EDF: Recent Market Performance Illustrates Dangers Of Premium Valuations

Richard Drury

The Virtus Stone Harbor Emerging Markets Income Fund (NYSE:EDF) is a closed-end fund, or CEF, that income-seeking investors may find especially appealing in their quest to achieve a high level of current income from the assets in their portfolios. The fund is quite effective at this task, as it currently boasts a 13.64% yield. That is substantially higher than any other closed-end fund that employs a similar strategy:

Fund Name | Morningstar Classification | Current Yield |

Virtus Stone Harbor Emerging Markets Income Fund | Fixed Income-Taxable-Emerging Market Income | 13.64% |

Morgan Stanley Emerging Markets Debt Fund (MSD) | Fixed Income-Taxable-Emerging Market Income | 11.47% |

Templeton Emerging Markets Income Fund (TEI) | Fixed Income-Taxable-Emerging Market Income | 9.91% |

Western Asset Emerging Markets Debt Fund (EMD) | Fixed Income-Taxable-Emerging Market Income | 10.28% |

Morgan Stanley Emerging Markets Domestic Debt Fund (EDD) | Fixed Income-Taxable-Emerging Market Income | 10.89% |

I would have preferred not to include two Morgan Stanley funds on the peer comparison table, but it was unfortunately necessary, as there are only five closed-end funds that invest in emerging market debt available on the U.S. market. This is certainly disappointing as more competition is always welcome in the space. As I noted in an article on the Voya Emerging Markets High Dividend Equity Fund (IHD), there are few remaining emerging market equity closed-end funds due to the poor performance of that asset class over the past ten years. From that article:

The 2007 collapse of Lehman Brothers sparked off a deep recession and a wave of money-printing throughout the developed world. This caused emerging markets to take something of a backseat to the asset appreciation that occurred in the U.S. markets. Over the past ten years, the iShares Core MSCI Emerging Markets ETF (IEMG), which tracks the MSCI Emerging Markets Investible Market Index, has only gained 4.34%. This obviously compares terribly to the S&P 500 Index (SP500).

As a result of the poor performance of emerging markets over the period, those funds that invested in the sector lost a lot of their former popularity and many of them were shut down.

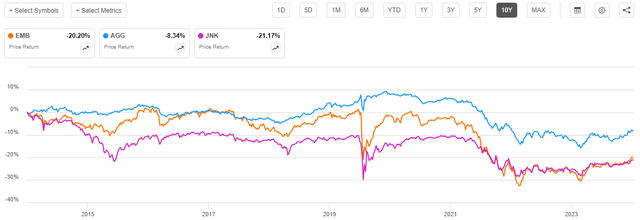

However, this only applies to emerging market equities. Emerging market bonds have actually done fairly well over the past decade. The J.P. Morgan EMBI Global Core Index (EMB) is down 20.20% over the period, which is actually better than domestic junk bonds (JNK):

Seeking Alpha

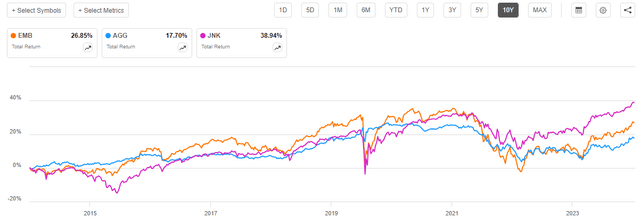

We do see though that domestic investment-grade bonds (AGG) held up much better over the past ten years and certainly exhibited much less volatility. However, we see that the yields paid out by emerging market bonds are significantly better than those offered by high-quality domestic bonds, we can clearly see that investors in these bonds overall made money and outperformed domestic investment-grade bond investors:

Seeking Alpha

However, domestic junk bonds still did the best overall. It is still rather difficult to see why there are not more closed-end funds trying to invest in this sector. It seems obvious that investment-grade bonds have not been a very good asset class over the past ten to fifteen years (and probably will not be over the next ten to fifteen years, due to the need for interest rates to remain artificially low to avoid collapsing the economy under a mountain of debt).

As regular readers may remember, we previously discussed the Virtus Stone Harbor Emerging Markets Income Fund in mid-June of this year. The global bond markets since that time have actually been fairly strong as various market participants became committed to the idea that interest rates will very shortly start coming down. This implies global central banks may shortly return the global economy to the bond bull market that has existed since the 1980s. It is worth noting though that this has only really affected developed markets. Emerging markets can generally sustain substantially higher interest rates and do not coordinate their monetary policies in accordance with the wishes of investors in wealthy nations. However, we still might expect that emerging market bonds have gone up in price both due to a desire from investors to lock in a high yield and the fact that declining interest rates weaken the U.S. dollar. We might also expect that the Virtus Stone Harbor Emerging Markets Income Fund has benefited from this.

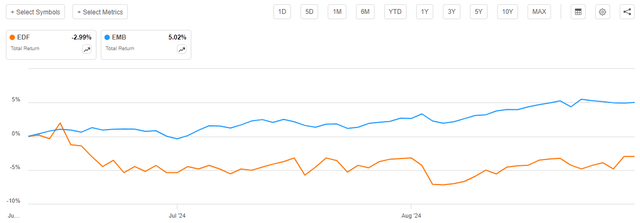

This assumption is partially correct. Emerging market bonds are up 4.11% since the previous article was published. However, the share price of the Virtus Stone Harbor Emerging Markets Income Fund is down 6.22%:

Seeking Alpha

This is quite disappointing and will almost certainly discourage potential investors from purchasing shares of this fund. After all, nobody wants to underperform an index, and the fact that a leveraged fund was unable to accomplish that task during a period in which the underlying assets were appreciating is quite discouraging. However, it is important to keep in mind that the share price performance of closed-end funds does not always match the performance of the underlying assets, so we might want to investigate further.

However, as I pointed out in my previous article on this fund:

A simple look at a closed-end fund’s share price performance does not necessarily provide an accurate picture of how investors in the fund did during a given period. This is because these funds tend to pay out all of their net investment profits to the shareholders, rather than relying on the capital appreciation of their share price to provide a return. This is the reason why the yields of these funds tend to be much higher than the yield of index funds or most other market assets.

As a result, we should include the distributions that the fund paid during a given period in any discussion of its performance. When we do this, we get this alternative chart:

Seeking Alpha

This is a better, but admittedly still disappointing performance. In particular, we see that not only did the Virtus Stone Harbor Emerging Markets Income Fund fail to match the performance of the index, but it also still handed its investors a loss. Nobody likes to take a loss in the capital markets, and certainly not during a time in which comparable things are delivering gains. As such, this is almost certainly going to discourage potential investors who might otherwise be attracted by this fund’s exceptionally high yield.

As is always the case, though, past performance is no guarantee of future results. We should take a look at the fund’s portfolios and current positioning and attempt to determine whether this disappointing performance was a fluke or if it is likely to continue. The remainder of this article will focus on this task.

About The Fund

According to the fund’s website, the Virtus Stone Harbor Emerging Markets Income Fund has the primary objective of achieving a high level of total return. This is not the most logical objective for a bond fund, given that bonds are income vehicles and do not deliver net capital gains over their lifetimes. However, it does make more sense when we consider a few aspects of the fund’s strategy. The strategy is described on the website:

The Fund’s investment objective is to maximize total return, which consists of income and capital appreciation from investments in emerging markets securities. The Fund will normally invest at least 80% of its net assets (plus borrowings for investment purposes) in emerging markets securities.

Flexibility – Managed portfolio of emerging markets fixed income securities structured to maximize total return and high current income with flexible asset allocation to local currency sovereign debt, hard currency sovereign debt, and emerging markets corporate debt.

Portfolio Diversification – Attractive total return and income potential with the possibility to diversify versus U.S. Dollar denominated assets.

There are a few things that we notice here that could give this fund the ability to generate returns from things apart from simply the coupon payments from the bonds in the portfolio. Perhaps the biggest one is the fact that it can include local currency bonds. These bonds pay out their coupons in the currency of the nation that issued the bond, or the currency used by a corporation within a given country. This provides the opportunity to earn some capital gains from the appreciation of the local currency against the U.S. dollar.

That could be a good opportunity right now, given the fundamentals of the U.S. dollar. Over the past year, the U.S. Dollar Index (DXY) has declined by 2.42%:

Seeking Alpha

We can see that the biggest declines came in the final two months of last year, and from July 2024 until the present. These were both periods in which the market was pricing for significant interest rate cuts by the Federal Reserve. That is important to keep in mind because once the Federal Reserve actually does start cutting interest rates (which is likely to start later this month), it will almost certainly drive the U.S. dollar lower. After all, the lower the amount of interest that investors can earn on U.S. dollars or U.S. dollar-equivalent assets, the less attractive it is to hold American currency versus other things. All else being equal, this should provide a tailwind for foreign and emerging market currencies going forward. That is precisely what we see in the U.S. Dollar Index.

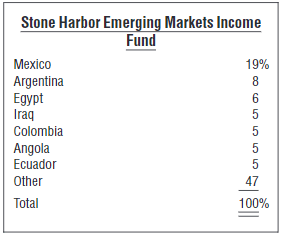

The fund’s semi-annual report states that Mexican government and corporate bonds accounted for the largest proportion of the fund’s assets as of May 31, 2024:

Fund Semi-Annual Report

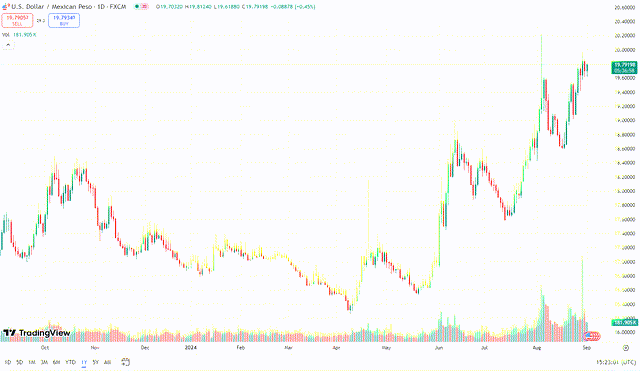

As of the end of May, Mexican securities were 19% of the fund’s total assets. Here is the one-year chart for the USD/MXN currency pair:

Trading View

In this case, an increase means that the U.S. Dollar went up in price against the Mexican peso and vice versa. Thus, we can see that any coupon payment received by the Virtus Stone Harbor Emerging Markets Income Fund that comes from a local currency Mexican bond is worth 16.20% less than the same payment made a year ago. Thus, in this case, we would have wanted the fund to be receiving U.S. dollars and not Mexican pesos. The reverse can also be sometimes true, and as indicated by the U.S. Dollar Index, there were several currencies that went up against the U.S. dollar over the past year. Thus, coupon payments made by bonds paying in those currencies now have a higher value than they did a year ago. Through this process, the Virtus Stone Harbor Emerging Markets Income Fund can sometimes earn capital gains exceeding anything that comes from the coupons or any interest rate movement. When we consider this, the fund’s total return objective actually starts to make a lot of sense.

The above example illustrates both the risks and potential rewards of investing in local currency bonds. Many investors are not comfortable with the risk that a given emerging market currency might decline rapidly in response to some event. This is why many investors often prefer hard currency bonds that pay their coupons in U.S. dollars, euros, or some similar currency that international investors are inclined to trust. The fund appears to share this preference, as currently only 17.01% of the fund’s assets are invested in local currency bonds:

Virtus Investments

The overwhelming majority of the fund’s assets are invested in sovereign bonds that pay coupons in a major world currency. This is usually U.S. dollars, but the schedule of investments in the fund’s semi-annual report does list a few bonds issued by the government of the Ivory Coast that pay their coupons in euros. This is most likely because the government of that country expected that the majority of the investors in those particular bond issues would be located in the European Union. The process effectively moves the currency risk from the investors to the issuer, and it is sometimes necessary for the issuer to obtain an interest rate that is acceptable.

It is interesting to note that the fund has slightly increased its allocation to local currency bonds since the last time that we discussed it. Please recall that at the time of our previous discussion, the Virtus Stone Harbor Emerging Markets Income Fund had 16.45% of its assets invested in sovereign local currency bonds. The fund also had 0.38% of its assets invested in corporate bonds denominated in an emerging market currency. Those two figures today are 17.01% and 0.41% respectively, so they both increased a bit over the past three months. This is something that will probably be appealing to those investors who are seeking to reduce their exposure to the U.S. dollar and benefit from a domestic currency decline. However, local currency bonds are still less than 20% of the fund’s portfolio in aggregate, so they will not have an enormous effect on the fund’s overall performance.

The fund’s investment objectives, as described in the annual report, do not limit the fund’s exposure to foreign currencies. All that it states is this:

The Fund’s investment objective is to maximize total return, which consists of income on its investments and capital appreciation. The Fund will normally invest at least 80% of its net assets (plus any borrowings for investment purposes) in Emerging Markets Securities. ‘Emerging Markets Securities’ include fixed income securities and other instruments that are economically tied to emerging market countries, that are denominated in the predominant currency of the local market of an emerging market country or whose performance is linked to those countries’ markets, currencies, economies or ability to repay loans. A security or instrument is economically tied to an emerging market country if it is principally traded on the country’s securities markets or if the issuer is organized or principally operates in the country, derives a majority of its income from its operations within the country or has a majority of its assets within the country.

…

The Fund seeks income and capital appreciation through country selection, sector selection, security selection and currency selection. In selecting Emerging Markets Securities for investment, the Fund’s subadviser will apply a market risk analysis contemplating the assessment of various factors, such as liquidity, volatility, tax implications, interest rate sensitivity, counterparty risks, economic factors, currency exchange rates and technical market considerations.

These two paragraphs strongly suggest that the fund’s potential exposure to local currency bonds can be anywhere from 0% to 100% depending on the amount of risk that the fund’s management is willing to accept. However, when we consider the problems that some emerging market currencies have had over the past ten to fifteen years, it would be very surprising if the fund ever went beyond 20%. The majority of investors in this fund are likely from developed markets, and they seem unlikely to accept too much risk.

In particular, most people who purchase bonds are rather risk-averse, so that makes it even less likely that the fund’s investors would be happy if this fund’s currency risk went up much beyond its current level. There is still the potential to profit from the likely decline in the value of the U.S. dollar over the long term, though. This is nicer than some other emerging market bond funds that do not carry out this function.

Leverage

As is the case with most closed-end funds, the Virtus Stone Harbor Emerging Markets Income Fund employs leverage as a method of boosting the effective yield and total return that it obtains from the assets in its portfolio. I explained how this works in my previous article on this fund:

In short, the fund borrows money and uses that borrowed money to purchase debt securities issued by governments and corporations in emerging market nations. As long as the yield that the fund receives from the purchased assets is higher than the interest rate that it needs to pay on the borrowed money, the strategy works pretty well to boost the effective interest rate of the fund’s portfolio. This fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates. As such, this will usually be the case.

The use of debt in this manner is a double-edged sword. This is because leverage increases both gains and losses. Thus, we want to make sure that the fund is not employing too much leverage because that would expose us to an excessive level of risk. I would generally prefer that a fund’s leverage remain under a third as a percentage of its assets for this reason.

As of the time of writing, the Virtus Stone Harbor Emerging Markets Income Fund has leveraged assets comprising 20.66% of its portfolio. This represents a significant decline over the 24.70% of assets that the fund had the last time that we discussed it. This decrease in leverage is quite surprising considering that the fund’s share price also declined fairly steeply during the period. After all, as I have explained in numerous previous articles, a share price decline gives cause to assume that the fund’s leverage actually increased.

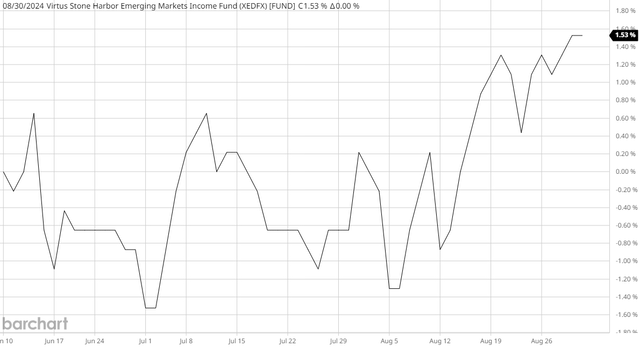

However, in this case, we should not be fooled by the fund’s steep share price decline. The fund’s net assets actually increased over the period:

Barchart

As we can see, the fund’s net asset value increased by 1.53% over the past three months. This explains the decline in leverage, as the fund’s outstanding borrowings now represent a smaller proportion of a larger portfolio. It is simply surprising that the fund’s net asset value would drop despite the underlying portfolio performing reasonably well. That does suggest that today’s entry point is better than previously, though, which we will discuss later.

Emerging market bonds tend to be more volatile than domestic bonds, so closed-end funds that invest in the sector cannot be as leveraged as most domestic fixed-income funds. Here is how the Virtus Stone Harbor Emerging Markets Income Fund compares to its peers:

Fund Name | Leverage Ratio |

Virtus Stone Harbor Emerging Markets Income Fund | 20.66% |

Morgan Stanley Emerging Markets Debt Fund | 0.00% |

Templeton Emerging Markets Income Fund | 15.41% |

Western Asset Emerging Markets Debt Fund | 26.37% |

Morgan Stanley Emerging Markets Domestic Debt Fund | 12.62% |

(All figures from CEF Data.)

As we can clearly see, the leverage ratio of the Virtus Stone Harbor Emerging Markets Income Fund is higher than most of its peers. However, it is certainly not the most leveraged fund shown on the list. This seems to suggest that the fund’s leverage is okay for its strategy.

Overall, we probably do not need to worry about the fund’s leverage too much, especially since it has come down since our last discussion. It does still pose a slightly higher risk than that of some comparable funds, though.

Distribution Analysis

The primary objective of the Virtus Stone Harbor Emerging Markets Income Fund is to provide its investors with a very high level of total return. However, most closed-end funds primarily provide their investment return through direct payments made to the investors, and this one is no exception. The fund pays a regular monthly distribution of $0.06 per share ($0.72 per share annually), which gives it a whopping 13.64% yield at the current price. This is a significantly higher yield than most of its peers.

However, the fund’s distribution has not been particularly consistent over the years. As I explained in the previous article:

Despite what some sources claim, the fund has not raised its distribution since its inception in late 2010. All of the distribution changes have been cuts. This is something that those investors who are looking to earn a safe and consistent income from their assets are probably not going to be too thrilled about, but it is not really surprising that this this would be the case given the shock that the COVID-19 pandemic had on the finances of many emerging markets and the willingness of investors to take risks.

The fund’s website lists the following distribution changes:

Date | Previous Month’s Distribution | New Distribution | Change |

02/28/2011 | N/A | $0.18 | N/A |

02/27/2020 | $0.18 | $0.17 | -5.56% |

05/28/2020 | $0.17 | $0.08 | -52.95% |

05/27/2021 | $0.08 | $0.07 | -12.50% |

11/19/2021 | $0.07 | $0.06 | -14.29% |

It is unclear why some sources show the fund’s distribution as being raised in 2022. The fund’s website shows only the above distribution changes, not the figures shown on some data sources.

As we saw in the introduction, the Virtus Stone Harbor Emerging Markets Income Fund boasts a substantially higher yield than any of its peers. This suggests that the market doubts the fund’s ability to sustain its current payout. Let us take a look at its finances to see if these fears are justified.

As of today, the most recent financial report that is available for the Virtus Stone Harbor Emerging Markets Income Fund is the semi-annual report for the six-month period that ended on May 31, 2024. A link to this document was provided earlier in this article. This is a newer report than the one that was available the last time that we discussed this fund, which is quite nice, as it should work rather well to provide us with an update on the fund’s financial performance.

For the six-month period that ended on May 31, 2024, the Virtus Stone Harbor Emerging Markets Income Fund received $8.330 million in interest along with $77,000 in dividends from the assets in its portfolio. We subtract the amount that the fund paid in foreign withholding taxes to arrive at a total investment income of $8.379 million for the six-month period. The fund paid its expenses out of this amount, which left it with $6.247 million available for shareholders. That was not sufficient to cover the $9.742 million that the fund paid out in distributions over the same period.

Fortunately, the fund was able to make up the difference through capital gains. For the six-month period that ended on May 31, 2024, the Virtus Stone Harbor Emerging Markets Income Fund reported net realized gains of $672,000 along with net unrealized gains of $13.354 million. Overall, the fund’s net assets increased by $62.181 million after accounting for all inflows and outflows over the period. It is, however, worth noting that the inflows included a capital raise that brought in $51.054 million. The fund still would have fully covered its distributions even without this new money, though.

Valuation

Shares of the Virtus Stone Harbor Emerging Markets Income Fund are currently trading at a 13.30% premium to net asset value. This is more attractive than the 15.77% average premium that the shares have had over the past month.

The large premium here means that anyone purchasing the fund’s shares today is paying substantially more than the assets underlying the fund are actually worth. This has always been something of a problem for this fund, but it is worth noting that the current premium is much smaller than the one that the fund had the last time that we discussed it. At that time, the fund’s share price premium was a whopping 21.00%. The decline of this premium thus explains how the fund’s share price can decline so severely while its net asset value actually rises.

The fund’s market performance over the past three months illustrates one concern with buying any fund at a large premium. As it does not have the assets to support its share price, large declines in price can occur regardless of the performance of the underlying portfolio. Thus, caution is always warranted when purchasing a fund at a premium.

Conclusion

In conclusion, the Virtus Stone Harbor Emerging Markets Income Fund is one of the few closed-end funds that invests in emerging market debt securities, and it is the highest-yielding of them. Perhaps surprisingly, the fund did manage to cover its distribution during the most recent six-month period. That is a rarity with any closed-end fund possessing an outsized yield. This fund is also one of the few ways to benefit from currency movements, as it does try to profit when the U.S. dollar declines against a foreign currency. This could be a pretty good long-term play, but of course, currencies are always vulnerable to short-term market sentiment.

The real problem with Virtus Stone Harbor Emerging Markets Income Fund is that this fund trades at an enormous premium. This can result in the share price declining much more than the underlying portfolio during market weakness. It can also result in share price declines during periods of market strength, as we saw over the past three months. As this fund does not have the assets to support its shares at the current level, investors are advised to be cautious.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

Most Discussed

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10