abbott Laboratories' growth trajectory—explore our risk evaluation report.

- Is Abbott Laboratories part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency• Be alerted to new Warning Signs or Risks via email or mobile• Track the Fair Value of your stocks

Try a Demo Portfolio for FreeHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

免責聲明:投資有風險,本文並非投資建議,以上內容不應被視為任何金融產品的購買或出售要約、建議或邀請,作者或其他用戶的任何相關討論、評論或帖子也不應被視為此類內容。本文僅供一般參考,不考慮您的個人投資目標、財務狀況或需求。TTM對信息的準確性和完整性不承擔任何責任或保證,投資者應自行研究並在投資前尋求專業建議。

熱議股票

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10