Iovance Biotherapeutics (NasdaqGM:IOVA) Reports Surge in Q4 Revenue to US$74M with Improved Losses

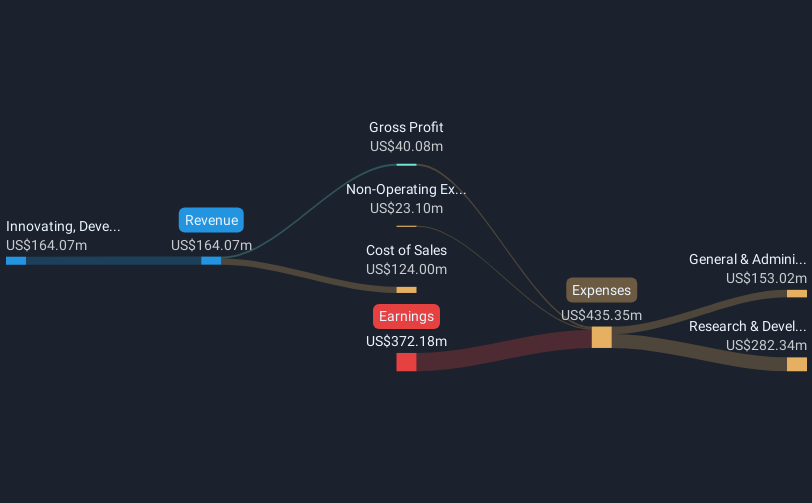

Iovance Biotherapeutics (NasdaqGM:IOVA) reported marked improvement in its financial performance, with revenue soaring to $73 million in Q4 2024 from $0.5 million the previous year and a reduced net loss. Despite this, the stock price fell 6% last week. This price movement comes amid a broader market decline, with the Nasdaq dropping 5.5% in February, likely influenced by broader economic concerns and uncertainty around tariffs. Even as Iovance reaffirmed its fiscal guidance for 2025, macroeconomic headwinds, including inflation easement and tech sector volatility, potentially contributed to investor caution. The broader market pressure and specific sector dynamics may have compounded the decrease in Iovance's share price, demonstrating that impressive revenue growth and narrowed losses did not insulate the company from market-wide trends.

Dig deeper into the specifics of Iovance Biotherapeutics here with our thorough analysis report.

```html

Over the past three years, Iovance Biotherapeutics' total shareholder returns have been -62.43%, reflecting challenges outside of short-term market pressures. While recent robust revenue growth and strategic advances like FDA approval for its AMTAGVI™ therapy have marked significant progress, the company has consistently faced profitability issues. Losses have increased by 16.5% annually over five years, affecting investor sentiment despite revenue growth forecasts. Additionally, Iovance's valuation remains high, with a Price-To-Sales Ratio significantly above both the estimated fair and industry averages, which may have weighed on its stock's long-term performance.

Comparatively, Iovance underperformed the broader US Biotech industry and market over the past year, which saw a -7% return for the industry and a 16.9% return for the market. This could be partly due to unprofitable operations and a negative Return on Equity, factors that often temper shareholder enthusiasm. Further, follow-on equity offerings in February and July 2024 potentially diluted share value, exacerbating the decline in total returns.

```- See how Iovance Biotherapeutics measures up with our analysis of its intrinsic value versus market price.

- Uncover the uncertainties that could impact Iovance Biotherapeutics' future growth—read our risk evaluation here.

- Is Iovance Biotherapeutics part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)• Undervalued Small Caps with Insider Buying• High growth Tech and AI CompaniesOr build your own from over 50 metrics.

Explore Now for FreeHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

免責聲明:投資有風險,本文並非投資建議,以上內容不應被視為任何金融產品的購買或出售要約、建議或邀請,作者或其他用戶的任何相關討論、評論或帖子也不應被視為此類內容。本文僅供一般參考,不考慮您的個人投資目標、財務狀況或需求。TTM對信息的準確性和完整性不承擔任何責任或保證,投資者應自行研究並在投資前尋求專業建議。

熱議股票

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10