Destiny Tech100 And The Dark Side Of Investment Democratization

sturti/E+ via Getty Images

We love investment democratization!

By “we,” I mean at least all segments of the Seeking Alpha community.

Its why members read articles, like some and hate others, comment candidly on them, and use the site’s other offerings. It’s why folks like me write independently here. Commitment to this mission is what brings editors, managers, etc. to Seeking Alpha.

I don’t know the Seeking Alpha demographic profile. But I suspect many in the community weren’t active investors back in the pre-democratization era. If that’s you, don’t fret. You didn’t miss much.

I’ve seen countless sell-side research reports. Those are what the elite (the big institutions) got but from which ordinary folks were excluded.

Trust me here… the typical Seeking Alpha article today is at least as insightful, and often more so, than sell-side research. (Actually, if you look at author Bios, you’ll see many have professional research backgrounds.)

We’re the good side of investment democratization.

But there’s a dark side too. Sometimes, we give the average investor more power than they can responsibly handle. And this can hurt them.

Consider, for example, the turn-of-the-century bursting of the dot-com bubble.

Too many investment recommendations were disseminated through freely accessible media. Audiences didn’t understand that “talking heads” represented just one opinion.

Nor did they understand that those opinions may not have been objective. Nor did they appreciate the need to independently vet those opinions against data and other speakers.

Democratization sounds good. But sometimes, people use their freedoms to hurt themselves.

An emerging democratization trends in venture capital opens the door to treacherous investments.

Destiny Tech100 (NYSE:DXYZ) is a “closed end” mutual fund that let's anybody who can click a mouse or tap a touch screen instantly become a venture capitalist.

DXYZ experienced a rapid meme-stock-like boom-bust quickly after it started trading on March 25, 2024.

The stock opened at $8.25. It hit an intra-day high of $32 before closing at $9. It then rallied to a $105 intra-day high on April 8th. It now trades near $11.

But even at today’s price, it remains a dangerous choice.

For starters…

DXYZ Looks Like an ETF, But in Truth, It’s Scarily Different

It’s a “closed-end” fund (CEF).

At one time, these were pretty popular. They let investors instantly buy into a basket/portfolio of stocks without the rigmarole of traditional “open-end” mutual funds.

With open-end funds, you would, quite literally, own a percent stake (albeit a nano sized stake) in the actual portfolio (minus an allocation for expanses).

But you could only buy in or sell out once per day. And fund sponsors found all sorts of ways to make you pay for the fund’s marketing costs.

CEFs did away with investors’ direct ownership of the assets. A CEF is business entity. Walmart (WMT) is a business entity that does retailing. CEFs are in the business of having an investment portfolio.

Just like buying WMT shares doesn’t give you direct ownership of any stores or inventory, buying CEF shares doesn’t give you direct ownership of anything in the portfolio. In both cases, you’re a part of the entity that owns the assets.

You buy and sell a CEF the same way you would WMT. You trade in the public markets through your broker.

As with WMT, a CEF company has an income statement, etc. But CEF revenues and (fee income) minus expenses (costs of running the fund) aren’t interesting to investors.

Instead, they focus on the CEF’s balance sheet. It’s about the Net Asset Value (NAV) of the portfolio.

Sounds like an open end mutual fund but with easier trading… right?

Not so fast.

CEFs would be ideal if we could be sure the market price of the stock would reflect the market value of the assets (NPV).

In the old days, we might have wanted the same for WMT. We would have hoped that the stock’s price would, more or less, equal book value per share. But we don’t think as much about that as we used to.

Contemporary investment culture focuses on WMT’s earnings. If we do that rationally, we figure the stock price and book value will relate in a sensible way. We also hope the price reflects the impact of intangible assets that defy conventional accounting methods and expectations for growth.

CEF shares do that too, but in a much vaguer way. We don’t really have analytic techniques for assessing the portfolio’s growth potential (to the degree we have for WMT’s retail operations). And CEFs don’t really deal with intangible assets per se.

So prices for CEF shares can and often do go meaningfully out of whack in terms of their relationships with NAVs.

So the first question a knowledgeable investor asks about a CEF is: “What’s the discount or premium?” In other words, we look for the gap between NAV and the stock price.

This is an entire investment theme unto itself. Investors love to buy CEFs that trade at large discounts to NAV. They assume they can profit as the discount vanishes, or as happens more often, narrows a bit.

Best of all is a very big discount that never narrows. That can prompt a proxy fight (or the threat of one) that forces CEF management to go through the legal steps to covert the CEF into an “open end” mutual fund.

That would immediately cause each shareholder’s interest to become exactly equal to NAV. The easy CEF trading would vanish. But you’d wind up with a nice profit. You’d profit by redeeming (selling) your no-longer-discounted stake for NAV.

But not all gaps between CEF NAV and CEF share prices involve discounts. Some CEFs sell at premiums to NAV. That means you might pay $110 for every $100 of NAV.

That’s usually bad.

It’s not impossible to justify. Back in the 1980s-90s. I covered some emerging market CEFs. It was extremely hard for the average U.S. investor to gain access to those stock markets. So many were intrigued by the growth opportunities and considered it reasonable to pay a premium just to get a stake.

Eventually, ETFs came into being. These are a lot like CEFs but with one massive difference.

An ETF has a complex exchange mechanism involving “authorized participants” (APs). They can

provide baskets of stocks that line up with the ETF’s portfolio. In exchange, they receive “creation units.” APs also can offer cash and receive stock baskets.

Don’t sweat the details. Just know that arbitrage trading by APs almost instantly causes premiums or discounts to largely vanish.

The problem for DXYZ is that it isn’t an ETF. It’s an old-fashioned CEF.

That means the shares that trade in the market can be priced at discounts or premiums to NAV.

Don’t bother wondering about getting a discount…

DXYZ Trades as an Extreme Premium to NAV

On August 30, 2024, DXYZ reported that it’s 6/30/24 NAV was $5.15 per share.

If DXYZ’s current share price is $11, that puts its premium at above 100%.

I went to the CEF Connect screener and retrieved all equity CEFs. (That tool is free, and powered by Morningstar.)

As of this writing, there are 411 equity CEFs. I sorted from highest premium to widest discount.

The top premium, 454.79%, is for the abrdn Asia-Pacific Income Fund (FAX). I know nothing about FAX or why the premium is so high. But it’s covered on Seeking Alpha. So if you’re interested, you can click here.

DXYZ carries the second highest premium. As of the pricing date used by the screener, it came in at 109.71%.

Three other CEFs have premiums above 50%. Another 16 have premiums between 10% and 50%. Finally, 54 CEFs had premiums between zero and 10%.

That means 336 Equity CEFs out of 411 (81.8% of the total) trade at discounts, rather than premiums.

So clearly, DXYZ is not by any means run of the mill. In fact, given the context of Equity CEFs, I feel comfortable characterizing the DXYZ premium as Extreme.

I Can’t Justify DXYZ’s Premium Stock Price

The only justification I could envision for such a large premium would be if DXYZ gave us access to growth we could not otherwise obtain.

That immediately raises the issue of “venture capital.”

Can DXYZ’s portfolio generate enough growth to justify paying about $11 a share for a portfolio worth little more than $5.00 per share. In other words, can DXYZ grow into its premium?

The romantic image of venture capital suggests a definitive “yes.” Who doesn’t dream of getting in on the ground floor of the next Microsoft (MSFT), Nvidia (NVDA), etc.

Imagine how wonderful it would be to get a stake before an IPO so we could later sneer at suckers who pay more than 50 times earnings in the public markets!

The realty, however, is often not so glamorous.

First off, don’t assume pre-IPO investors get all that return. Many use IPOs as to exit their venture investments. They sell the shares being purchased by the public.

Imagine you were a venture capitalist who cashed out when NVDA went public on January 22, 1999. Your takeout price (adjusted for splits) would have been $0.04375 per share. The other $100-plus per share was realized by public shareholders, not you.

So venture capital is not a simple short cut to the main job of a growth investor… to correctly identify companies with bright long-term prospects and make reasonable judgments about public market valuations.

To get longer term gains, one would have to keep the venture investment going longer, or get involved in venture secondaries, a secondary market for venture capital interests.

And there are just so many future NVDAs out there.

The typical venture capital portfolio is widely diversified, often with 30-80 holdings. But many, perhaps 9 out of 10 investments, fail. Only a small percentage of investment hit big.

DXYZ’s portfolio is trending in this typical direction.

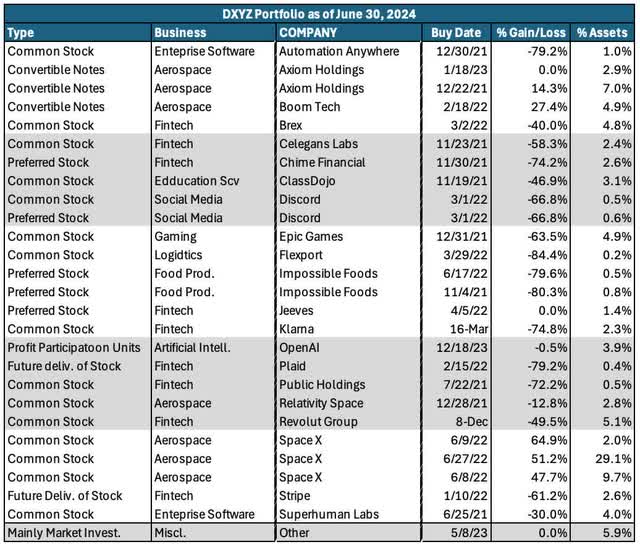

Here are the assets DXYZ held as of the last reporting date, June 30, 2024.

Author compilation based on data from DXYZ 6-30-34 Semi-Annual Report

Notice how many positions are very deep in the red.

Space Exploration (Space X) is the big winner. But despite outsized gains here, the portfolio’s overall weighted average gain so far is just 2.57%.

The Cambridge Associates U.S. Venture Capital Index suggests an average annual return of 18.96% over the 25-year period that ended March 31, 2024.

That, however, measures venture capital investments… not returns earned by investors who pay more than $200 for every $100 of venture capital actually invested.

Don’t get swayed either by better returns you may have seen attributed to “private equity.” By strict dictionary definition, we can say venture capital is a form of private equity. But as a practical matter, private equity invests in mature companies. Venture capital aims at early stage situations.

Cambridge has a private equity index too. It averaged a 13.03% annual return over the 25 years that ended March 31, 2024. And again, these presume investors pay $100 for every $100 invested, not $200-plus.

So I see nothing about the DXYZ portfolio that leads me to believe in paying the absurd premium its share price commands.

There’s a Better Way If You Can Handle the Risks

It’s easy to get a stake in private equity. You can, for example, consider shares of KKR & Co. (KKR) or others in the Asset Management and Custody Banks Industry.

But even if you’re aggressive and really want in on venture capital, you can consider the ARK Venture Fund (ARKVX).

Yes, this is the ARK many readers know well, the one run by Cathie Woods.

It’s not an ETF. It’s not even a CEF. It is quite literally, a venture capital fund.

You can’t get it easily. Schwab doesn’t trade in it.

The “How To Buy” link on ARK’s web site provided two buying choices a week or so again.

One was to Titan, an advisory firm. But that arrangement no longer seems to be operational. I don’t know why Titan is suddenly no longer able to put anyone in ARKVX.

The other involves SoFi, a fintech company covered by Seeking Alpha; SoFi Technologies (SOFI).

That firm rightly considers XRKVX an ”alternative investment.” You need a user ID and password to get to its ARKVX page.

If you go for it, make absolutely positively sure you read the disclosure (see pale yellow box on the right side of the page) about ARKVX being an “interval fund.” The quick and dirty – you can get into an interval fund easily enough easily, but it’s harder to get out.

And don’t even think of investing without opening the Summary Prospectus and studying at least page 41. That gives more detail on ARKVX’s interval fund status.

The Right Side of Investment Democratization

It’s a pain in the neck to deal with ARKVX.

Good!

That’s how it should be. Venture capital is breathtakingly risky. ARK can’t know for sure that you understand the risks. But limitations on the way you can get into the fund at least increases the probability that you’ve thought about it carefully. Hopefully, your thought process included the risks.

DXYZ is on the wrong (dark) side of democratization. It’s too easy and convenient to get it in.

That opens it up to folks who don’t truly understand the risks involved and don’t properly understand how dangerous it is to pile a 100%-plus premium to NAV on top of all the other risks inherent in venture capital.

What to Do About DXYZ Stock

YOU INDIVIDUALLY might understand the risks and decide for yourself you want to own DXYZ. That’s fine. All investors are entitled to do their own risk assessment and act accordingly.

But I don’t know you as an individual. Individualized investment is the essence of the regulated investment advisory (RIA) field. I’m not an RIA anymore. And Seeking Alpha isn’t an RIA. Articles here are OK because we communicate one-to-many, not one-to-one.

In my articles I usually relate my recommendation per the Seeking Alpha scale to my confidence in the market and whether I think a stock will outperform, match or underperform the market. I won’t go through that for DXYZ.

Given the absence of a one-to-one RIA relationship, my one-to-many advice is to keep this issue out of your portfolio. If you don’t own it, good. If you do, then I say “Strong Sell.”

And by the way, even if we did have an RIA relationship, I’d still argue long and hard against owning DXYZ and the absurd premium at which its shares are priced. I’d rather have conversations about ARKVX. I won’t own it, but I’d be willing to discuss whether you can handle the risks. I’d be much more comfortable discussing private-equity plays like KKR.

Finally, check back if, in the future, DXYZ’s currently indefensible premium evaporates. I may then change my mind and consider saying Buy or Hold.

Editor's Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

Most Discussed

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10