LGLV: A Low-Volatility ETF Suitable For This Environment

gchutka/E+ via Getty Images

While the equity market has generally remained in a risk-on mode with subdued volatility, sharp selloffs, as seen in August, come alongside elevated volatility, eroding a meaningful portion of past gains. Although these declines were followed by a quick price recovery, this is not always the case. That is why funds offering less volatile options remain in the spotlight.

One such fund is the SPDR SSGA US Large Cap Low Volatility Index ETF (NYSEARCA:LGLV), which selects and weights stocks based on their past volatility. This fund has managed to achieve volatility measures, such as beta, in the range of 0.80 to 0.85 compared to the reference level of 1.0 for the S&P 500 index.

With a positive track record versus other low-volatility ETFs and a slightly different sector allocation relative to peers, LGLV is a good fit for investors looking to diversify their portfolio and take a cautious stance in an environment of slow economic growth alongside the uncertain interest rate path and the upcoming U.S. election that could be potential catalysts for stock market moves.

ETF Description & Highlights

LGLV is an exchange-traded fund that follows the performance of large capitalization companies in the U.S. market that exhibit low volatility, tracking the SSGA US Large Cap Low Volatility Index.

This index applies a rules-based process designed to overweight stocks with low volatility, as measured by the standard deviation of monthly total returns over the trailing five years, starting from a universe of eligible securities comprised of the largest 1,000 U.S. stocks by market capitalization.

Eligible stocks are assigned to a sector and ranked within each sector according to their volatility. Stocks exhibiting the lowest volatility, which combined correspond to 30% of the sector's market capitalization, are selected for inclusion in the index. Among these, stocks with the lowest volatility receive the highest weight in the index, following liquidity constraints that limit constituents to 5% of the index and 20 times the stock's weight in the initial universe of the largest 1,000 stocks. This index is rebalanced annually after the close of the last business day of March.

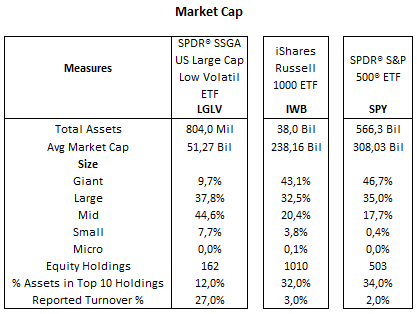

As of August 29, 2024, LGLV has $804 million in AUM invested in 162 companies, with an average market cap of $51.3 billion in an allocation biased toward mid and large-capitalization companies, which combined make up 82.4% of the fund. The remainder is composed of mega caps with 9.7% and small caps with 7.7% of total assets.

LGLV's top ten holdings are Colgate-Palmolive (1.48%), PepsiCo (1.33%), Linde (1.23%), Walmart (1.22%), General Mills (1.22%), Duke Energy (1.12%), Xcel Energy (1.11%), Johnson & Johnson (1.09%), and AvalonBay Communities (1.08%). These holdings represent 12% of total assets, reflecting the index's approach to mitigate stock concentration in an allocation with emphasis on defensive areas like consumer staples and utilities.

Morningstar, consolidated by the author

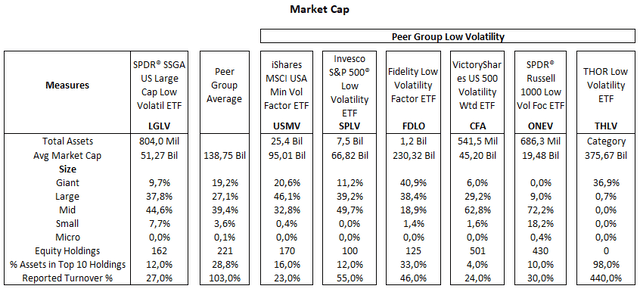

Below is a table comparing LGLV with a peer group of ETFs focusing on lower-volatility stocks. In this list, large funds like USMV and SPLV, alongside other much smaller ETFs, follow distinct strategies. Funds such as SPLV and FDLO hold relatively concentrated portfolios, while CFA has a more diversified allocation strategy with nearly 500 holdings, and THLV invests in sector ETFs instead of common stocks.

Morningstar, consolidated by the author

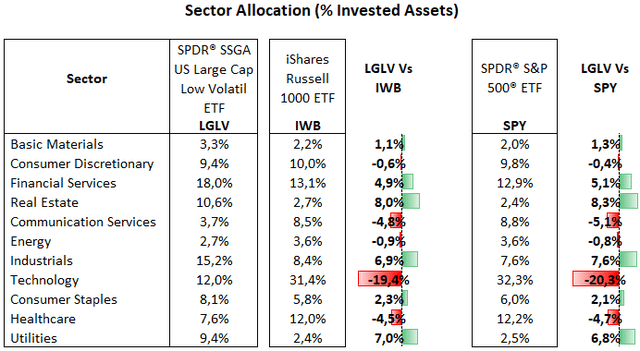

From a sector allocation perspective, LGLV's largest allocation is to the Financial Services sector, with 18.0% of total equities, followed by Industrials with 15.2%, Technology with 12.0%, Real Estate with 10.6%, Utilities with 9.4%, Consumer Discretionary with 9.4%, Consumer Staples with 8.1%, Healthcare with 7.6%, Communication Services with 3.7%, Basic Materials with 3.3%, and Energy with 2.7%.

Relative to the Russell 1000 index, used in this analysis as the benchmark and represented by the iShares Russell 1000 ETF, LGLV is overweight in Real Estate (+8.0%), Utilities (+7.0%), and Industrials (+6.9%), with heavy allocations to residential REITs, multi-utilities and diversified exposure to industrials. In contrast, LGLV is underweight in Technology (-19.4%), Communication Services (-4.8%), and Healthcare (-4.5%), as the fund has virtually no holdings in semiconductor or software in the Technology sector, nor in volatile names in the biotechnology and medical devices industries.

Morningstar, consolidated by the author

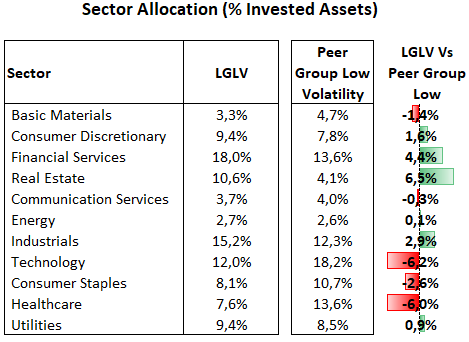

Compared to the peer group of low-volatility ETFs, LGLV is overweight in Real Estate (+6.5%) and Financial Services (+4.4%), as the relatively high volatility seen in Real Estate, with beta near 1.15, has likely prevented the peer group from heavier allocations in the sector. Meanwhile, LGLV is underweight in Technology (-6.2%) and Healthcare (-6.0%), as a beta near 0.70 in the Healthcare sector has understandably drawn the attention of the peer group.

Morningstar, consolidated by the author

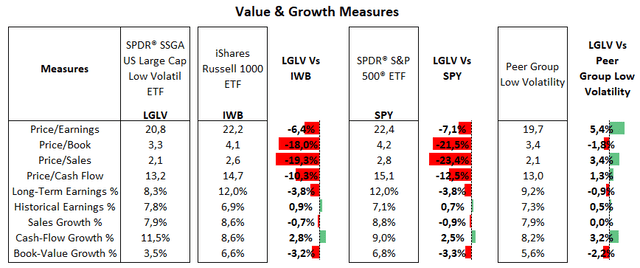

Mixed Valuations

LGLV's underweight exposure to mega caps trading at premium price/earnings ratios like Microsoft (32.2x), Apple (33.9x), Nvidia (46.6x ), and Amazon (37.9x) led its average price/earnings ratio to a discount of nearly 6% compared to the Russell 1000 index. This more than compensates for LGLV's higher allocation in high multiple Real Estate companies like Equinix (P/E 74.3x), AvalonBay (39.7x), and Equity Residential (49.3x). A side effect of this lower allocation to names like Microsoft, Apple and Nvidia can be seen in LGLV's profitability measures, as its average EBITDA margin dropped roughly 10 percentage points compared to the Russell 1000 index, while ROA fell by 7 percentage points. This is not a positive factor for the overall portfolio, but it is the price to pay for the limited exposure to these relatively volatile and profitable behemoth names that have driven the stock market. Furthermore, it is worth noting that despite being underweight in the technology sector, LGVL's price/earnings ratio is nearly 5% higher than that of the peer group of low-volatility ETFs.

Morningstar, consolidated by the author

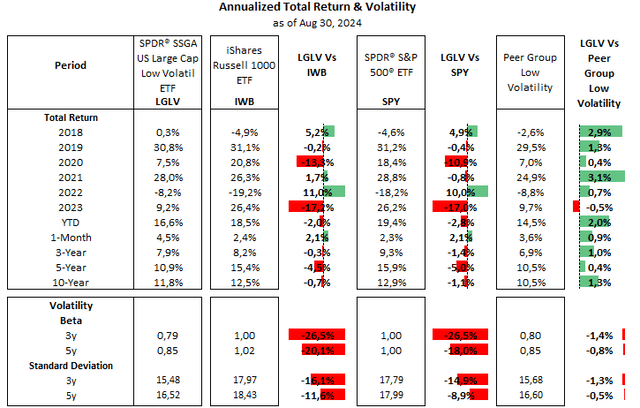

Low Volatility, Outperforming Peers

LGLV and its peer group have arguably delivered on their goals of being less volatile investment vehicles over time, as they have produced more stable performance compared to benchmark indexes, like the S&P 500 and Russell 1000. This was evident in 2022, for example, when they registered a negative return in the 8 to 9% range, while the S&P 500 lost 18%. The flip side occurred in 2023, when low-volatility ETFs gained roughly 9%, but the S&P surged 26%. This relatively lower volatility translates into a beta in the range of 0.80 to 0.85, which is not as low as those of more defensive sectors like consumer staples or utilities, respectively at 0.58 and 0.72, but remains significantly lower than the S&P 500's reference level of 1.0.

However, this moderate volatility has come alongside an underperformance of these low-volatility ETFs, including LGLV, relative to the broader market. Meanwhile, LGLV has outperformed in all timeframes relative to the peer group, with double-digit annualized total returns over the past five years.

Morningstar, consolidated by the author

On balance, there is a mixed picture when comparing LGLV with other low-volatility ETFs. LGLV has delivered higher historical returns, but with a portfolio showing higher valuation measures. Furthermore, LGLV's portfolio contrasts with the peer group to some degree, given its lower exposure to the Technology sector, with only 12% of total holdings, but with overweight exposure to Financials and Real Estate sectors, particularly in the Residential REITs segment. In my view, this is a good thing for investors looking to diversify exposure across different sectors to mitigate concentration risk.

That said, despite lower historical returns relative to the Russell 1000 and the S&P 500 indexes, I view low-volatility ETFs, and particularly LGLV, as a good option to remain invested in the equity market, but with relatively lower downside risk, as the overall market remains vulnerable, driven by a slowing economy that is likely to limit earnings growth and stocks upside, while negative data on the macroeconomic front may trigger new selloffs in the stock market.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

Most Discussed

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10