Target (NYSE:TGT) Launches Disney And Marvel Kids' Bedding Collections Under US$30

Target (NYSE:TGT) recently introduced new kids' bedding collections featuring Disney and Marvel characters, marking the first of several planned collaborations with Disney in 2025. Meanwhile, the retail sector was overshadowed by broader market declines, as seen with the tech-heavy Nasdaq Composite falling 2% and the S&P 500 dropping 1% amid concerns over economic outlook and policy impact. While Target launched innovative product lines like Carroten's suncare and Imaraïs Beauty gummies, earnings guidance suggested modest growth, potentially influencing investor perception. Legal issues, such as a class action lawsuit related to ESG initiatives, added to the complexities facing the company. Concurrently, significant leadership changes were announced, possibly affecting strategic direction. The market's overall downtrend, with a 3% drop over the past week, combined with tech stocks' pressures, may have compounded the influence on Target's share price, leading to a 0.62% decline this quarter.

Get an in-depth perspective on Target's performance by reading our analysis here.

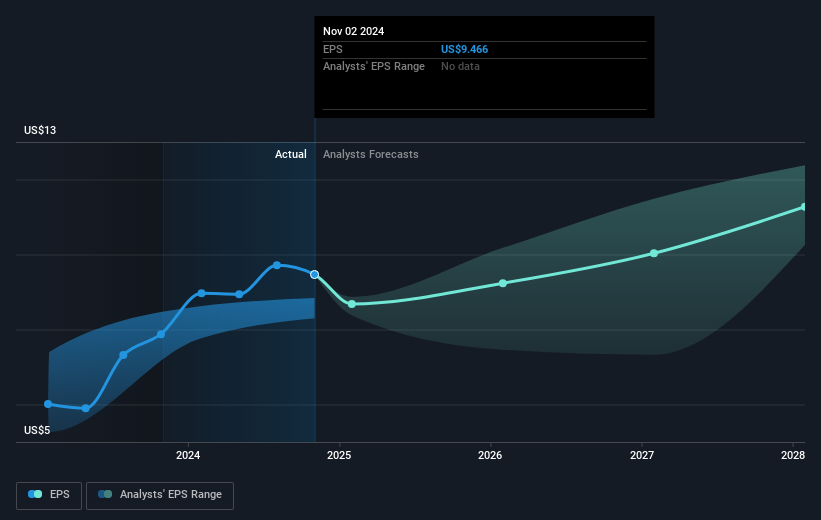

The past 5 years have seen Target's total shareholder returns reach 29.83%, reflecting a combination of share price appreciation and consistent dividend payments. Despite recent underperformance compared to the broader market and the U.S. Consumer Retailing industry over the last year, Target's value proposition remains recognized. Factors such as its robust Price-To-Earnings Ratio of 13.2x compared to its peers and the industry indicate good valuation, although the company's declining earnings of 0.3% per year over this period paint a more complex picture.

Target's consistent dividend payments, including its recent US$1.12 quarterly dividend, reflect its ongoing shareholder focus. Over the past year, Target has seen its profit margins improve, with current net profit margins rising to 4.1% from 3.4% a year ago, linked with earnings growth of 19.5%. However, the company's overall earnings growth forecasts remain below the U.S. market average, potentially influencing longer-term investor sentiment.

- Analyze Target's fair value against its market price in our detailed valuation report—access it here.

- Gain insight into the risks facing Target and how they might influence its performance—click here to read more.

- Shareholder in Target? Ensure you're never caught off-guard by adding your portfolio in Simply Wall St for timely alerts on significant stock developments.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Target might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

免責聲明:投資有風險,本文並非投資建議,以上內容不應被視為任何金融產品的購買或出售要約、建議或邀請,作者或其他用戶的任何相關討論、評論或帖子也不應被視為此類內容。本文僅供一般參考,不考慮您的個人投資目標、財務狀況或需求。TTM對信息的準確性和完整性不承擔任何責任或保證,投資者應自行研究並在投資前尋求專業建議。

熱議股票

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10