HYT: This Is A Decent Junk Bond Fund, But It Does Not Deserve Its Current Premium

Anthony Bradshaw

The BlackRock Corporate High Yield Fund (NYSE:HYT) is a closed-end fund that has proven itself to be a popular choice among those investors who are seeking to earn a very high level of income from the assets that they already possess. There are a lot of reasons why one might need to earn an income from their portfolios right now. In particular, retirees frequently need income to pay their monthly bills, as Social Security payments alone are usually not enough to enjoy the lifestyle that many retirees who had higher incomes during their working years would really like to have. Admittedly, it is possible to simply sell a few common stocks whenever one needs some money, but that also exposes an investor to market risk. As Charles Smith, a former quantitative stock market analyst, pointed out on September 06, 2024, the high level of volatility in the stock market that we have seen since the start of August is not a sign of a healthy market. In addition, the fact that only a handful of stocks have been responsible for the majority of the total returns of the S&P 500 Index (SP500) over the past year is a sign that the market lacks breadth, which is similarly unhealthy. As such, we see signs that the market may be about to enter a period of prolonged weakness, and such an environment would not really be conducive to generating income by selling stocks every month to support retirement. It would be much better to own something that makes a regular monthly payment that can be used as needed income.

The BlackRock Corporate High Yield Fund does fairly well at the provision of income, as the fund yields 9.44% at today's share price. That is substantially above the 1.27% trailing twelve-month yield of the SPDR S&P 500 ETF Trust (SPY), which is the most popular exchange-traded product tracking large-cap stocks. Here is how the yield of the BlackRock Corporate High Yield Fund compares to that of its immediate peers:

Fund Name | Morningstar Classification | Current Yield |

BlackRock Corporate High Yield Fund | Fixed Income-Taxable-High Yield | 9.44% |

Allspring Income Opportunities Fund (EAD) | Fixed Income-Taxable-High Yield | 8.91% |

BNY Mellon High Yield Strategies Fund (DHF) | Fixed Income-Taxable-High Yield | 8.33% |

Fixed Income-Taxable-High Yield | 8.65% | |

Invesco High Income Trust II (VLT) | Fixed Income-Taxable-High Yield | 10.26% |

Neuberger Berman High Yield Strategies Fund (NHS) | Fixed Income-Taxable-High Yield | 13.13% |

As we can see, the BlackRock Corporate High Yield Fund does not offer the highest yield available in the closed-end junk bond space, but it still compares reasonably well to that of its peers. This is a good sign because the fact that the fund does not have an outsized yield suggests that the market believes that the fund's current distribution is sustainable. Investors in this fund will still end up receiving a higher level of income than they would with some other options, however.

As regular readers might remember, we previously discussed the BlackRock Corporate High Yield Fund in November 2023. The bond market since that time has been all over the place, as bonds experienced a raging bull market during the final two months of last year before various market participants began to realize that the economic conditions in the United States did not justify six or more interest rate cuts in 2024. Bonds fell for most of the first half of this year, although junk bonds held up better than investment-grade bonds, due mostly to bond investors seeking to lock in high coupon yields before the central bank eventually reduces interest rates. Finally, in the latter half of the summer, investors once again started bidding up bond prices in response to a dovish pivot by the Federal Reserve in July and August. As such, we might expect that the shares of the BlackRock Corporate High Yield Fund have been range-bound since our last discussion, with a certain amount of price movement within that range.

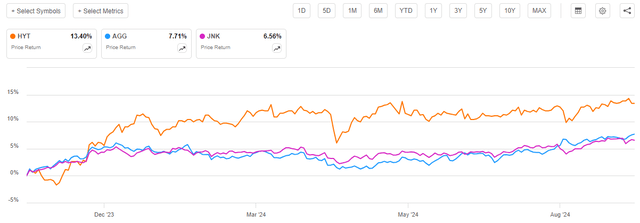

This assumption is somewhat correct. As we can see here, the shares of the fund shot up in November and December but have been flat over most of this year:

Seeking Alpha

We also see that the shares of the BlackRock Corporate High Yield Fund have outperformed both the Bloomberg U.S. Aggregate Bond Index (AGG) and the Bloomberg High Yield Very Liquid Index (JNK), which track domestic investment-grade and domestic junk bonds, respectively. This is not unexpected, considering that the fund's leverage would ordinarily result in its portfolio appreciating more rapidly than the indices during periods in which bond prices increase (as was the case in November and December 2023). Overall, most investors will probably be reasonably pleased with the fund's performance since our last discussion, since we all like to outperform the indices.

It is worth noting, though, that investors in this fund actually did better over the period than the above price chart suggests. As I explained in a recent article:

A simple look at a closed-end fund's price performance does not necessarily provide an accurate picture of how investors in the fund did during a given period. This is because these funds tend to pay out all of their net investment profits to the shareholders, rather than relying on the capital appreciation of their share price to provide a return. This is the reason why the yields of these funds tend to be much higher than the yield of index funds or most other market assets.

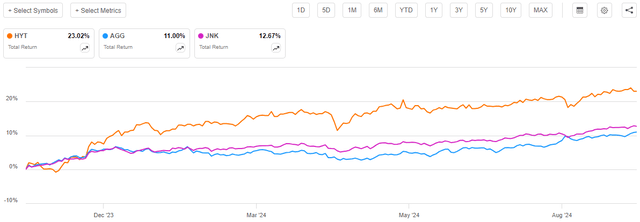

This is a particularly relevant point when it comes to bond funds because bonds deliver an outsized proportion of their total returns in the form of direct payments to their owners. As such, when we include the distributions paid out by this fund and the bond indices, we can clearly see that investors did much better over the past ten months than we might think:

Seeking Alpha

As we can see, investors in the BlackRock Corporate High Yield Fund have benefited from a 23.02% total return since mid-November 2023. This is substantially better than the total returns offered by the two bond indices, although anyone who purchased any of these three assets on the date of our previous discussion on the fund has realized a double-digit return. There are few investors who will be overly disappointed with this, as the BlackRock Corporate High Yield Fund has done substantially better than the stock market's average return over most ten-month periods.

However, past performance is no guarantee of future results and indeed, with this fund, it does appear that the best is behind us. After all, the only way to make money on bond appreciation today is if the Federal Reserve cuts interest rates by more than the market currently expects, and that seems unlikely. The fund still possesses a yield that is reasonably attractive to most, however, and by itself, it should satisfy the needs of an average person if it proves to be sustainable. This article will specifically focus on the changes that have occurred to this fund and in the macroeconomic environment since our previous discussion, and provide an updated analysis of the fund's finances.

About The Fund

According to the fund's website, the BlackRock Corporate High Yield Fund has the primary objective of providing its investors with a very high level of current income. This makes a lot of sense for a bond fund, and the description of the fund that is provided on the website makes it very clear that this is a bond fund. Here is the description:

BlackRock Corporate High Yield Fund, Inc.'s primary investment objective is to provide shareholders with current income. The Trust's secondary objective is to provide shareholders with capital appreciation. The Trust seeks to achieve its objectives by investing, under normal market conditions, at least 80% of its assets in domestic and foreign high yield securities, including high yield bonds, corporate loans, convertible debt securities and preferred securities which are below investment grade quality. The Trust may invest directly in such securities or synthetically through the use of derivatives.

This description makes it quite clear that the fund invests at least 80% of its assets into debt securities that are backed by the creditworthiness of below-investment-grade companies. The fact that the fund can invest in corporate loans (which are not technically bonds), convertible securities, and preferred securities does not change the fact that this is a junk bond fund. After all, most junk bond funds reserve themselves the right to purchase such securities, but they usually end up representing a very small proportion of the portfolio. This is the case with this fund, which we can see by looking at the asset allocation that is provided in the fund's schedule of investments from its semi-annual report.

The semi-annual report states that the BlackRock Corporate High Yield Fund had the following asset allocation on June 30, 2024:

Asset Type | % of Net Assets |

Asset-Backed Securities | 0.2% |

Common Stocks | 0.8% |

Corporate Bonds | 108.8% |

Floating Rate Loan Interests | 15.4% |

Fixed-Income Funds | 3.4% |

Preferred Securities | 3.9% |

Curiously, the fund's schedule of investments does not list any cash or cash-equivalent assets. This is a bit strange because most funds prefer to keep a small amount of cash on hand to pay distributions or take advantage of opportunities in the market as they arise. This fund does not appear to be doing so, and as such, it is probably relying on a revolving line of credit or something similar to make the regular monthly payments to its investors. This is similar to how some investors will take a margin loan against their stock holdings whenever they desire cash for some reason. This is not necessarily a bad way to do things, especially in times like today, as interest rates are likely to drop in the near future and bonds rallied during much of the year. However, there are some risks associated with this strategy, as it might result in the fund borrowing more money than we are really comfortable with as investors.

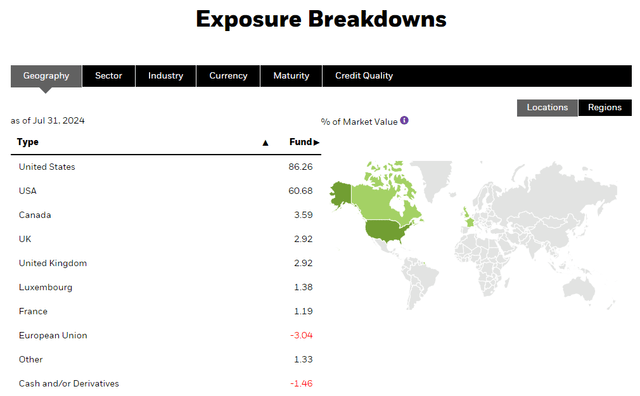

The fund's website confirms the above statement that this fund has no cash and is relying on some sort of revolving credit line to obtain cash whenever its management needs to finance a purchase or pay a distribution. The website shows the following country allocation for the fund:

BlackRock

We will discuss the country allocation in just a bit, but for now, please notice that the website states that the fund has a -1.46% allocation to cash and/or derivatives. This means that the fund actually has a debit balance in a revolving line of credit or a margin balance. It owes cash to another party, which might be BlackRock itself. Thus, if the securities in this fund do not appreciate going forward, the interest that it needs to pay on this debit balance could serve as a drag on the fund's performance.

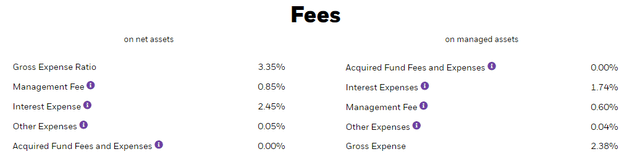

The fund had an interest expense of 2.45% on net assets for the full-year 2023 period, as shown here:

BlackRock

As we can clearly see, the fund's interest expenses were by far the largest expense borne by shareholders during the most recent fiscal year. Presumably, this increased a bit during the first six months of the 2024 fiscal year. The fund's semi-annual report states that its gross annualized expense ratio was 3.56% of net assets for the first six months of 2024. That is higher than the 3.35% gross expense ratio on net assets that the fund reported in 2023. This fund's management fee is not really that high and its other expenses are negligible, so the increase in the fund's gross expense ratio must be caused by higher interest expenses. That makes sense, too, since interest rates were lower during the first half of 2023 than they are today. After all, the most recent federal funds interest rate hike was in July 2023.

We notice in the description on the website that the BlackRock Corporate High Yield Fund invests in securities issued by both domestic and foreign entities. This is likely to be appealing to those investors for whom reducing their exposure to the United States is a priority. However, as we saw in the geographic exposure above, this fund is not taking advantage of that option to any great degree. As of July 31, 2024, the fund's website states that it had 86.26% of its total assets invested in the United States. Admittedly, though, the website appears confused on this because it lists the United States twice and assigns two different weightings - 86.26% and 60.68% - to the country. It is possible that the 60.68% figure actually refers to the tiny percentage of the portfolio that is invested in common stocks. Here are the common stocks held by the fund:

Company Name | Country of Origin | % of Net Assets |

JELD-WEN Holding (JELD) | USA | 0.1% |

Ardagh Metal Packaging S.A. (AMBP) | USA* | 0.0% |

SunPower Corp. (OTC:SPWRQ) | USA | 0.0% |

Nine Energy Service (NINE) | USA | 0.0% |

Avantor (AVTR) | USA | 0.1% |

Constellium SE (CSTM) | France | 0.2% |

Kcad Holdings I Ltd. | United Kingdom | 0.0% |

NGL Energy Partners (NGL) | USA | 0.1% |

ADLER Group (OTC:ADPPF) | Germany | 0.0% |

Maxeon Solar Technologies (MAXN) | Singapore | 0.0% |

Crown Castle Inc. (CCI) | USA | 0.1% |

VICI Properties (VICI) | USA | 0.2% |

* Ardagh Metal Packaging is a Luxembourg-based company. However, it appears that the fund is holding shares of a domestic subsidiary.

We can see that 60.68% could be a reasonable estimate for the percentage of American stocks (as a proportion of the total common stock allocation) held by the fund. However, it would be rather strange for the fund to break things down in this way, given that the common stock allocation itself is only 0.8% of the fund. The only other feasible explanation though is that BlackRock was careless and made a mistake on its website. I will admit that I am uncertain about what is going on here, but it seems like this is a reasonable guess.

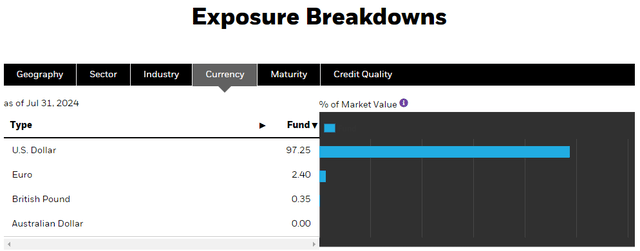

The fund only has 86.26% of its assets invested in securities that were issued by American entities. However, fully 97.25% of the fund's assets are denominated in U.S. dollars:

BlackRock

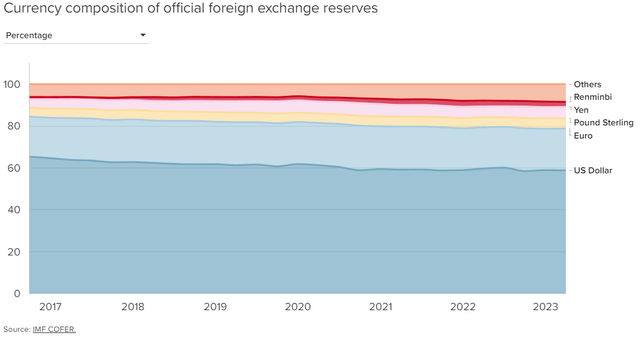

This means that the coupon payments of nearly all of the securities in the portfolio will be paid in U.S. dollars. This might be acceptable for some domestic investors who are worried about currency risks, but I will admit that I would rather have exposure to other currencies. After all, nearly everyone who reads the financial media regularly is well aware that the U.S. dollar is struggling to retain its reserve currency status. As of right now, the U.S. dollar accounts for 58.88% of official reported currency reserves. This is close to the lowest representation that the U.S. dollar has had going back to 2016:

Atlantic Council/Data from International Monetary Fund

The representation of the Japanese yen and the Chinese renminbi in foreign currency reserves have increased over the same period, as has the proportion of currencies not specifically considered to be typically held by central banks. The representation of the British pound and the euro have remained relatively stable. Thus, it is only the U.S. dollar that is seeking declining interest. This situation, unfortunately, means that the foreign demand for the U.S. dollar is not what it once was and that applies downward pressure on the value of the U.S. dollar relative to foreign currency. As the Federal Reserve begins to cut interest rates, that will almost certainly apply further downward pressure on the currency's valuation, since there will no longer be as much interest in purchasing it in foreign exchange carry trades. When we combine this with the near certainty of high Federal government fiscal deficits going forward, it is easy to see why I am growing bearish on the U.S. dollar. As such, I will admit that I would prefer to see this fund receiving coupon payments in a larger variety of currencies in order to potentially profit from a foreign currency rising against the U.S. dollar. It does not appear that this fund is doing so.

Potential investors should therefore consider this to be a play on domestic interest rates and the U.S. dollar. As entities in the United States represent the overwhelming majority of the fund's assets, the BlackRock Corporate High Yield Fund can be expected to perform much like a domestic bond fund. As in, the policies of the Federal Reserve are the most important determinants of the fund's performance, although it will be vulnerable to shocks if an enormous number of companies default all at once. Despite the website's claims about foreign investment, this fund is not really a good way to invest in foreign-issued bonds.

Leverage

As is the case with most closed-end funds, the BlackRock Corporate High Yield Fund employs leverage as a method of boosting the effective yield and total return that it earns from the assets in its portfolio. I explained how this works in my previous article on the fund:

In short, the fund borrows money and then uses that borrowed money to purchase high yield bonds and similar income-producing assets. As long as the purchased bonds have a higher yield than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. This fund is capable of borrowing at institutional rates, which are considerably lower than retail rates. As such, this will usually be the case. However, it is worth noting that the rising interest rate environment has made this strategy less effective than it was a few years ago, when leverage was basically free.

The real downside to leverage comes from the fact that it boosts both gains and losses. As such, we want to ensure that the fund does not have too much leverage, because that would expose us to too much risk. I do not typically like to see a fund's leverage exceed a third as a percentage of its assets for this reason.

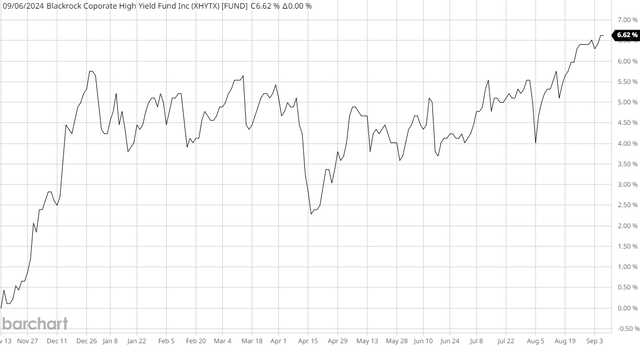

As of the time of writing, the BlackRock Corporate High Yield Fund has leveraged assets comprising 25.56% of its overall portfolio. This represents a marked improvement over the 29.56% leverage that the fund had the last time that we discussed it. After all, the fund's share price has risen fairly significantly since the publication date of my previous article on this fund. That suggests that the fund's net asset value has also increased over the period.

This chart shows the fund's net asset value from November 13, 2023 (the date that my previous article on this fund was published) through today:

Barchart

As we can see, the fund's net asset value is up 6.62% since the publication date of my previous article. This is much less than the fund's share price appreciation over the same period, which suggests that the fund is no longer offering as attractive a valuation as it was the last time that we discussed it. This will be discussed later in this article. For now, we see immediately that the fund's net asset value has risen over the period. All else being equal, that should cause the fund's leverage to decline due simply to the fact that the outstanding borrowings now represent a smaller proportion of a larger portfolio.

The BlackRock Corporate High Yield Fund currently has a leverage ratio that is substantially below the one-third maximum that we usually consider to be acceptable for a closed-end fund. However, let us compare this fund to its peers to determine if its current leverage ratio is reasonable for the fund's strategy:

Fund Name | Leverage Ratio |

BlackRock Corporate High Yield Fund | 25.56% |

Allspring Income Opportunities Fund | 30.80% |

BNY Mellon High Yield Strategies Fund | 28.66% |

Credit Suisse High Yield Bond Fund | 26.33% |

Invesco High Income Trust II | 27.81% |

Neuberger Berman High Yield Strategies Fund | 27.50% |

(all figures from CEF Data)

As we can see, the BlackRock Corporate High Yield Fund boasts the lowest level of leverage out of all of its peers. This strongly suggests that the fund is not employing too much leverage for a junk bond fund. Thus, investors probably do not need to lose too much sleep over the fund's use of borrowing.

Distribution Analysis

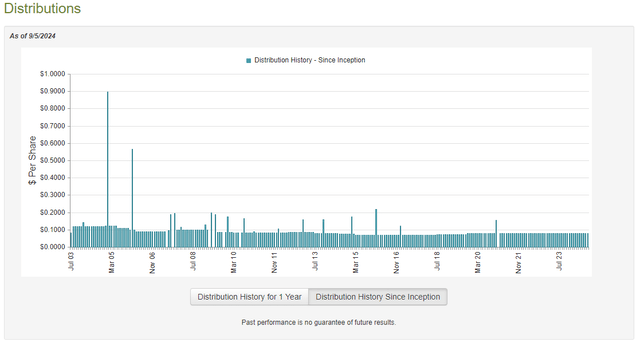

The primary objective of the BlackRock Corporate High Yield Fund is to provide its investors with a very high level of current income. To this end, the fund pays a regular monthly distribution of $0.0779 per share ($0.9348 per share annually). This gives the fund a 9.44% yield at the current share price, which, as we already saw, is reasonable compared to its peers.

The fund has been very consistent with respect to its distribution since October 2019, but prior to that, it tended to fluctuate somewhat:

CEF Connect

As I described in my previous article on this fund:

The fact that the distribution has exhibited a great deal of volatility may be something of a turn-off for those investors who are seeking to earn a safe and consistent level of income from the assets in their portfolios. However, this fund has been much more consistent than most other bond funds over the past three years. As we have seen in various previous articles, most closed-end funds that invest in traditional bonds have cut their distributions over the past two years as falling bond prices and rising yields have caused many of them to suffer losses across their portfolios. This fund has maintained its distribution over the same period, which is curious. We should have a closer look at the fund's finances and attempt to determine why it has been able to perform a task that few of its peers have been able to accomplish.

As of the time of writing, the most recent financial report for the BlackRock Corporate High Yield Fund is the semi-annual report for the six-month period that ended on June 30, 2024. A link to this report was provided earlier in this article. This is obviously a much newer report than the one that we had available to us the last time that we discussed this fund, so it should work pretty well to provide an update.

For the six-month period that ended on June 30, 2024, the BlackRock Corporate High Yield Fund received $1,167,172 in dividends and $72,755,848 in interest from the assets in its portfolio. When we combine this with a small amount of income from other sources, we see that the fund had a total investment income of $75,252,940 over the six-month period. The fund paid its expenses out of this amount, which left it with $53,783,405 available for shareholders. This was not sufficient to cover the $66,867,491 that the fund paid out in distributions over the period.

Unfortunately, the fund was not able to make up the difference via capital gains. For the six-month period that ended on June 30, 2024, the BlackRock Corporate High Yield Fund reported net realized gains of $8,253,196, but this was offset by $14,351,868 net unrealized losses.

The fund's net assets did increase over the period, but it was only because of a capital raise that brought in $15,216,067 to the fund. The fund also issued new shares to those investors who reinvested their distributions, which brought the total amount of money coming in to $19,927,716. Due to the money coming into the fund from these two sources, the fund's net asset value increased by $744,958 over the period. However, this was entirely due to new money, not investment performance.

The fund had to issue new shares to those investors who put in the $19,927,716 of new money. Thus, the total amount of money that it has to pay out in distributions has increased. This has not helped the fund cover its distributions in any way. The only way that a fund can get money to distribute on a sustainable basis is if its net investment income plus net realized gains increases by the same amount or more than it is distributing. This fund failed to do that during the six-month period ending June 30, 2024.

With that said, there were sufficient excess returns during the full-year 2023 period to allow the fund to fully cover all of the distributions that were paid out during the past eighteen months. Thus, while the fund failed to cover its distributions during the most recent six-month period, it does appear that it is okay overall. Investors are still advised to keep an eye on the fund's net asset value, though, as there is no guarantee that this will continue to be the case.

Valuation

Shares of the BlackRock Corporate High Yield Fund are currently trading at a 0.80% premium to net asset value. This is a better price than the 1.33% premium that the shares have had on average over the past month. However, there is no real reason why this fund deserves to have a premium valuation. The last time that we discussed this fund, it traded at a discount and some of the fund's peers have similar performance and also trade at a discount right now. Thus, it may be advisable to wait for a better price.

Conclusion

In conclusion, the BlackRock Corporate High Yield Fund is a reasonably good bond fund that investors can use to obtain a high level of income from their portfolios. The fact that this fund pays a distribution to its investors instead of forcing them to sell shares for income makes it more attractive during periods of market volatility like today's environment. Unfortunately, bonds in general offer limited upside right now because all of the interest rate cuts that are likely to occur are already priced in. Bonds also have a limited ability to protect against inflation. Thus, the yield is probably all that today's investors can really expect from this fund.

I cannot see any reason to recommend this fund while it trades at a premium. It might be a decent income play if it ever becomes available at a discount, however.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

Most Discussed

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10