Red Cat Holdings (NasdaqCM:RCAT) Secures US$20 Million Deal Amidst 16% Price Drop

Red Cat Holdings (NasdaqCM:RCAT) has recently experienced a price decline of 16% over the past month, coinciding with significant strategic decisions and broader market movements. The company has secured a $20 million convertible debt agreement with The Lind Partners, coupled with an Analyst/Investor Day where it discussed a new partnership roadmap aimed at long-term growth. While these developments indicate a concerted effort to bolster its strategic direction, they occur amid a mixed market backdrop. Investor apprehensions were heightened by broader economic concerns, tariff announcements, and mixed performances in major indices, such as a 0.7% rise in the Dow Jones alongside a 0.1% dip in the S&P 500. Such conditions might have influenced the recent stock performance of RCAT, which aligns with the overall 3.6% market decline in the past week, potentially reflecting investor reactions to economic policies and market volatility.

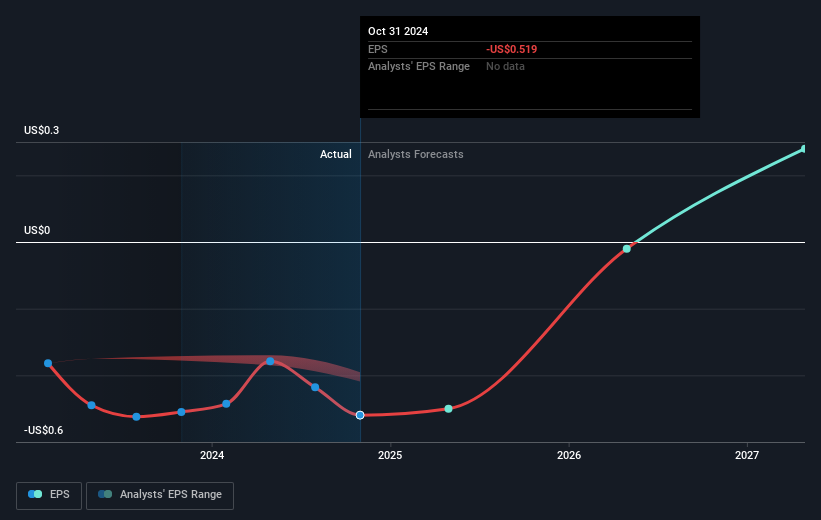

Click to explore a detailed breakdown of our findings on Red Cat Holdings.

Over the last year, Red Cat Holdings achieved a very large total shareholder return, far exceeding the broader US market and its industry, which saw returns of 16.7% and 12.4%, respectively. This remarkable performance can be linked to several key developments. In early 2024, Red Cat significantly grew its revenue, showcasing promising fiscal results, especially with its fiscal year 2024 sales reaching US$17.84 million, up significantly from the previous year. Additionally, the company's proactive approach to securing major contracts, such as the US$1.6 million deal with U.S. Customs & Border Protection in October, likely played a vital role in boosting investor confidence.

The company also fortified its strategic partnerships to enhance drone capabilities, exemplified by its expanded collaboration with Palladyne AI in November 2024. Furthermore, executive changes, including the appointment of Chris Rill as President of Teal Drones in December, might have contributed to renewed market enthusiasm. Lastly, Red Cat's addition to the S&P Technology Hardware Select Industry Index in December helped solidify its market position, possibly supporting its substantial total shareholder returns during this period.

- Understand the fair market value of Red Cat Holdings with insights from our valuation analysis—click here to learn more.

- Discover the key vulnerabilities in Red Cat Holdings' business with our detailed risk assessment.

- Already own Red Cat Holdings? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)• Undervalued Small Caps with Insider Buying• High growth Tech and AI CompaniesOr build your own from over 50 metrics.

Explore Now for FreeHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

免責聲明:投資有風險,本文並非投資建議,以上內容不應被視為任何金融產品的購買或出售要約、建議或邀請,作者或其他用戶的任何相關討論、評論或帖子也不應被視為此類內容。本文僅供一般參考,不考慮您的個人投資目標、財務狀況或需求。TTM對信息的準確性和完整性不承擔任何責任或保證,投資者應自行研究並在投資前尋求專業建議。

熱議股票

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10