SPYU: A Great ETN For Savvy Investors

RichVintage/E+ via Getty Images

Once upon a time, a fund like the recently introduced MAX S&P 500 4X Leveraged ETN (NYSEARCA:SPYU) would have likely taken a beating by investment analysts for its irresponsible exposure to risk. About seven years ago, it felt lonely to be one of the very few writers seeing the benefits of investing in leveraged funds, even (and especially) in the context of long-term strategies, if and when done reasonably. Now, I am glad to see others, including on Seeking Alpha, appreciate the case for owning an instrument like SPYU for the long haul.

The risk is sizable

One of the few instances in which introducing a bull thesis on a fund by first talking about risks is in the world of leveraged strategies. This is true because, if poorly handled, four-times leverage on an equity index can feasibly (and maybe easily) nearly wipe out one's entire wealth.

SPYU's goal is to deliver four times the daily return of the S&P 500 (SPY). This means that, if the ETN existed in March 2020, during the thick of the COVID-19 stock market crisis, SPYU would have lost (1) nearly half of its value on a single day, March 16, and (2) a total of 89% from the February 19 peak to the March 23 trough.

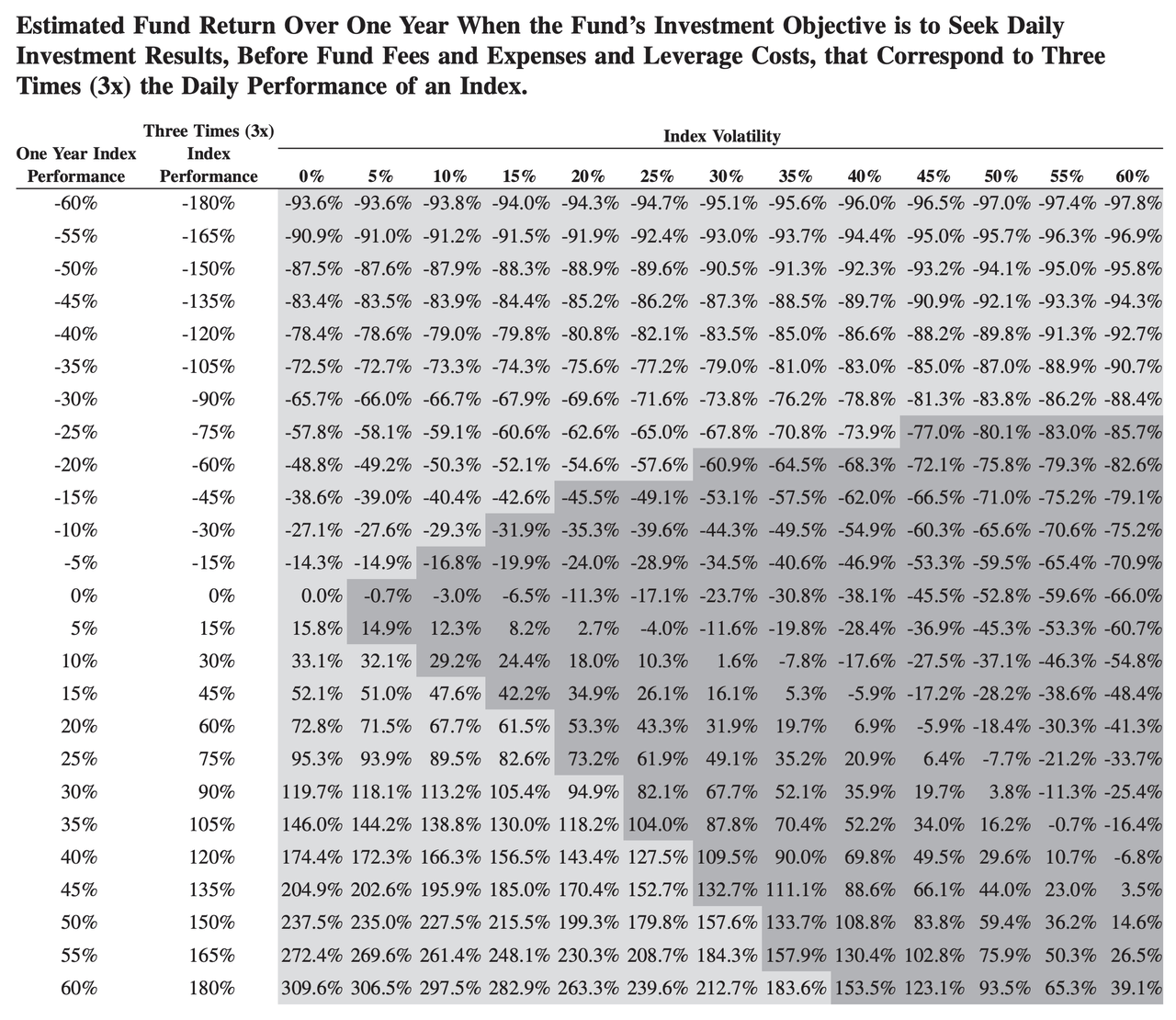

Worth noting, over the long run, SPYU will not necessarily produce four times the return of the S&P 500. In fact, assuming even mild volatility in the market, SPYU is virtually guaranteed to deliver less than that, maybe by quite a bit. This is the case primarily because of a phenomenon known by a few different names, including volatility drag. On a three-time leveraged fund, the table below illustrates what an investor might expect to earn at different levels of volatility. For a four-time leveraged fund, the impact of volatility decay would be even more pronounced.

For the reasons above, maybe it is better if the majority of individual investors stay away from SPYU. Those willing to use the fund as a relatively small piece of a bigger puzzle in which other assets and asset classes are held alongside the leveraged ETN may instead choose to keep reading.

My case for owning SPYU

One Seeking Alpha author has argued for using SPYU tactically in an attempt to ride the upside off of a relative low (i.e., buying dips). While I respect the approach, I am rarely confident enough in my ability to time entries and exits and would be particularly uneasy about doing so with a four-time leveraged ETN.

Rather, I think that SPYU can be best used as part of a stacked-return strategy - that is, as a tool to roughly replicate the performance of the S&P 500 at close to 100% allocation while freeing up plenty of capital to invest in other assets.

Because I am a fan of combining investment instruments whose returns tend to have low or even negative correlations relative to each other, allocating 20% of one's portfolio to SPYU, 60% to a treasury fund like the iShares 20+ Year Treasury Bond ETF (TLT), and the remainder 20% to cash would, effectively, mimic an 80/60 stock-and-bond portfolio, minus fees and the eventual tracking error.

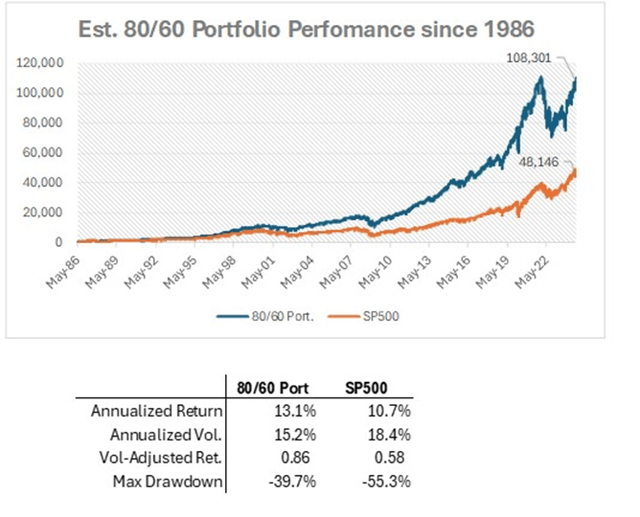

It is not too difficult to simulate how such a portfolio would have performed over the past four decades or so, had SPYU existed since then. I calculated the gains and losses of the Vanguard 500 Index Fund (VFINX) and multiplied each daily return by four, allocating to it 20% of a hypothetical portfolio originally worth $1,000. I then took the Vanguard Long-Term Treasury Fund (VUSTX), calculated the daily returns, and assigned a 60% portfolio allocation. I assumed daily rebalance for simplicity. The results are below:

DM Martins Research

Notice that the 80/60 portfolio would have outperformed the S&P 500 in virtually all meaningful metrics: higher absolute returns, better returns relative to risk, and less destructive drawdowns.

To be fair, the historical average return of 13.1% displayed above may be too high a bar to overcome, considering the secularly favorable interest rate environment in the 1980s through the 2010s, especially in the first couple of decades of that period. Still, with the 30-year yield today at more than 4%, and assuming an equity market risk premium of 6%, I expect the 80/60 portfolio to produce average annualized returns of 10.7% broken down as follows, using the capital asset pricing model (or CAPM):

- 60% of the portfolio is allocated to an asset that will likely produce annual gains of 4.2% (i.e., the treasury yield), on average.

- 80% of the portfolio is allocated to an asset that should offer gains of 4.2% (risk-free rate) plus 6% equity risk premium times a beta of one.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

Most Discussed

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10