Should You Investigate Westlake Corporation (NYSE:WLK) At US$88.46?

Let's talk about the popular Westlake Corporation (NYSE:WLK). The company's shares received a lot of attention from a substantial price movement on the NYSE over the last few months, increasing to US$119 at one point, and dropping to the lows of US$88.46. Some share price movements can give investors a better opportunity to enter into the stock, and potentially buy at a lower price. A question to answer is whether Westlake's current trading price of US$88.46 reflective of the actual value of the large-cap? Or is it currently undervalued, providing us with the opportunity to buy? Let’s take a look at Westlake’s outlook and value based on the most recent financial data to see if there are any catalysts for a price change.

AI is about to change healthcare. These 20 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10bn in marketcap - there is still time to get in early.

Is Westlake Still Cheap?

According to our price multiple model, which makes a comparison between the company's price-to-earnings ratio and the industry average, the stock price seems to be justfied. In this instance, we’ve used the price-to-earnings (PE) ratio given that there is not enough information to reliably forecast the stock’s cash flows. We find that Westlake’s ratio of 18.94x is trading slightly above its industry peers’ ratio of 17.32x, which means if you buy Westlake today, you’d be paying a relatively sensible price for it. And if you believe that Westlake should be trading at this level in the long run, then there should only be a fairly immaterial downside vs other industry peers. Is there another opportunity to buy low in the future? Since Westlake’s share price is quite volatile, we could potentially see it sink lower (or rise higher) in the future, giving us another chance to buy. This is based on its high beta, which is a good indicator for how much the stock moves relative to the rest of the market.

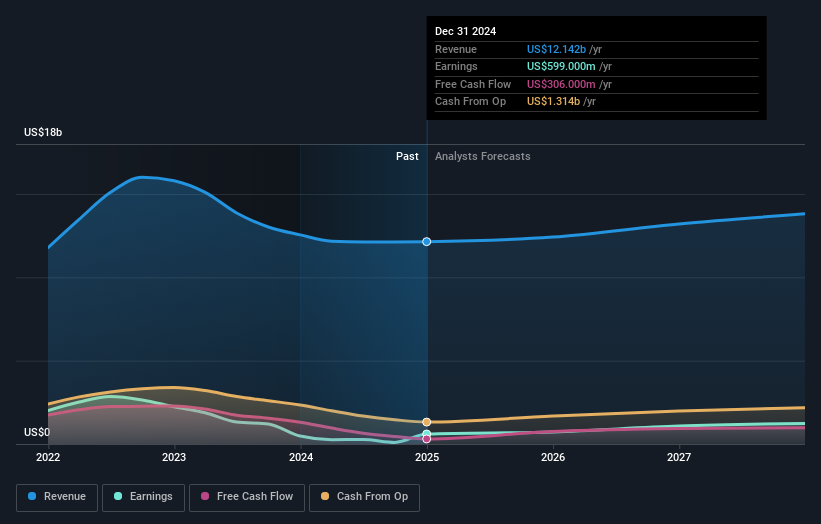

Check out our latest analysis for Westlake

Can we expect growth from Westlake?

Investors looking for growth in their portfolio may want to consider the prospects of a company before buying its shares. Buying a great company with a robust outlook at a cheap price is always a good investment, so let’s also take a look at the company's future expectations. Westlake's earnings over the next few years are expected to double, indicating a very optimistic future ahead. This should lead to stronger cash flows, feeding into a higher share value.

What This Means For You

Are you a shareholder? It seems like the market has already priced in WLK’s positive outlook, with shares trading around industry price multiples. However, there are also other important factors which we haven’t considered today, such as the financial strength of the company. Have these factors changed since the last time you looked at WLK? Will you have enough conviction to buy should the price fluctuate below the industry PE ratio?

Are you a potential investor? If you’ve been keeping tabs on WLK, now may not be the most optimal time to buy, given it is trading around industry price multiples. However, the optimistic forecast is encouraging for WLK, which means it’s worth diving deeper into other factors such as the strength of its balance sheet, in order to take advantage of the next price drop.

Since timing is quite important when it comes to individual stock picking, it's worth taking a look at what those latest analysts forecasts are. Luckily, you can check out what analysts are forecasting by clicking here .

If you are no longer interested in Westlake, you can use our free platform to see our list of over 50 other stocks with a high growth potential.

Valuation is complex, but we're here to simplify it.

Discover if Westlake might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

免責聲明:投資有風險,本文並非投資建議,以上內容不應被視為任何金融產品的購買或出售要約、建議或邀請,作者或其他用戶的任何相關討論、評論或帖子也不應被視為此類內容。本文僅供一般參考,不考慮您的個人投資目標、財務狀況或需求。TTM對信息的準確性和完整性不承擔任何責任或保證,投資者應自行研究並在投資前尋求專業建議。

熱議股票

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10