EZA: Overreaction To GNU Government And Lower Inflation

- The iShares MSCI South Africa ETF has surged over 15% in six months due to a favorable election result and a potential regional interest rate pivot.

- Despite improved investor sentiment, I'm cautiously optimistic about South Africa's new government. Moreover, cyclical economic challenges have emerged.

- EZA ETF's portfolio appears concentrated, raising concerns about its cyclical performance and exposure to geopolitical risks.

- Although a peer-based analysis conveys that the EZA ETF has a compelling dividend, I outline the ETF's cyclicality risk and valuation concerns.

Anup Shah/DigitalVision via Getty Images

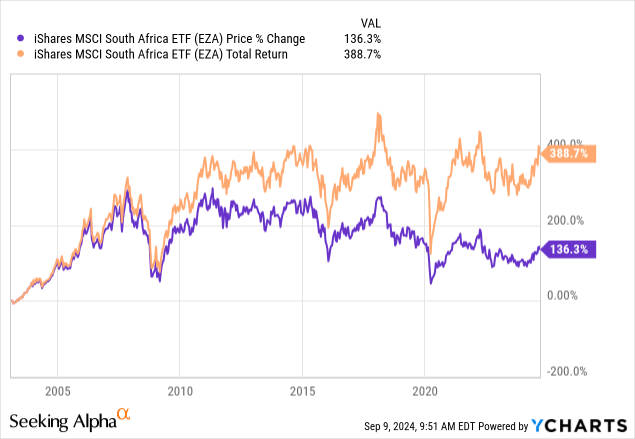

As its name implies, the iShares MSCI South Africa ETF (NYSEARCA:EZA) is a tracking vehicle replicating the South African stock market. The ETF has surged by over 15% in the past six months, mainly due to a favorable South African election result and a pending regional interest rate pivot.

EZA ETF Six Month Performance (Seeking Alpha)

This article assesses EZA ETF's latest surge in the context of South Africa's election result, other economic considerations, financial-market-based variables, and the ETF's portfolio composition.

Without further delay, let's traverse into the analysis.

What Is The EZA ETF?

The iShares MSCI South Africa ETF tracks the MSCI South Africa 25/50 index, which captures about 85% of South Africa's float-adjusted market capitalization. Furthermore, the EZA ETF's FX risk is hedged, presenting investors with U.S. dollar-based returns, meaning its total risk profile is likely less than South Africa's Johannesburg Stock Exchange.

iShares

The iShares MSCI South Africa ETF's recent returns have impressed as regime changes have emerged. However, as visible in the following diagrams, the ETF displays cyclical results, likely due to sector concentration and geopolitical risk.

Let's examine EZA ETF's latest events to make sense of its recent performance and formulate an outlook.

South Africa's GNU Government: Sentiment Vs. Reality

South Africa hosted its national election in May, in which the African National Congress lost its majority rule for the first time in thirty years.

The African National Congress received a bad rap for mismanagement and corruption charges. Therefore, it was acknowledged by market participants when South Africa's major political players agreed to a Government of National Unity. Moreover, fears of an anti-democratic government through the MK Part and the EFF were avoided, adding additional optimism to South Africa's outlook.

Election Results (IEC)

Cautious Optimism

Investor sentiment has improved. However, I'm cautiously optimistic about the country's new government; here's why.

Firstly, South Africa has dispensed numerous positive messages in the past thirty years, including optimism about Nelson Mandela's ANC government in 1994 and a post state capture government led by Cyril Ramaphosa since 2018. However, the reality is that South Africa has a disappointing employment rate, sluggish GDP growth, dysfunctional state-owned enterprises, and exceptionally high levels of corruption. In fact, South Africa is on the Financial Action Task Force's greylist regarding serious charges, which you can read about via this link.

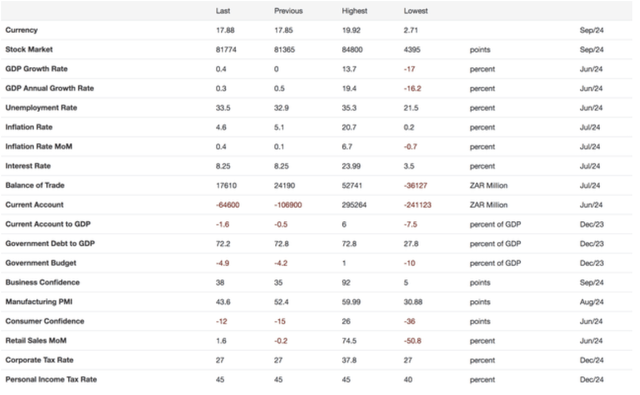

Economic Indicators (Trading Economics)

In summary, my first point in this subsection alludes to the fact that political deception has prevailed while fundamental socio-economic factors have been neglected. Therefore, like many, I want to see tangible results before buying into the hype.

Challenges Faced By Government

Looking past the optics of the GNU, South Africa's government faces serious challenges. For those unaware, South Africa has various state-owned enterprises, such as Transnet, Eskom, and South African Airways.

The aforementioned enterprises contribute to the nation's fiscus and are key in securing external debt. Unfortunately, the nation's SOEs are in tatters, and the private sector has been called upon to help mitigate the situation. I'm unsure whether South Africa's government and private sector will merge, as their relationship has broken down in recent years. Moreover, South Africa has a narrow tax base and a vulnerable corporate ecosystem. As such, the region's capacity to produce the necessary capital expenditures can be questioned.

I'm not saying that the GNU won't work, or that critical infrastructure cannot be restored. I'm merely saying that I think the Johannesburg Stock Exchange and EZA ETF's post-election performance might be premature, especially considering the tangible risk factors I have outlined.

EZA's Portfolio Composition Seems Concentrated

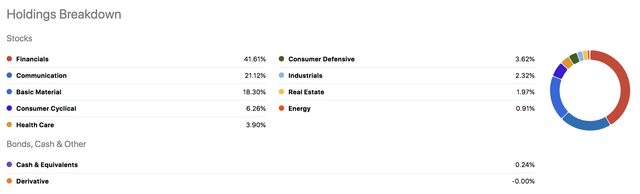

I deem EZA ETF quite concentrated. Although not necessarily disadvantageous, concentration risk can cause problems for long-term investors as it might introduce cyclicality.

A sectoral vantage point shows that approximately 41.61% of the EZA ETF's portfolio belongs to financial services. Moreover, the communications and basic materials sectors fulfill 21.12% and 18.3%, respectively, much more than their closest counterpart, the consumer goods (cyclical) sector, which spans merely 6.26% of EZA ETF's portfolio.

EZA ETF Portfolio - Sectoral (Seeking Alpha)

The ETF's sectoral exposure suggests it can be sensitive to primary economic and capital market indicators. Furthermore, EZA's constituency indicates security concentration risk, with its top ten holdings consuming approximately 63.18% of its portfolio.

Some of EZA ETF's primary holdings include Naspers (OTCPK:NPSNY), FirstRand Ltd (OTCPK:FANDY), Standard Bank (OTCPK:SBGOF), Capitec (OTCPK:CKHGY), and Gold Fields (GFI). I'm not saying I dislike these stocks. I'm simply outlining the concentration risk and lack of diversification.

EZA Portfolio - Constituents (Seeking Alpha)

Concentration Risk and Market Factors

Let's expand on the ETF's concentration risk and why it might play a critical role in late 2024.

South Africa's inflation rate has dipped below 5% for only the second time since late 2021. Most believe an interest rate cut will occur, which, I think, will detract from the banking industry through lower gross and possibly net interest income. Moreover, South African credit spreads are exceptionally tight, which might change when interest rates settle lower as slower economic growth paired with the (generally accepted) inverse relationship between the yield and credit curve cycles take shape.

CDS - Click on Image To Enlarge (Investing.com)

I'm essentially stating that I expect a higher credit risk environment in late 2024 and early 2025, which might lead to higher provisions and lower NII for banks. To substantiate my economic outlook, I re-embedded a table of South Africa's salient economic variables below.

Economic Variables (Trading Economics)

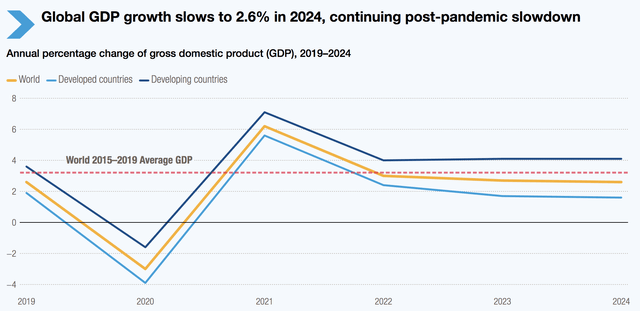

Another matter to consider is the outlook on global economic growth. I think slower global economic growth might stun basic material producers. Although I think the likes of Impala Platinum (OTCQX:IMPUY) and Sibanye Stillwater (SBSW) might provide tactical opportunities, I believe most commodity producers face significant headwinds. Therefore, I'm concerned about EZA ETF's exposure to basic materials.

Global Growth To Slow Just Above Recession Threshold (UN Trade & Development)

EZA ETF's Return Profile

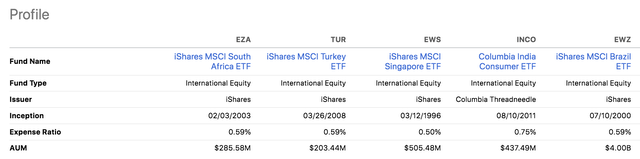

I compared EZA ETF's optics to TUR ETF (TUR), EWS ETF (EWS), INCO ETF (INCO), and EWZ ETF (EWZ) to gain a better understanding of its return profile.

Peers (Seeking Alpha)

The ETF's expense ratio is in line with those of its peers, suggesting no real benefit or disadvantage. Assuming the ETF's expense ratio stays constant, investors will see a ten-year holding period cost of around 6.06%.

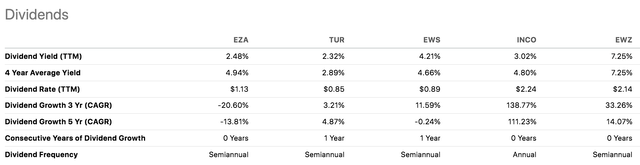

Furthermore, EZA ETF has a four-year average dividend yield of 4.94%, which is high if a peer-based analysis is considered. However, I flag the ETF's negative dividend growth rate and cyclical features.

Peers (Seeking Alpha)

A glance at the ETF's price-to-net asset value shows that it probably doesn't present an arbitrage opportunity. In fact, I think the ETF's P/NAV should be lower than one due to its cross-border settlement, the use of American Depositary Receipts, and the inclusion of illiquid securities.

| Metric | Value |

| NAV/PS Sept. 9 | $45.41 |

| Closing Price Sept. 9 | $45.62 |

| P/NAV | 1.004x |

Source: iShares and Seeking Alpha

Final Word

The iShares MSCI South Africa ETF has surged amid optimism about South Africa's GNU government and anticipation of an interest rate cut. However, I believe investors have overcommitted, as tangible proof of a better political environment remains to be seen. Moreover, lower interest rates can detract from EZA ETF's bank stock-centric portfolio through lower interest income and higher provisions.

While a peer-based analysis suggests that EZA ETF presents a decent dividend, I identify cyclicality and valuation metrics as salient risk factors.

I'm unconvinced by South African stocks for the time being.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

Most Discussed

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10