Carvana (NYSE:CVNA) Up 11% In A Week Following Q4 Earnings Turnaround

Carvana (NYSE:CVNA) recently announced a significant improvement in its Q4 2024 earnings, showcasing substantial growth in sales and revenue, and achieving a positive net income after a period of losses. This strong financial performance likely contributed to the company's 11% share price rise over the past week. Meanwhile, the broader market remained positive, with major indexes showing resilience, which may have further supported Carvana's gains. The improving performance signals a potential recovery for Carvana, contrasting with some market sectors experiencing volatility, like Nike and FedEx, which reported disappointing outlooks and declines.

We've identified 3 weaknesses with Carvana (at least 1 which is a bit concerning) and understanding the impact should be part of your investment process.

AI is about to change healthcare. These 25 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

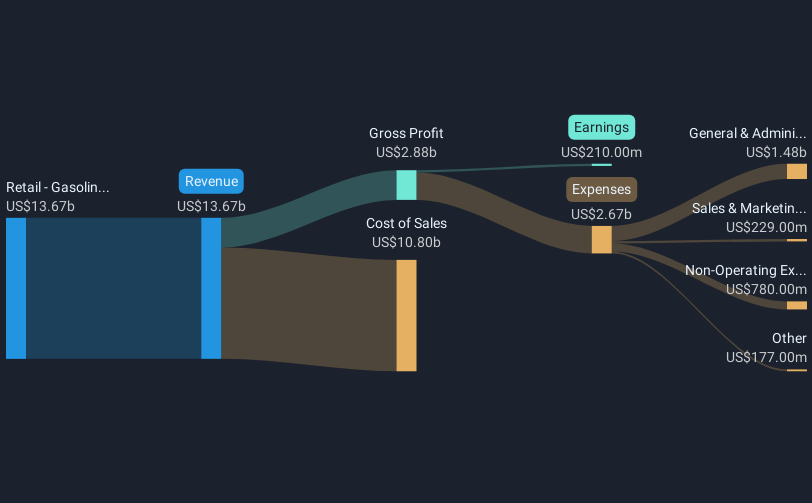

Over the past five years, Carvana's shares have delivered a total return of 227.89%. This impressive performance can be attributed to several key developments. Notable among these was the successful integration of ADESA mega sites, significantly boosting reconditioning capacity and enhancing operational efficiency. Concurrently, Carvana's adoption of AI technologies optimized inventory management, streamlining processes and improving customer experiences. This focus on operational prowess and customer satisfaction positioned the company favorably against challenges like high debt levels and competitive market dynamics.

Further bolstering the company's position, Carvana's expansion initiatives, including the introduction of same-day vehicle delivery in multiple regions, enhanced sales capacity and customer convenience. Financial strategies including a substantial debt reduction of over US$1.325 billion also contributed to its financial stability. Over the past year, Carvana outperformed both the broader US market and the Specialty Retail industry, highlighting its strong market standing despite a challenging economic climate.

In light of our recent valuation report, it seems possible that Carvana is trading beyond its estimated value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)• Undervalued Small Caps with Insider Buying• High growth Tech and AI CompaniesOr build your own from over 50 metrics.

Explore Now for FreeHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

免責聲明:投資有風險,本文並非投資建議,以上內容不應被視為任何金融產品的購買或出售要約、建議或邀請,作者或其他用戶的任何相關討論、評論或帖子也不應被視為此類內容。本文僅供一般參考,不考慮您的個人投資目標、財務狀況或需求。TTM對信息的準確性和完整性不承擔任何責任或保證,投資者應自行研究並在投資前尋求專業建議。

熱議股票

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10