PAXS: Analyzing Recent Changes For This Highly Levered Bond Fund

Anthony Bradshaw

The PIMCO Access Income Fund (NYSE:PAXS) is a closed-end fund that income-focused investors can purchase as a method of achieving their goals. As is the case with many PIMCO funds, this one seeks to accomplish this task by investing in a portfolio that consists primarily of fixed-income securities. This can be both a good and a bad thing in today’s market environment. The good comes from the fact that fixed-income securities have generally been rising in price during recent weeks as various market participants have begun to expect that the Federal Reserve will embark on a series of interest rate cuts beginning later this month, just like several other developed-market central banks have done. However, this also means that fixed-income securities will no longer have yields that are attractive to most income seekers as they are now, so it may be necessary to move into riskier assets in order to obtain the income that is needed for daily life. In addition, as I pointed out in a recent article, all of the interest rate cuts that are likely to occur are already priced into bonds. As such, there may be limited upside for bonds from their current levels. This is mostly a problem for new investors though, not for existing ones who already have benefited from realized or unrealized capital gains.

As is the case with most PIMCO closed-end funds, the PIMCO Access Income Fund sports a much higher yield than that of most bonds in today’s market. As of the time of writing, the fund’s shares yield 11.24%, which compares quite well to the fund’s peers:

Fund Name | Morningstar Classification | Current Yield |

PIMCO Access Income Fund | Fixed Income-Taxable-Multi-Sector | 11.24% |

BlackRock Multi-Sector Income Trust (BIT) | Fixed Income-Taxable-Multi-Sector | 9.87% |

DoubleLine Yield Opportunities Fund (DLY) | Fixed Income-Taxable-Multi-Sector | 8.57% |

Guggenheim Strategic Opportunities Fund (GOF) | Fixed Income-Taxable-Multi-Sector | 14.29% |

TCW Strategic Income Fund (TSI) | Fixed Income-Taxable-Multi-Sector | 4.72% |

Fixed Income-Taxable-Multi-Sector | 11.69% |

As we can immediately see, the PIMCO Access Income Fund has a higher yield than many of its peers today. It is not the highest-yielding fund in its peer group though, which is a very good thing. As I have pointed out in the past, when the market assigns an outsized yield to a closed-end fund or other asset, it is a sign that the market doubts the fund’s ability to sustain its distribution. Therefore, such a fund may be at risk of cutting its distribution and reducing the income that it provides to its investors. That does not appear to be a problem with the PIMCO Access Income Fund, which may make it easier to sleep at night. At the same time, this fund can provide its investors with a higher level of income than other assets, so it is likely still going to be appealing to anyone who is depending on their portfolios to provide them with the income that they need to survive.

As regular readers might remember, we previously discussed the PIMCO Access Income Fund in mid-June of 2024. As already mentioned, the market environment for bonds in most developed countries has been fairly positive since that time. The European Central Bank and Bank of England have both begun to reduce their benchmark interest rate. The Bank of Canada reduced its benchmark rate for the third month in a row earlier today. The market expects that the U.S. Federal Reserve Bank will cut the federal funds rate by 25 or 50 basis points later this month. The expectations of a new monetary easing cycle have driven up bond prices due to the forward-looking nature of the market. This process has driven up the net asset value of many bond funds as well. Due to the fact that the share price of closed-end funds usually correlates somewhat with its net asset value, we can probably expect that the PIMCO Access Income Fund has also provided its investors with a fairly attractive performance.

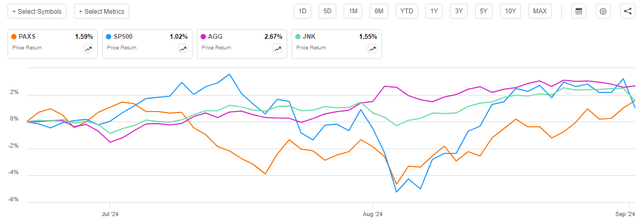

However, the PIMCO Access Income Fund has not done as well as might be expected. Its share price has only risen by 1.59% since the date that my previous article on the fund was published:

Seeking Alpha

As we can see the PIMCO Access Income Fund has managed to outperform large-cap common stocks (SP500), and it barely outperformed domestic junk bonds (JNK), but it lagged significantly behind domestic investment-grade bonds (AGG). Indeed, domestic investment-grade bonds delivered the strongest performance here. That is very rare for any bull market period, as we generally do not typically see investment-grade bonds outperforming common stocks except for during recessions. Then again, some market analysts have suggested that the United States either is currently or is about to be in a recession, which is pretty much the only way to justify the market’s current prediction of 100 basis points of interest rate cuts by the end of the year.

In any case, the share price performance of the PIMCO Access Income Fund was acceptable over the past two-and-a-half months but it was nothing amazing. However, as I stated in my previous article on this fund:

A simple look at a closed-end fund’s price performance does not necessarily provide an accurate picture of how investors in the fund did during a given period. This is because these funds tend to pay out all of their net investment profits to the shareholders, rather than relying on the capital appreciation of their share price to provide a return. This is the reason why the yields of these funds tend to be much higher than the yield of index funds or most other market assets.

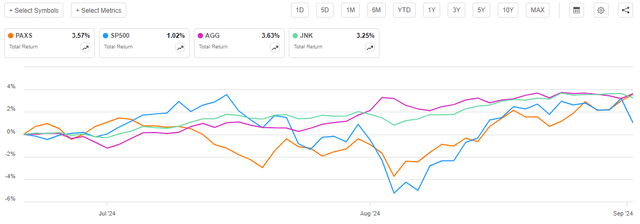

The distributions that the fund pays out represent a real investment return to the shareholders that is not reflected in the share price. As such, we need to include the distributions paid out in order to get an accurate picture of how investors in this fund actually did. When we do that, we get this alternative to the chart above:

Seeking Alpha

As we can see, the PIMCO Access Income Fund delivered a 3.57% total return over the past two-and-a-half months. This was slightly below the total return provided by investment-grade bonds, but admittedly the fund came very close to matching their performance. It still managed to beat both large-cap common stocks and junk bonds. Overall, many investors will probably be satisfied with the fund’s performance when we consider that the yield alone is likely to be attractive to most.

As two-and-a-half months have passed since we last discussed this fund, it is reasonable to assume that several things have changed. Perhaps most importantly, the fund released its annual report for the most recent fiscal year. We will want to consult this document in order to see how well it is covering its distribution. In addition, the domestic economy has deteriorated and strengthened the case for interest rate cuts. Interest rates are perhaps the most important thing to consider when investing in bonds, so this is also important. The remainder of this article will focus on updating readers on these developments.

About The Fund

According to the fund’s website, the PIMCO Access Income Fund has the primary objective of providing its investors with a very high level of current income. Bonds are, by their very nature, income vehicles so this objective makes a great deal of sense for any bond fund. The fund’s description of its strategy makes it very clear that this is a bond fund:

The Fund utilizes an opportunistic approach to pursue high conviction income-generating ideas across global credit markets to seek current income as a primary objective and capital appreciation as a secondary objective.

In managing the fund, PIMCO will employ an active approach to allocation among multiple fixed income sectors based on, among other things, market conditions, valuation assessments, economic outlook, credit market trends and other economic factors. With PIMCO’s macroeconomic analysis as the basis for top-down investment decisions, including geographic and credit sector emphasis, PIMCO will manage the Fund with a focus on seeking income generating investment ideas across fixed income sectors, including opportunities in developed and multiple emerging global credit markets. PIMCO may choose to focus on particular countries/regions, asset classes, industries and sectors to the exclusion of others at any time and from time to time based on market conditions and other factors. The relative value assessment within fixed income sectors will draw on PIMCO’s regional and sector specialist insights.

The Fund seeks to achieve its investment objectives by utilizing a dynamic asset allocation strategy among multiple sectors in the global public and private credit markets, including corporate debt, mortgage-related and other asset-backed instruments, government and sovereign debt, taxable municipal bonds and other fixed-, variable-, and floating-rate income-producing securities of U.S. and foreign issuers, including emerging market issuers and real estate-related investments. The Fund may invest without limitation in investment-grade debt securities and below investment grade debt securities, including securities of stressed, distressed or defaulted issuers.

As we can see, this description makes numerous mentions of the fund investing in fixed-income securities, bonds, and other credit instruments. In addition, it makes no mention of equities, derivatives, or any instrument that is not created due to one party owing money to another. This description clearly, therefore, matches that of a bond fund.

Its portfolio composition also makes it clear that the PIMCO Access Income Fund invests in bonds. The fund’s most recent annual report states that the fund had the following asset allocation on June 30, 2024:

Asset Type | % of Net Assets |

Loan Participations and Assignments | 31.2% |

Corporate Bonds and Notes | 33.6% |

Municipal Bonds and Notes | 2.5% |

Non-Agency Mortgage-Backed Securities | 52.0% |

Asset-Backed Securities | 34.6% |

Sovereign Issues | 1.6% |

Common Stocks | 10.5% |

Warrants | 0.0% |

Preferred Securities | 0.1% |

U.S. Treasury Bills | 1.0% |

Enhanced Cash Management Fund | 11.1% |

As expected, we do not see too much here other than debt securities. There is, however, a 10.5% allocation to common stocks. Many of these appear to be shares of highly distressed or bankrupt companies:

Company | Current Dividend Yield |

Steinhoff International Holdings NV (OTC:STHHF) | N/A |

Banca Monte del Paschi di Siena SpA (OTCPK:BMDPF) | 4.98% |

Market Garden Dogwood LLC | Unknown – Private |

Amsurg Equity (AMSG) | N/A |

Syniverse Holdings (SVR) | N/A |

ADLER Group SA (OTC:ADPPF) | N/A |

West Marine | Unknown – Private |

The only one of these companies that pays a dividend is Banca Monte del Paschi di Siena, and Seeking Alpha’s quote page for that company contains no recent articles and only two from 2014 advising investors to avoid it:

Seeking Alpha

The remainder of these companies are mostly penny stocks that trade over the counter. In other words, these are not the kinds of companies that risk-averse income-seeking investors would ordinarily be interested in. As such, the fact that the PIMCO Access Income Fund has 10.5% of its net assets invested in these companies could be quite concerning to many.

However, it is not uncommon for a bond fund to sometimes accumulate equity securities in its portfolio. In many cases, these equity securities will be issued by bankrupt or defunct entities. The reason for this is quite simply that the fund held the debt of a company that defaulted on its credit obligations. As part of its bankruptcy proceedings, the company swapped its debt for equity, which resulted in the creditors receiving equity securities. This was not sufficient to save the company, though, and today there are virtually no potential buyers for the equity. Thus, the fund ends up with some equities that it cannot get rid of and which already have fairly large losses either realized or unrealized. These securities are not a core part of the fund’s investment portfolio, but it simply has to list all of its holdings on the schedule of investments.

We do see a few changes in the fund’s schedule of investments that took place during the December 31, 2023, to June 30, 2024, period. These changes are summarized in this table:

Asset Type | % of Net Assets on December 31, 2023 | % of Net Assets on June 30, 2024 | % Change |

Loan Participations and Assignments | 27.1% | 31.2% | +4.10% |

Corporate Bonds and Notes | 28.5% | 33.6% | +5.1% |

Municipal Bonds and Notes | 2.9% | 2.5% | -0.4% |

Non-Agency Mortgage-Backed Securities | 56.8% | 52.0% | -4.8% |

Asset-Backed Securities | 33.0% | 34.6% | +1.6% |

Sovereign Debt | 0.9% | 1.6% | +0.7% |

Common Stock | 7.6% | 10.5% | +2.90% |

Warrants | 0.0% | 0.0% | N/A |

Preferred Stock | 0.1% | 0.1% | N/A |

Real Estate Investment Trust Common Stock | 0.5% | 0.0% | -0.5% |

United States Treasury Bills | 1.6% | 1.0% | -0.6% |

Money Market Funds | 14.1% | 11.1% | -3.0% |

Perhaps the biggest change that we see here is that the fund significantly increased its allocation to floating-rate loans and fixed-rate corporate bonds. This was at least partially funded by the reduction in cash-equivalent securities, which actually makes a certain amount of sense. While the Federal Reserve’s next move was not entirely certain during most of the period in question, many market participants believed that it was a question of when, and not if, the central bank would reduce interest rates. During periods of falling rates (or ultra-low interest rates), it does not make sense to hold more cash than is needed. The interest rate earned by cash-equivalent securities did not change during the period in question, but it still made sense to begin to deploy capital as there were opportunities to lock in yields that were well above the 5.25% paid by most money market funds. In particular, junk bonds offered opportunities to earn higher yields. The fund’s management, realizing that it would be more difficult to obtain very high yields once the monetary easing cycle began, may have deployed some capital in order to lock in a yield that would be considered by most fixed-income investors today.

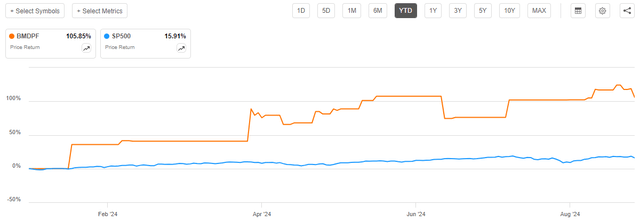

We also see a significant increase in the fund’s allocation to common stocks, which is a bit harder to explain due to the fact that this fund is not really buying common stock. After all, it appears that most of the shares that it currently has were obtained through bankruptcy settlements and the like. However, we can see one reason for the increase in the fund’s common stock allocation by looking at the recent share price performance of Banca Monte dei Paschi di Siena. As we can see here, the shares of this company are up a whopping 105.85% year-to-date:

Seeking Alpha

As that performance would easily surpass any bond that this fund is holding, the allocation to common stocks would rise simply due to the outperformance of this one common stock. The common stock weighting increase was probably not caused by the fund actually borrowing money to purchase common stocks, nor was it caused by the fund selling bonds in order to purchase common stocks.

Leverage

As is the case with most closed-end funds, the PIMCO Access Income Fund employs leverage as a method of boosting the effective yield and total return that it earns from the assets in its portfolio. I explained how this works in my previous article on the fund:

In short, the fund borrows money and then uses that borrowed money to purchase bonds and similar fixed-income assets. As long as the purchased assets have a higher yield than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. As this fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates, that will normally be the case. With that said though, this strategy is much less effective today with market rates above 5% than it was three years ago when rates were just barely above 0%.

However, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund is not employing too much leverage since that would expose us to an outsized amount of risk. I generally do not like to see a fund’s leverage exceed a third as a percentage of its assets for this reason.

As of the time of writing, the PIMCO Access Income Fund has leveraged assets comprising 42.86% of its assets. This is a slight improvement from the 43.35% leverage that the fund had the last time that we discussed it. Ordinarily, we expect a fund’s leverage to decline when its share price rises, due to the simple fact that usually a rising share price means that the fund’s portfolio gets larger.

This was very much the case here. This chart shows the fund’s net asset value from June 20, 2024 (the date that my previous article on this fund was published) until today:

Barchart

As we can clearly see, the fund’s net asset value has increased by 1.99% over the period. This means that the portfolio on a per-share basis is larger than it is today. All else being equal, this will cause the fund’s borrowings to represent a smaller proportion of the portfolio than previously. This is exactly what we appear to be seeing.

However, we note that the fund’s leverage is substantially above the one-third of assets maximum that we would ordinarily prefer to see. It is also higher than any of its peers today:

Fund Name | Leverage Ratio |

PIMCO Access Income Fund | 42.86% |

BlackRock Multi-Sector Income Trust | 35.49% |

DoubleLine Yield Opportunities Fund | 18.40% |

Guggenheim Strategic Opportunities Fund | 17.89% |

TCW Strategic Income Fund | 0.00% |

Western Asset Diversified Income Fund | 31.38% |

(all figures from CEF Data)

The last time that we discussed the PIMCO Access Income Fund, it was also the most leveraged fund of any of its peers by a fairly significant margin. At the time, I made the following observation:

This chart confirms that the PIMCO Access Income Fund employs substantially more leverage in the pursuit of its investment strategy than any of its peers. This means that investors in this fund are exposed to substantially more risk than shareholders who opt to purchase a peer fund instead, as investors in the PIMCO Access Income Fund will almost certainly wind up taking more losses than they would feel comfortable with in the event of a bond market correction.

This statement holds true today. As leverage increases volatility, this fund’s net asset value will likely exhibit greater swings than a more conservatively leveraged fund. This remains true even though the fund’s leverage has decreased somewhat from the last time that we discussed it.

Distribution Analysis

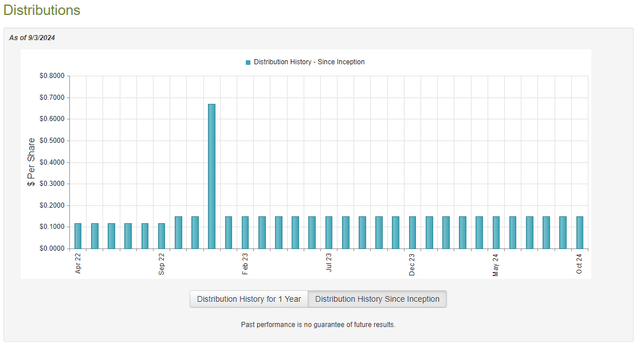

The primary objective of the PIMCO Access Income Fund is to provide its investors with a very high level of current income. To that end, the fund pays a monthly distribution of $0.1494 per share ($1.7928 per share annually). This gives the fund a very attractive 11.24% yield at the current price.

Unlike most bond funds, the PIMCO Access Income Fund has been remarkably consistent with respect to its distributions over its history:

CEF Connect

As I stated in the previous article:

This stands in stark contrast to the distribution history of most fixed-income funds. After all, the majority of the funds in this sector that are not heavily weighted to floating-rate loans have had to reduce their distributions due to the losses that they took in 2022. The fact that this one has not had to reduce its payout is something that we should therefore investigate, as it seems quite strange that it would be able to pull off a feat that few other funds were able to accomplish.

The fund has not changed its distribution since our previous discussion, so there is nothing to update there. However, it did recently release its annual report for the full-year period that ended on June 30, 2024 (linked earlier) so we should take a look at this document and see how well the fund is covering its distribution.

For the full-year period that ended on June 30, 2024, the PIMCO Access Income Fund received $98.908 million in net interest and $4.466 million in dividends net of foreign withholding taxes. When combined with a small amount of income from other sources, the fund reported a total investment income of $105.853 million for the full-year period. It paid its expenses out of this amount, which left it with $59.880 million available for the shareholders. That was not sufficient to cover the $78.945 million that the fund paid out in distributions during the period.

Fortunately, the fund was able to make up the difference through capital gains. For the full-year period that ended on June 30, 2024, the PIMCO Access Income Fund reported net realized losses of $21.757 million but these were offset by $47.978 million in net unrealized gains. Overall, the fund’s net asset value increased by $8.744 million after accounting for all inflows and outflows during the period.

Therefore, we can see that the PIMCO Access Income Fund did manage to cover its distributions for the most recent full-year period. However, it was only able to do so because of unrealized capital gains. That can be concerning, as unrealized capital gains can be easily erased by any market correction. For the time being though, such a market correction does not seem particularly likely as recent economic data suggests that we will see central banks follow through on the interest rate cuts that are priced into both domestic and many foreign bonds. As a rate hike from any developed market central bank is unlikely in the near future, a shock that causes yields to rise does not appear to be imminent. Therefore, for now, we probably do not need to worry too much about the fund’s distribution being reduced.

Valuation

Shares of the PIMCO Access Income Fund are currently trading at a 4.56% premium on net asset value. This is significantly more expensive than the 2.24% premium that the fund has had on average over the past month, and even that price results in investors paying more for the fund’s assets than they are actually worth. As such, the current valuation seems rather high.

Conclusion

In conclusion, the PIMCO Access Income Fund is an interesting closed-end fund that provides its investors with a high level of income by investing in fixed-income assets from all over the world. That is a pretty attractive proposition, as it allows investors to get exposure to opportunities that are located outside of the United States. The fund does have limited exposure to other assets though, but it appears to be focusing on bonds and other debt instruments. The fund also has one of the highest yields available in the sector and appears to be fully covering it.

The fund does have a very high level of leverage though, which could be concerning to some potential investors. It is also very expensive right now.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

Most Discussed

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10