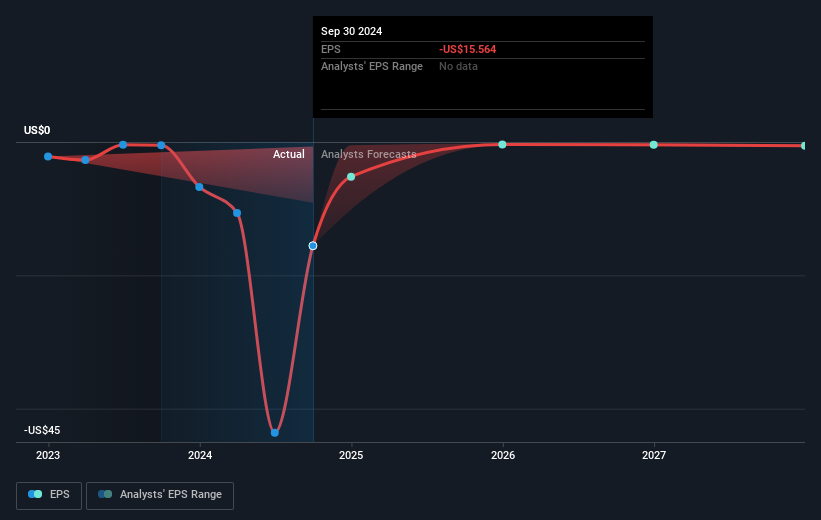

Oklo (NYSE:OKLO) Sees 4% Rise Over Last Quarter Amid US$74 Million Net Loss

Oklo (NYSE:OKLO) recorded a 4% increase in share price over the past quarter, reflecting the company's proactive regulatory engagement and strategic developments in the nuclear energy sector. Key events include significant regulatory engagements with the U.S. Nuclear Regulatory Commission for the Aurora Powerhouse, and a Memorandum of Agreement with the Department of Energy, which bolster the company's potential for growth despite reporting a net loss of USD 74 million in annual financial results. While the broader market has remained flat in recent days, recent tariff announcements have overshadowed many sectors, affecting tech and retail stocks more than companies like Oklo focused on long-term energy solutions.

We've spotted 4 risks for Oklo you should be aware of, and 1 of them is concerning.

We've found 19 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

Over the past three years, Oklo's shares have achieved a total return of 132.58%. Compared to the previous year, Oklo's performance outpaced both the broader US market and the US Electric Utilities industry. Several key developments have contributed to this impressive longer-term return. Noteworthy is the signing of a Master Power Agreement with Switch in December 2024 for 12 GW of power projects, which marked a significant commitment to clean power expansion. Additionally, the partnership under Letters of Intent to provide low carbon power for data centers was a step towards broader infrastructure engagement across the U.S.

The company's leadership changes, with the appointment of Daniel Poneman and Michael Thompson to the Board in March 2025, brought expertise in nuclear technology and financing to Oklo, signaling strengthened governance. Strategic alliances, like the MOU with Lightbridge Corporation for nuclear waste recycling, aligned with Oklo's forward-looking approach in the nuclear sector, likely enhancing investor confidence in the company's long-term vision.

Explore historical data to track Oklo's performance over time in our past results report.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)• Undervalued Small Caps with Insider Buying• High growth Tech and AI CompaniesOr build your own from over 50 metrics.

Explore Now for FreeHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

免責聲明:投資有風險,本文並非投資建議,以上內容不應被視為任何金融產品的購買或出售要約、建議或邀請,作者或其他用戶的任何相關討論、評論或帖子也不應被視為此類內容。本文僅供一般參考,不考慮您的個人投資目標、財務狀況或需求。TTM對信息的準確性和完整性不承擔任何責任或保證,投資者應自行研究並在投資前尋求專業建議。

熱議股票

沒有相關數據