The Market Thinks Argan, Inc. Earnings Were Incredible, I Agree

- Argan, Inc. operates an engineering and construction conglomerate providing services primarily in the energy sector.

- Its last earnings report caused it to soar 25%+. This article looks at what in the report caused the jump.

- I also cover risks to the buy thesis and other potential headwinds and tailwinds for AGX.

bjdlzx/E+ via Getty Images

Introduction

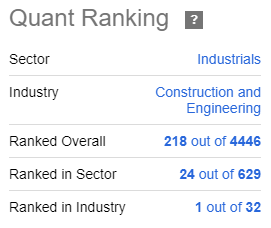

Argan, Inc. (NYSE:AGX) is a construction and engineering conglomerate primarily operating in the energy construction sector. AGX is headquartered in Rockville, MD, and operates domestically in the US, as well as abroad in Ireland and the United Kingdom. It has recently become a universal darling, earning praise from Wall Street, quant models, and Seeking Alpha analysts.

Seeking Alpha Seeking Alpha

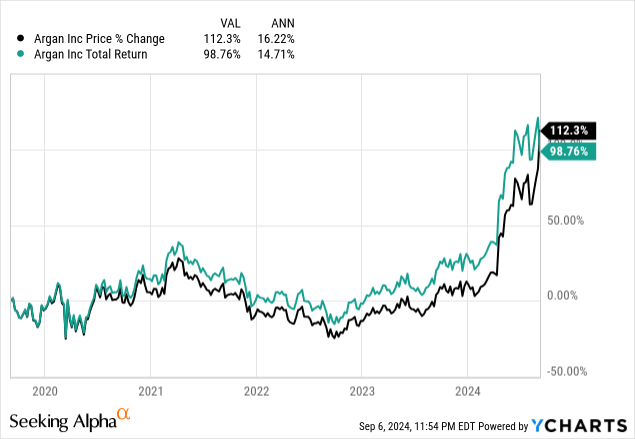

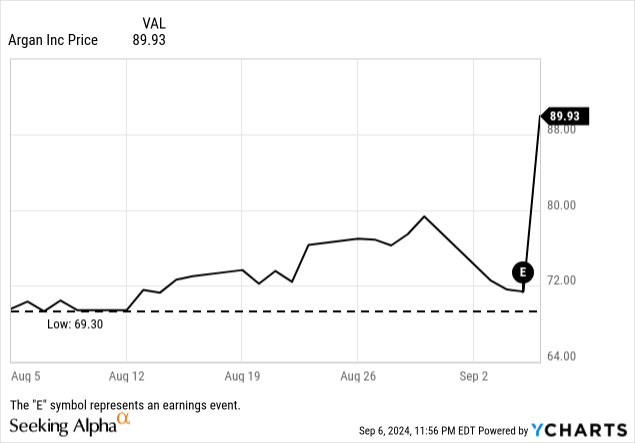

For all those who have recommended AGX, it's paid off. As of the time of writing, they are at an all-time high after a very positive earnings report on 9/5.

AGX Charts

Here are the 5-year and 1-month charts.

What's so Impressive?

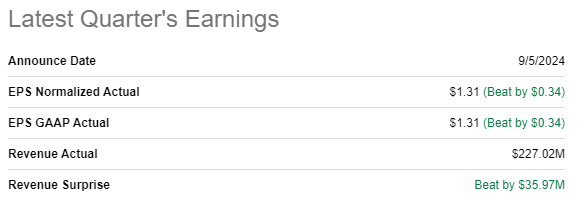

What we learned at the earnings call was surprising, as AGX beat its expectations handily across the board.

Seeking Alpha

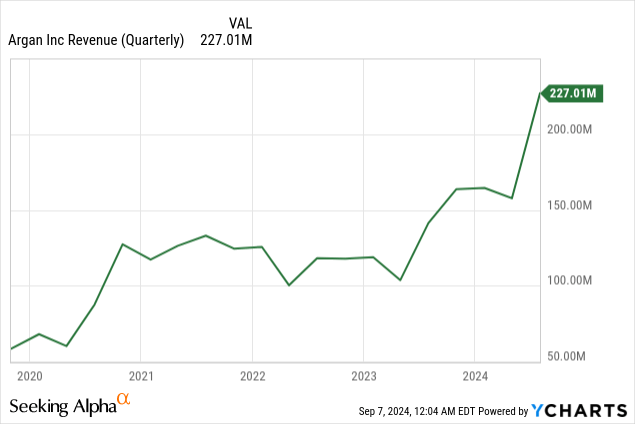

Revenue is Up

Revenue has hit a five-year high, built on the strength of their book and healthy backlog of projects to keep business churning.

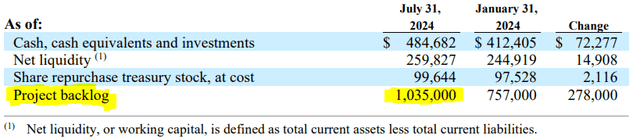

The Backlog is Churning and Building

Speaking of the backlog, it has grown YoY, and is now sitting at 1,035,000 projects waiting to begin.

Argan, Inc.

Here is what CEO David Watson commented regarding the backlog:

The Company closed the second quarter with backlog of $1.0 billion, which reflects an increase from last quarter of approximately $210 million, and includes $570 million of renewable projects...Our pipeline remains strong and we are confident that our energy-agnostic capabilities and proven success leave us well positioned to compete effectively for the growing number of projects coming to market.

I like the energy-agnostic approach because it allows Argan to tap into infrastructure funding more broadly, and not be pigeon-holed into a niche that may or may not pay off. So far, it's paying off.

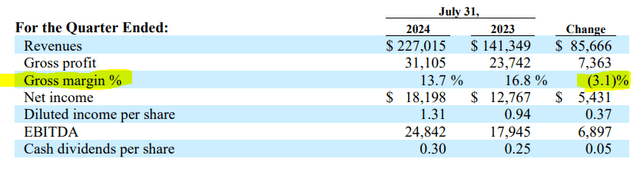

Margins are Down, Profits are Up

Even though gross margin shrunk YoY, the shrinkage was minimal, and the massive jump in profits and EBITDA seems to have made up for it.

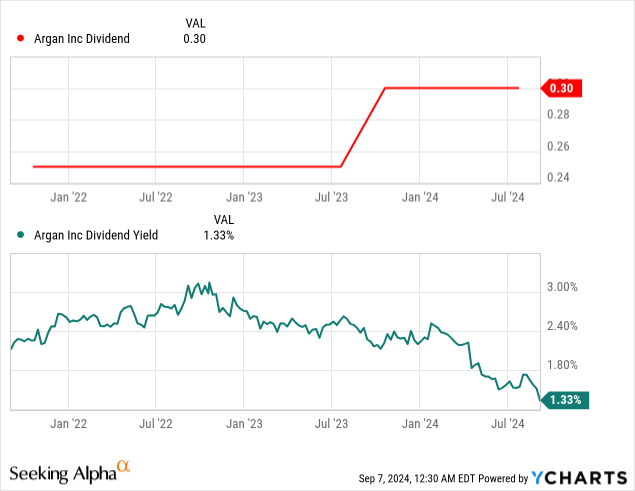

Good news for dividend investors, the dividend is being raised another nickel. This is good for AGX, as it shows confidence from the board that they are able to continue to deliver the current dividend, and some, and will continue to do so into the future. Note that even though the dividend is up, the price has risen so far that the current yield is low for the sector.

Future Catalysts

Even though AGX just made a jump, it may still have positive catalysts ahead of it that we can expect to continue to give them business:

- Elective vehicle adoption requires extending and restructuring some power grids, especially in rural areas

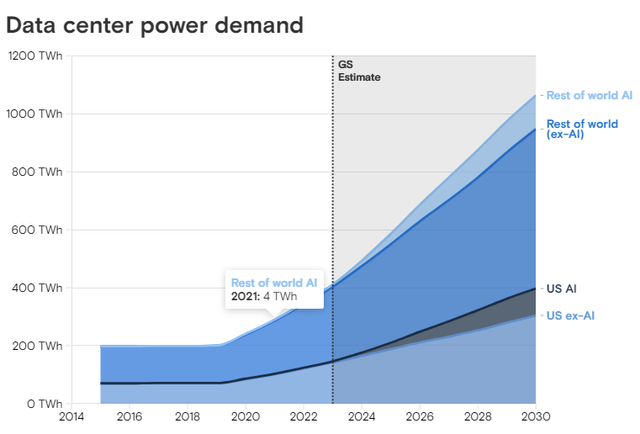

- Data centers are a new source of demand, with the AI revolution set to expand power demand by up to 160% in the next six years

Goldman Sachs

The Real Winner of the Election

One of the interesting shifts in politics has been the bipartisan support for infrastructure spending that has coalesced into actual policy. The Inflation Reduction Act increased spending on infrastructure tremendously, and much of it is in energy.

This policy is one that the Biden administration is very proud of, as evidenced by their repeated use of it as a campaign token. It is clear that, if Harris is elected in November, she will push similar policies such as the IRA and the CHIPS Act, which put government spending into microchip production (another massive energy consumer for AGX to provide solutions for!)

Former President Trump had no issue pushing his own infrastructure successes, but has very recently said that he wants to create a sovereign wealth fund in the US dedicated to infrastructure spending. This would be a tremendous boon for companies like AGX, who rely on manufacturing plants and data centers for their main source of demand.

Biden too has announced a similar plan aimed at increasing investment in the US manufacturing and technology sectors.

Political affiliations aside, AGX stands to gain no matter who wins. Both sides want to pump as much money as they can into infrastructure investment. The re-shoring that will take place once the new fabs and factories are built should bring about tremendous demand for energy and new pipelines, solar arrays, and power plants.

Risks to Consider

Valuations are now rather high compared to where they were before. If you are starting a position now, know that there is a lot of room to fall from here in the short term if there is pain in the markets.

Although, my colleague Shri Upadhyaya makes the case that AGX's returns are uncorrelated enough with the market to make it an "all-weather" holding.

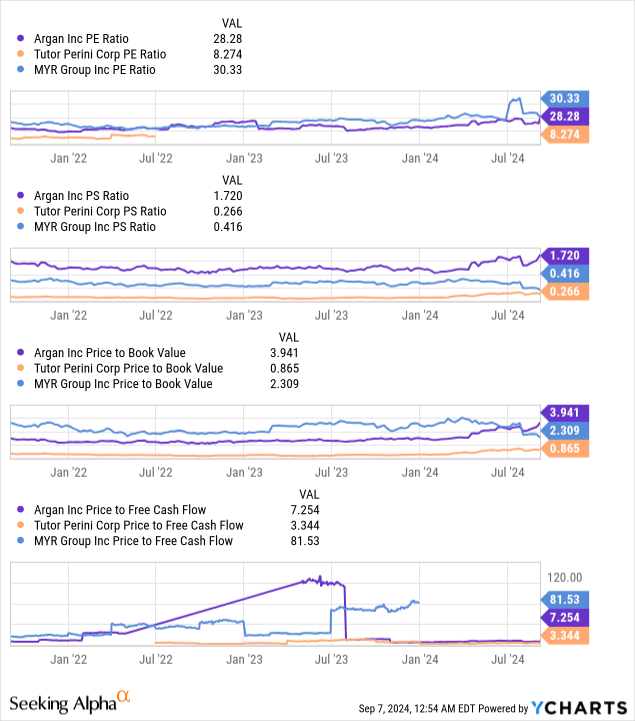

Compare its pricing ratios to similarly sized companies in the sector and we see that there is some real competition for "cheap" firms in construction.

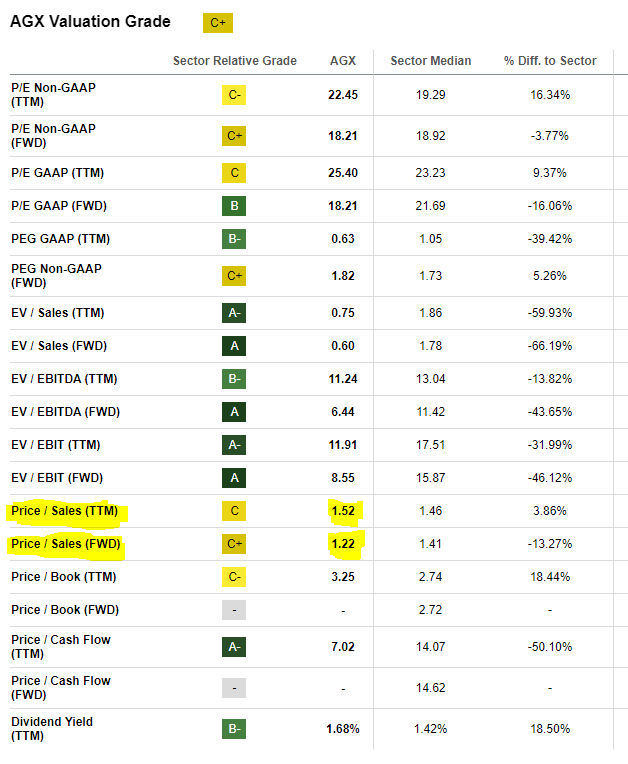

SA Quant gives AGX a C+ in this category, its lowest mark. I agree with SA Quant that the price to sales ratio should be a reason for investors to tighten their position sizing.

Seeking Alpha

Conclusion

Argan, Inc. (AGX) had a stellar earnings report and its shareholders were rewarded with a 25% jump the next day. AGX's revenue and profit soared, impressing investors. I believe that AGX still has a strong growth narrative ahead of it, even though some of its pricing ratios are a little rich.

I am considering a position in AGX for my equity portfolio. After this jump, I am going to scale back my initial recommendation. I recommend no more than a 5% allocation for aggressive investors, and no more than a 2% allocation for conservative investors. AGX is poised to benefit from current secular trends and its management has proven their recent abilities to continue revenue and profit increases.

This is a stock that feels easy to be bullish on. Beware of that feeling. It may mean there is something too good to be true at play; I don't see it. Let me know in the comments if you do.

Thanks for reading.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

Most Discussed

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10