Betting Against The Market With The SPDN ETF

- The SPDN ETF offers a way to bet against the market, moving inversely to the S&P 500, but it's not for long-term holding.

- Market's muted response to rate cuts suggests they're already priced in; high S&P 500 P/E ratio supports this sentiment.

- Weak economic data, potential oil price spikes, and slowing consumer demand could negatively impact market valuations and company earnings.

- SPDN's 0.58% expense ratio is offset by a 6% dividend yield, but timing is crucial to avoid significant losses, assuming continued long-term normal market conditions.

honglouwawa

Investment thesis: The SPDN ETF (NYSEARCA:SPDN) offers a convenient way for investors to bet against the market's continued appreciation. The market's tepid reaction to the clear signal that the Federal Reserve intends to start lowering interest rates suggests that the expected rate cuts are already priced in. The high P/E ratio of the S&P 500 (SPX) reinforces that sentiment. The Federal Reserve's gift to markets in the form of lower interest rates that can help to justify higher stock market valuations, may also be canceled out by increasingly weak economic data, which may suffer an extra hit from a potential oil price spike later this year or going into next year. I started a modest position in SPDN shares, with the intent to buy more on the way down as it moves inversely, and proportionally with the S&P 500. If it starts moving higher, for valid reasons, I may consider buying on the way up, as long as fundamentals justify the move and evidence suggests that the market selloff will be sustained.

About the SPDN ETF.

The Direxion Daily S&P 500 Bear 1X ETF is designed to provide investors with an opportunity to invest in an asset that moves opposite & proportionally to the S&P 500 index.

Direxion

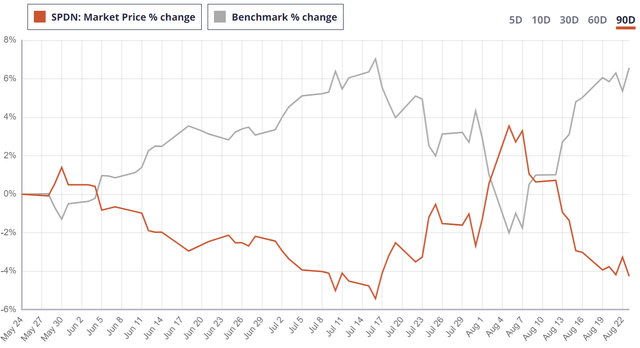

In the past few months, the S&P moved up 6% and the SPD almost mirrored the move with a 4% decline, as the chart shows. It is not a perfect correlation, but it is close enough.

For the longer term, the SPDN ETF is destined to permanently decline as long as normal market conditions persist. In other words, as long as we can expect the S&P 500 index to continue appreciating for the long term, the SPDN ETF will lose its share price.

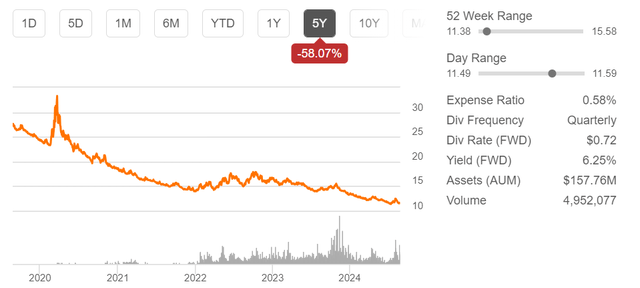

SPDN 5-year share price chart & other metrics (Seeking Alpha)

The only way to benefit from investing in it is to execute a well-timed entry point, and then time the exit just as well. This is not a long-term buy-and-hold investment opportunity.

The expense ratio of .58% is made bearable by the expected dividend yield, which is rather generous, currently in the 6% range. The dividend yield is high enough that it has the potential to blunt longer-term losses if one gets the timing of this investment wrong. If for instance, the S&P were to rise 16% in the next 12 months, to 6,500 points the loss in the share value of SPDN for the year would be around 10% once the dividend is factored in.

Markets did not respond to news of impending rate cuts with the expected rally, because lower interest rates are already baked in.

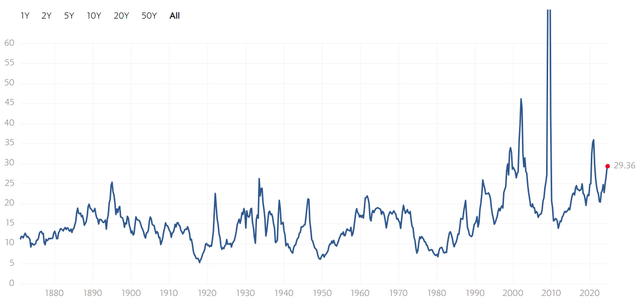

Perhaps the most profound statement on the stock market post-2008, after the era of low interest rates was ushered in was Warren Buffet's correlation of acceptable market valuations with interest rates. In other words, when interest rates are kept low for a prolonged period, it may be alright to see P/E ratios rising above the long-term historical average of about 16.

S&P 500 historical P/E ratio (Multipl.com)

We are almost double the historical average in terms of the P/E ratio of the S&P 500 index. Initial market reactions to declining interest rates may push the stock markets higher, but it is unclear where it can go from here on a sustained basis.

We are seeing early signs of an impending decline in consumer demand, driven by a deterioration in household finances.

The market's valuation issues may be exacerbated in the coming quarters if the early signs of slowing job growth, deteriorating household finances, and perhaps a decline in government spending growth combine to negatively impact revenues and profits.

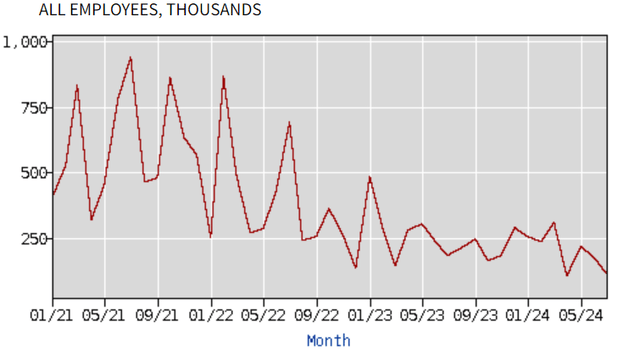

U.S. Bureau of Labor Statistics

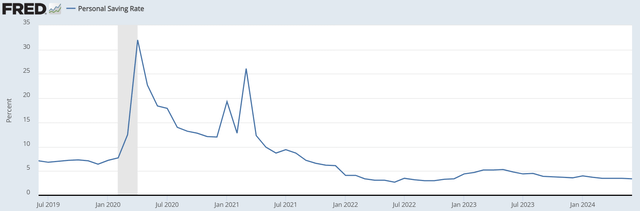

As we can see, the post-COVID jobs recovery is slowing down dramatically. The unemployment rate of 4.3% is not high, but it is higher than at the end of 2019 when it was 3.6%. Consumer spending is still holding up, but the personal savings rate is now only half of what it was just before the COVID pandemic.

Federal Reserve Bank of St. Louis

Between a tightening jobs market and a deteriorating household financial situation, it stands to reason that a significant consumer pullback may be on the horizon. Since consumer spending contributes about 2/3 of the overall makeup of the economy, company earnings may come under pressure in the next few quarters if consumers start to pull back on spending.

Prospects for an oil price spike should not be ignored.

Perhaps the greatest threat to the economy is also the one factor that tends to be ignored currently. The reason why the markets are ignoring this is because there is a significant schism between the EIA & IEA on the one hand, both of which are forecasting weak demand, and robust oil supply growth, and OPEC on the other which sees a current supply shortfall, that has the potential to widen as demand growth remains robust. The market seems to mostly focus on the IEA & EIA forecasts.

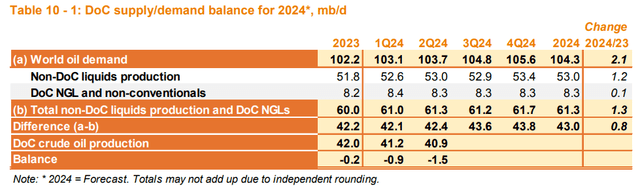

OPEC

As the OPEC supply/demand balance report shows, for the second quarter of this year, there was a 1.5 mb/d shortfall in global liquid fuel supplies. By the fourth quarter demand will be almost 2 mb/d higher compared with the second quarter. It is unclear where the extra supply will come from to cover that growth, and to reduce the already-existing supply/demand gap.

The IEA is forecasting demand growth of 1 mb/d for this year and the same for next year, which is only half of OPEC's forecast growth. The IEA also sees global liquid fuel supplies growing twice as fast as demand next year. In other words, there is no reason for the market to bid up the price of oil, since there is an excess in supplies on the horizon.

The divergence in forecasts, estimates, and even backward-looking data seems to be growing, which calls into question the reliability of data going forward. My take on it is that these reports are increasingly subservient to political, geopolitical, and national interests, with the interest of investors and the overall market sacrificed in favor of those above-mentioned interests. We have no way of knowing which outlook is less reliable.

While we wait for data validation and confirmation of which viewpoint turns out to be closer to reality, we have to be mindful of the potential implications for the markets in the next few months. If the IEA is closer to reality, and oil prices remain tame, inflation could decline further, giving central banks room to cut rates. Consumers and companies alike will also benefit from lower energy costs. It could help to sustain the current economic recovery, which should be a positive for the stock markets.

If OPEC turns out to be closer to actual reality, at some point soon, the markets will pick up on the supply shortfall situation. Higher oil prices are inflationary. Higher oil prices may put further central bank easing into doubt. Personal consumption is likely to take a hit as well since higher energy costs act as an extra tax on consumers. Companies would see their revenues and profits hit from all sides. Interest rate relief expectations will dissipate, and consumers will cut back on non-essentials. Higher energy costs also tend to increase the costs of operating most businesses, directly or indirectly. If OPEC is correct, the stock market is set for a wild ride, with the overall trend mostly down.

Political & fiscal risks.

By now, we are all familiar with the dire predictions regarding the calamity that awaits us all if the next Presidential election goes in either direction. For once, I have to agree that both camps are putting forward economic platforms that are arguably dangerous. The Harris camp is looking to tax unrealized capital gains, introduce price controls, and introduce several subsidies and other forms of market distortion. The Trump camp is considering introducing trade tariffs as a means for filling the government coffers, instead of income taxes. I doubt that either of these ideas can become policy, regardless of how the election goes. The market could still price in either one of these ideas as a future risk after the election.

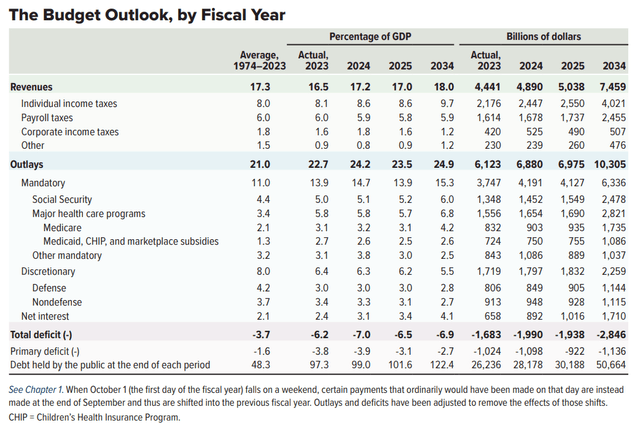

the CBO projects annual shortfalls in the budget of about $2 trillion or higher for the next decade.

CBO

For the current year and next year, we are looking at a $2 trillion deficit, with deficits forecast to grow to $ 3 trillion by 2034. The CBO is not factoring in any potential recessions for the period, which would likely make the situation a lot worse. Regardless of which way the election goes in November, the new administration will have to deal with what has arguably become an unsustainable fiscal situation. So far, both sides are proposing more spending on family support and other items, while the proposals to increase revenues are arguably outright dangerous to the foundational well-being of the economy.

Adding it all up, I believe that there is a chance that after the election is over, the markets will start to take stock of the unsustainable fiscal situation, within the context of the electoral promises made along the way. The conclusion drawn by the market after the election may be that we are looking at another four years of worsening fiscal fundamentals, with no prospect of remediation due to a lack of political will to do so. The market will react accordingly and a classical rush to exit US government bonds before everyone else does can lead to a collapse in private sector demand for US government debt. The scenario may seem far-fetched, but we should remember how quickly the markets turned against Greece's unsustainable debt situation in 2010. We should also remember how hard it was to stem the downward spiral, even though the IMF, the EU, and other actors worked to rescue that small country. There is no external financial safety net large enough to catch a downward-spiraling fiscal situation in the US.

It is hard to see a significant upside for the markets going forward.

While the risks to the markets seem many and severe, it is hard to envision an outcome where the S&P 500 will gain perhaps 30%-50% in the next few years. The odds of a significant fiscal stimulus to the economy are low, given the high deficit situation. The global economy is currently struggling with geopolitical & trade frictions, that are likely to slow the global economy and reduce opportunities for US firms to raise sales in foreign markets. There is the interest rate cut scenario, but as the P/E ratio shows, it is already largely priced in.

Something needs to come along and push the market forward. Perhaps new tech innovations, such as the AI craze may be the catalyst that will move us forward. However, it seems that there is some skepticism about the ability of firms to monetize the AI capabilities they are spending much capital on acquiring. If anything, it may lead to a new tech bubble that can burst at any moment, similar to the dot.com bust, perhaps within months.

I see no prospects of major global economic & military powers sitting down to hammer out a new world order to replace the current one that is crumbling. A new grand bargain could help the global economy to find new synergies and help to bolster economic growth. In other words, we could grow our way out of the rising tide of economic problems. At the moment, it looks like things are set to become far worse before they become better.

Investment implications:

- SPDN is less time-sensitive than other options.

Timing is everything when it comes to investing in an inverse ETF like SPDN or other similar assets. One could argue that if the thesis in favor of betting against the market at this point is so robust, then it might be worth betting on more aggressive alternatives such as the Direxion Daily S&P 500 Bear 3X ETF (SPXS). The problem with a more aggressive alternative is that while the potential gains from a well-timed buy are far more impressive, the higher risk that one can lose out on timing, even if the overall thesis is correct, but delayed makes it far less attractive.

- Inflation may be the main risk to this investment thesis.

This may seem counter-intuitive, but the main risk to a bet against the market at this point may be a return to higher inflation rates. Rising inflation should in theory lead to a decline in real consumer demand, while the Federal Reserve might not be able to lower interest rates, all of which is negative for the markets. However, if hypothetically the Federal Reserve chooses to support the economy instead of fighting inflation, this could lead to a situation where stock markets may rise in nominal terms, even if in real, inflation-adjusted terms markets might be flat at best.

- Buying SPDN incrementally as the S&P 500 index continues to push toward 6,000.

I started a modest position in the SPDN ETF as the S&P 500 index hovers around the 5,600 points mark. I expect that the S&P 500 will reach 6,000 points before a significant market selloff will occur. My initial small investment is just a way to ensure that I will not miss out in case I am wrong. My next buying point will likely be around 5,800 points, and then again once it reaches or comes close to reaching 6,000 points. My plan may change slightly depending on how the markets and indicators will be trending in the next few months. If the market goes the other way, I plan to start selling incrementally once the index drops below 5,000 points. If this investment proves to be not very well timed, I intend to take any losses before the end of next summer at the latest.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

Most Discussed

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10