9 Closed-End Fund Buys In The Month Of August 2024

Jerome Maurice

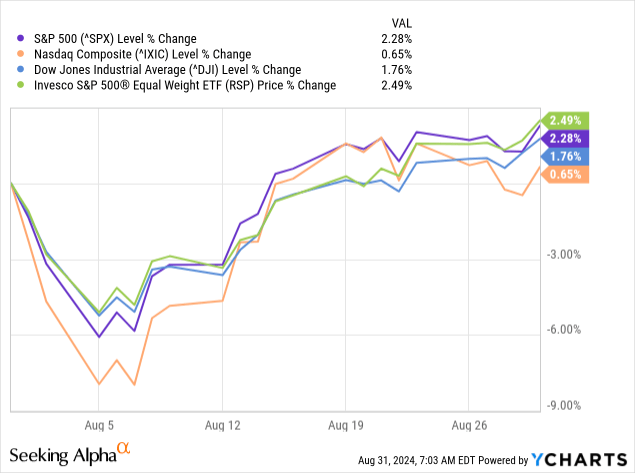

The broader equity market started off in August with a continuation of declines that started in July. The Nasdaq ended up actually hitting correction territory; however, that was only briefly, and the markets finished off the month near all-time highs once again.

The Dow Jones Industrial Average actually was finishing off the month at all-time highs as there has been a rotation into more value-oriented investments. The Invesco S&P 500 Equal Weight ETF (RSP) actually came out on top over the last month.

Ycharts

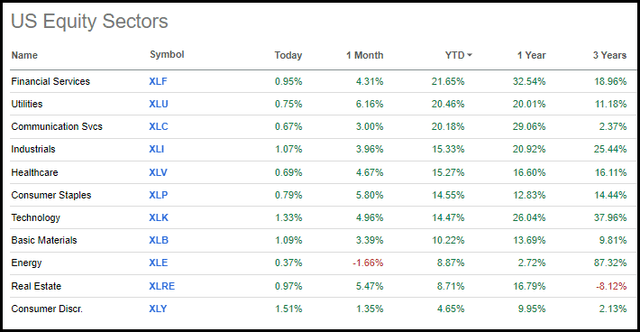

This broadening out of the market appears healthy as interest rate-sensitive sectors start to get some attention. For the last month, utilities, consumer staples and real estate led the way, finishing up 6.16%, 5.80% and 5.47%, respectively. Perhaps more surprisingly, it is the YTD returns that now show financials and utilities are the top-performing sectors.

Real estate is still coming in near the bottom at second to last, but the last month went a long way to push the sector higher. The consumer discretionary sector is the worst performing, but with an increase of 4.65% is good enough to put all sectors positive this year.

U.S. Equity Sector Performance (Seeking Alpha)

Initially, it was looking like we were finally going to get some market volatility to put some more cash to work aggressively. However, being near all-time highs once again on the back of a swift recovery meant that those plans changed. This month ended up being mostly active just because of the corporate actions this month, primarily BlackRock tender offers.

Calamos Strategic Total Return Fund (CSQ)

I picked up CSQ on August 5, the low for the latest market pullback and correction for the Nasdaq. Meaning I was able to get one really good purchase in for this latest market decline, so the short bit of volatility that we got wasn't a complete waste for me.

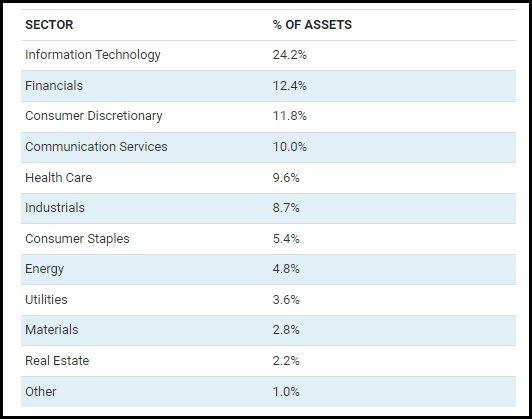

The largest allocation for the fund is to the information technology sector. It is double the size of the next largest sector allocation. Though it isn't overwhelmingly weighted in tech, it still has enough in the mega-cap tech names that they have a sizeable influence on the fund. The use of leverage in the fund will also make it more sensitive to market gyrations.

CSQ Sector Allocation (Calamos)

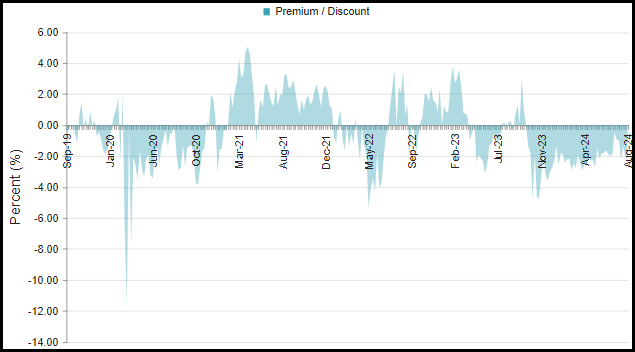

One thing that is difficult with CSQ is the fact that it always trades near parity with its NAV per share. As a CEF investor, I like buying at unusually large discounts that are relatively deeper than the fund has historically traded at. Even despite the rather brief volatility, CSQ's discount did not open up materially in this latest market decline. Still, it was the overall market decline that made me feel it was still worth adding to this position for the long term.

CSQ Discount/Premium History (CEFConnect)

Adams Diversified Equity Fund (ADX)

Shortly after adding CSQ, I rebought my ADX shares. This was a rebuy because ADX had gone through a 10% tender offer at 98% of NAV. This was a TO that worked out fairly well.

As usual, there were many investors who didn't participate. While it is generally expected, you will get more accepted than the minimum, there were far fewer who participated in this ADX offering than I thought. The proration ended up being ~29.62%.

That is nearly 3x of the 10% offer, where 10% is the minimum, as that would happen if only 100% of shareholders tendered 100% of their shares. So, investors who did participate saw more shares accepted than they otherwise would.

The tender offer also finished on August 2, 2024, for determining the share price, which ended up being $22.47. This meant it did occur during the market pullback period, but despite that, I was able to turn around and add back to my position at $20.31. So it could have worked out a bit better had it expired a week or two earlier, but a profit is a profit.

NXG NextGen Infrastructure Income Fund (NXG)

NXG was also the bit of a result of a corporate action because they had finished up their rights offering last month. I had initially purchased a part of my position back after sidestepping the RO, as I discussed last month. With the market downturn, I was able to pick up shares even cheaper—though hesitation of just a few days saw me miss out on an even better deal.

With a high distribution rate of ~16%, this fund is certainly an enticing one. The NAV rate comes in at just over 15%, which is also elevated. So the distribution isn't likely to be sustainable over the long run, but it should get investors to bid up the shares near premium again—then they may or may not choose to do another rights offering.

At a premium, one could consider taking their profit or even selling out at a loss and sidestepping for a potential RO. So, with a higher distribution comes potentially more opportunities to trade around the fund. That's even if I don't believe they'll be able to achieve the actual returns of the high level of the distribution.

BlackRock Tender Offers

After those initial few purchases earlier in the month came the BlackRock tender offers. Earlier in the year, BlackRock announced a discount management program on a number of their closed-end funds. These were moves driven by Saba Capital Management targeting a number of their funds aggressively. BlackRock ultimately 'won the battle,' but it did come at the cost of implementing this sort of move and even raising distributions on their funds to elevated levels.

BlackRock Funds Adopting Discount Management Program (BlackRock)

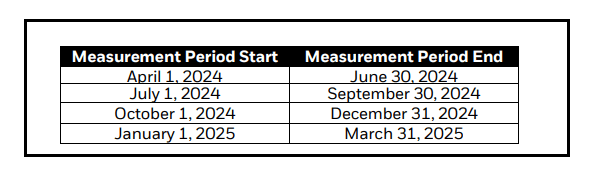

The idea here, though, is that there are four different measurement periods, and if a fund's discount is wider than 7.5%, they will conduct a 2.5% tender offer at 98% of NAV.

Measurement Periods For Tender Offer Triggers (BlackRock)

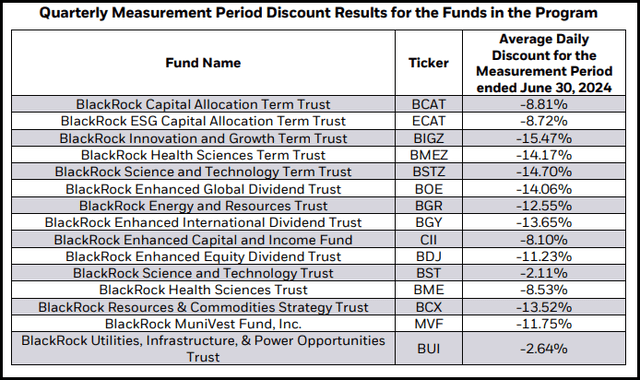

During the first measurement period, all but two of the funds triggered the tender offer. The only two that didn't are two positions I hold, and that was BlackRock Science and Technology Trust (BST) and BlackRock Utilities, Infrastructure, & Power Opportunities Trust (BUI).

BlackRock Quarterly Measurement Discount Average (BlackRock)

In total, I have 8 BlackRock CEFs that qualified for the conditional tender offers, but only participated with 6. The two I didn't participate in were the BlackRock Enhanced Global Dividend Trust (BOE) and the BlackRock Innovation and Growth Term Trust (BIGZ).

My excuse was that these are two of my smallest positions (BIGZ is my smallest position), so I wouldn't stand to benefit as much. That said, I should have and will probably participate in all the funds I can in the future after seeing how many investors didn't participate in these offers. For 2.5% TOs, the prorations on these were big wins!

At least, in my opinion, as I was expecting at least double 5% proration, but they all ended up being so much more. Some investors hesitate to participate in these TOs for tax reasons or simply not knowing about them. Some I also believe that the 2.5% tender offers probably aren't worth their time to track. So, I think those are some of the factors that kept investors from participating. And for those of us who do participate, we thank you for your non-participation, as it ultimately means a better outcome for us.

Here's the recap of the six BlackRock CEF TOs that I participated in:

- BlackRock Enhanced Capital and Income Fund (CII) proration was ~18.88%, and the purchase price was $20.9524. I ended up buying all the shares back that were accepted, plus added to my position at $19.51. I felt like the ~9% discount was incredibly attractive, as the fund doesn't often stay at that wide of a discount for long historically.

- BlackRock Enhanced Equity Dividend Trust (BDJ) saw a proration of ~20.32%, with shares being accepted at $9.1826. BDJ is already one of my largest positions, so I was happy just to add what shares were accepted, and I was able to add those back at $8.62.

- BlackRock Health Sciences Term Trust (BMEZ) had a proration of ~11.09% with a purchase price of $17.6204. I added back only my original shares that were tendered at a price of $15.97.

- BlackRock Health Sciences Trust (BME) saw the best proration I had in this round of offerings, with a total of ~27.27% of shares accepted at a price of $44.4822. BME was already one of my largest positions, but I added even more than what was accepted anyway, thanks to what I view as a very compelling discount that the fund is trading at. I picked the shares up at $41.96.

- BlackRock Science and Technology Term Trust (BSTZ) was the smallest proration I had in this round, likely due to its sizeable discount and its relatively poor performance in the last few years. The proration was ~8.19% at a purchase price of $21.4522; I rebought only the shares that were tendered at $19.32.

- Finally, there was BlackRock ESG Capital Allocation Term Trust (ECAT) with a proration of ~14.57% and a purchase price of $18.0516. I picked the shares that were tendered for $17.44. ECAT's discount has narrowed quite a bit as the fund, along with its similar sister fund, BlackRock Capital Allocation Term Trust (BCAT), adopted a 20% managed distribution policy based on a 12-month rolling average NAV. Those are the types of distributions that aren't sustainable over the long run, but they do narrow discounts.

Overall, I was quite happy with the results and look forward to participating in the next round.

There is an opportunity to get more aggressive here and add to some of the funds that are doing these conditional tender offers with large discounts. However, just because there is a discount and a tender offer doesn't mean it is a guaranteed profit.

One could buy a fund, and if we go into a market correction, these funds could very easily slip below one's buy-in price. There is some margin thanks to a 98% NAV tender offer price, but even with that, it might not be enough with a decent decline in the market.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

Most Discussed

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10