QQQY: Surprisingly Solid Strategy But Overambitious Distributions

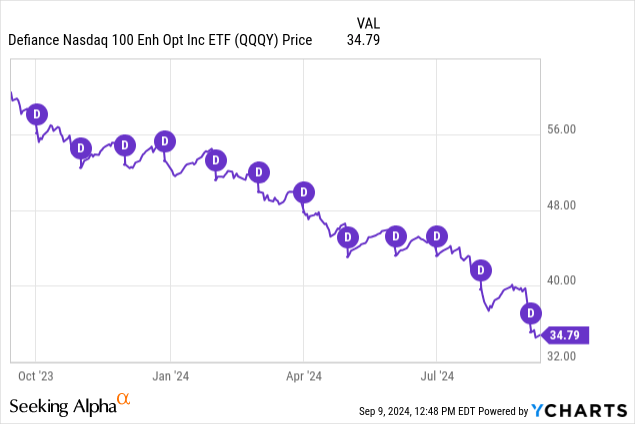

Alistair Berg

Last year, one of the most significant developments in the income ETF space was the launch of the Defiance Nasdaq 100 Enhanced Options Income ETF (NASDAQ:QQQY). This ETF was the first to sell daily NASDAQ 100 put options to generate income and piqued many income investors' interest, by claiming a minimum income target of 0.25% per day. Unfortunately, it's been a year, and many investors may have noticed that QQQY's 90% distribution rate has come at the cost of its NAV. As a result, Defiance announced a 1-for-3 reverse stock split for QQQY and two of its other similar funds. That being said, if you look at total returns, you'll see that QQQY has actually had a positive return. Thus, I decided to look deeper into QQQY and analyze its mechanics. What I found is that QQQY's put option strategy is surprisingly solid and that there is a world where you can do well with this fund. Today, I will share my findings, the strategy you can use with QQQY to maintain NAV, and ultimately, why I don't recommend using that strategy and rate QQQY a Sell.

Surprisingly Solid Strategy

For those unfamiliar with QQQY's strategy, the fund sells daily 0 Days-to-expiry (0DTE) put options on the NASDAQ 100 via Nasdaq-100® PM-Settled Index Options (NDXP). These put options are either at-the-money or 1-5% in-the-money per QQQY's prospectus:

Every day, the Fund will sell put options that are priced either at-the-money or up to five percent in-the-money (i.e., higher than the current market price).

These moneyness adjustments are made based on their target of generating a minimum 0.25% yield daily. If the income is not high enough on any given day, QQQY will sell more aggressive put options to generate larger option premiums, even if it comes at an overall loss.

The Fund seeks to make monthly distributions. To enable it to do so, the Fund seeks to generate a consistent stream of income on a daily basis. In particular, the Fund sells in-the-money put options to seek a minimum daily income of 0.25%. If the Sub-Adviser determines this 0.25% daily income is not achievable, the Fund will sell options that are priced at the current market value to try to make the most of the available daily income. If the potential daily income exceeds 0.25%, then the Sub-Adviser will select a target strike to seek an equal mix of current and potential income.

When I saw this strategy last year, my first thought was that the fund would have more unprofitable days than profitable ones and quickly erode its NAV by taking repeated losses. After backtesting the strategy, however, I was surprised to see the results. QQQY's strategy of selling 0-5% in-the-money 0DTE put options was actually a profitable one over the last year. Using historical NDXP option prices, a hypothetical starting balance of $1.6M on September 8, 2023, would be worth $1.92M today for a total return of 20.2%.

Chart From Author

I started this backtest by collecting historical option prices for NDXP put options at 0%, 1%, 2%, 3%, 4%, and 5% in-the-money, rounded to the nearest $100. At the time, $1.6M was the collateral needed to sell one NDXP put contract, and a 0.25% minimum daily income meant I needed to collect at least $4000 from option premiums daily. Thus, I defaulted to selling at-the-money put options and moved further in-the-money on any given day if I couldn't meet the $4000 minimum. Then, depending on the NASDAQ 100's closing prices, I would cash-settle if needed and add the total profit or loss to the cash balance. Of the 250 tradable days, 171 were profitable, while 79 were unprofitable, for a 68.4% win percentage. It's also good to note that the average profit and loss generated in a day was $9,551 and ($16,414), with the maximum and minimum profit/loss sitting at $60,195 and ($69,231).

Granted, the data is not perfect and should only be used to see the big picture. You should expect QQQY to perform better than these results, even after its 0.99% management fee. The reason is that I had not factored in the interest earned from putting collateral in treasury notes and bonds, and that QQQY can sell options at better prices than the historical data I have. For example, the put option in the following QQQY's Top Holdings Chart was sold at $160.50 per contract while I was limited to $140 using historical option prices.

QQQY Top Holdings as of September 9, 2024 (Image From Defiance)

All things considered, QQQY's 0DTE put options strategy is not the biggest weakness of the fund. Some improvements could be made, but overall, the strategy has come out ahead, at least in the past year. The real problem lies with its overambitious distribution rate.

0.25% Minimum Income Per Day Is Too Much

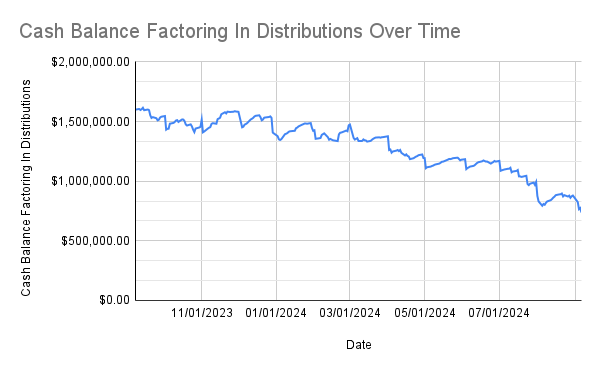

While targeting a 0.25% minimum income daily is somewhat manageable, distributing it is far too ambitious. As soon as I add a factor of withdrawing 7.5% (0.25% times 30 days) from the cash balance in my backtest, you can see how QQQY's distributions are quickly eroding its NAV. An initial balance of $1.6M is only worth $737K by the end of one year compared to the $1.92M if no cash was distributed.

Chart From Author

It's no coincidence that every steep drop in QQQY's price is on its distribution date, and if you look closely, the dips are generally much larger than the fund's gains in any given month.

QQQY would do far better if they didn't constrain themselves to their 90% distribution targets and opted for more conservative income targets. Including out-of-the-money puts (strike prices below the NDX current price) would help them have more profitable days for overall more stable returns, even if the option premiums received aren't as high since they do not capture intrinsic value.

Reinvest What You Don't Need

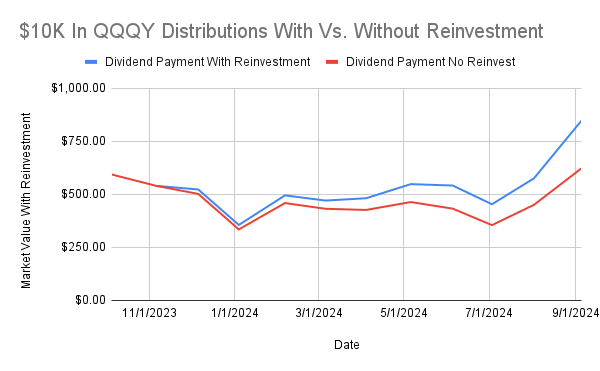

Though QQQY does look like a fund that will continue to decrease in NAV over time, there is an argument that you can reinvest in this fund to retain market value while lowering your cost basis. The idea is that most investors don't necessarily need or should use the entirety of QQQY's 90% distribution. For example, a 90% distribution from $1M in QQQY would equate to approximately $900K. If you're a retiree with $1M and have an income target of $100K per year, there's a surplus of $800K you don't necessarily need and could reinvest. With this idea, I decided to do a hypothetical study on QQQY, where I reinvested a portion of the distributions to attempt to maintain around $10K in market value.

Chart From Author Chart From Author

The results were astonishing. Using this reinvestment strategy would have allowed you to still receive over $2K in distributions for an approximately 23% distribution rate while only losing about 5% in market value. For comparison, JEPQ has gained 6.7% in the last year in market value but only distributed 9.9%. There is a world where you can reinvest even more into QQQY for positive market value while collecting larger premiums. However, there are a couple of problems with this approach.

The Problems

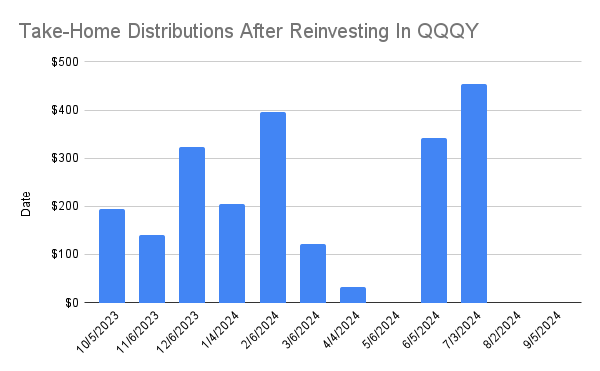

First, distributions become extremely inconsistent when you also attempt to maintain market value. While the total distributions at the end of the year were very high, there were multiple months where you had to reinvest all your distributions to maintain market value.

Chart From Author

For many income investors, stability is a non-negotiable. With this strategy, you're either dealing with volatility in the asset price or distributions, which can make the fund unappealing to many. Also, considering that most people won't use this strategy and another large number of QQQY investors will opt to reinvest distributions in other assets, it turns into a question of how long people are willing to continue propping up a fund whose NAV has and will only continue to decline.

Taxes must also be mentioned here. If any QQQY investment is made outside of a tax-sheltered account, certain portions of QQQY's distributions are subject to ordinary income taxes, which can significantly eat away your profits.

NAV Will Continue To Decline

Although I was pleasantly surprised by QQQY's positive returns, I have to rate this fund a Sell as its NAV will continue to decline without any significant changes to its strategy. Selling puts in the money, and distributing at an approximately 90% rate is far too aggressive and unsustainable, especially if the market begins to slow down as it has. Yes, QQQY will collect larger option premiums during periods of higher volatility, but a declining market would lead to a larger number of put options exercised and increase the losses QQQY takes from cash-settling their positions. For most buy-and-hold investors, QQQY just isn't the right fund unless Defiance decides to reduce its target distribution rate to a more sustainable one.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

Most Discussed

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10