Freight Technologies: A Digital Transformation And AI Focused Business Without Profits

- Freight Technologies focuses on cross-border logistics solutions, offering multiple digital platforms to optimize freight and carrier matching, LTL shipments, fleet management, and real-time tracking.

- Despite significant opportunities in the cross-border market, Freight Technologies faces high competition and relies on volatile spot prices and volume-dependent revenue models.

- The company has a history of operating losses, significant cash burn, and dilution risk, raising doubts about its ability to achieve profitability and sustain operations.

- Given the lack of profitability and high financial risks, I recommend selling the stock until there is clear evidence of improved financial performance and cash flow.

Just_Super/E+ via Getty Images

Currently, many companies are leveraging data to optimize industries and businesses, Freight Technologies is one of those companies. However, as I discuss in this report, the company is also one of the companies that is finding out that despite the opportunities for data leverage to increase industry efficiencies, doing it in a profitable way is more than challenging.

What Does Freight Technologies Do?

Freight Technologies, stylized as FR8technologies or Fr8Tech, is a company that focuses on increasing efficiencies in cross-border logistics. The company has a portfolio of digital solutions. Through the Fr8App, the company offers a platform to match freight and carriers to optimize availability and increase transportation efficiency. The company also has the Fr8Now platform focused on LTL or less-than-truckload shipments whereas the Fr8Fleet platform which is a dedicated fleet management solution and the Fr8radar app allows real-time tracking solutions. Through the Waavely platform, the company also provides digital ocean solutions.

What Are The Opportunities And Risks For Freight Technologies?

Fr8Tech

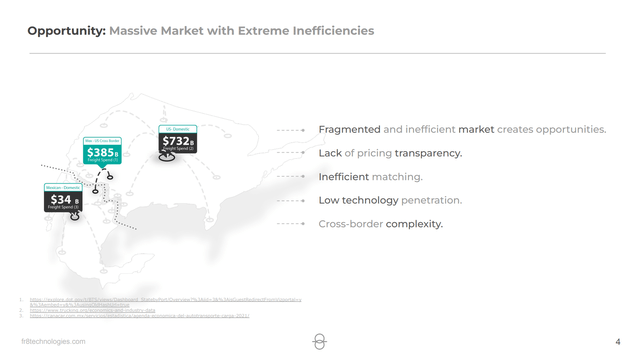

For Freight Technologies there definitely are opportunities, unlike other companies, Freight Technologies focuses on addressing cross-border complexities and efficiencies between the US and Mexico and the US and Canada. In that sense, the company, also unique to other digital freight solution providers such as Uber Freight, Convoy, and Transfix, focuses mostly on the US domestic market. The US domestic market has a freight spend of $732 billion with cross-border US-Mexico having a freight spend of $385 billion and domestic Mexico freight spend is $34 billion. So, there is a huge opportunity if we look at the dollar value of the freight spend and currently technology has a fairly low technology penetration in the industry and the company can leverage artificial intelligence to further enhance its products. I believe that with the cross-border focus, the company has a big opportunity to see demand rise on the nearshoring trend which sees more and more companies opening up facilities in Mexico.

However, what we do see is that rather than running a business with profitable subscription models, digital freight solution providers mostly run a business that depends on spot prices and volume. That makes sense since making the pricing volume dependent allows digital freight solution providers to benefit from volume growth whereas some sort of fixed sum subscription model would not unless subscriptions would be tiered. The drawback of that is that if volumes or prices drop, so do the revenues of the digital platforms. So betting on digital solution providers is not really a way that insulates investors from price and volume dynamics.

Other risks to the business are that many companies are working on technology injection in the freight industry and as a result, it is a highly competitive industry. Not only are dedicated digital freight solution providers among the competitors of Freight Technologies, traditional brokers, 3PL (third-party logistics) companies and internal technology developments at trucking companies also could reduce the demand for the solutions of Freight Technologies.

Probably the biggest risk for investors is the fact that Freight Technologies has never generated a profit:

Fr8Tech has a history of significant operating losses, and Fr8Tech has not been profitable since its inception in 2015. Fr8Tech plans to continue to invest in improving Fr8Tech's platform and services. Recurring losses from Fr8Tech's operations could raise substantial doubt regarding its ability to continue as a going concern. If Fr8Tech fails to transition from a company with a development focus and early growth strategies to fully commercializing its product offerings, it may not be able to fund its operations without raising additional capital, if at all. While Fr8Tech has been successful in raising capital in the past, there is no assurance that it can access additional capital in the future when needed, on favorable terms, or at all. If Fr8Tech fails to execute its business plan and strategies, it may incur losses for the foreseeable future, and be unable to fund its operations at some time in the future.

The company recently completed a 1:25 reverse stock split to comply with the listing standards.

A Look At The Freight Technologies Earnings

There are opportunities for Freight Technologies, but also big risks, and the fact that the company does not provide detailed quarterly earnings does not help either. We do know that the company reported a 30% growth to $4.3 million year-on-year in Q1 2024 with 278% volume growth. Given that Q1 seasonally is the weakest quarter it shows that there could be more growth ahead in the balance of the year. At the same time, we note that revenue growth was nowhere near volume growth which can be driven by spot prices but also could indicate that the pricing model leaves the company more exposed to volume decreases than to increases.

Fr8Tech

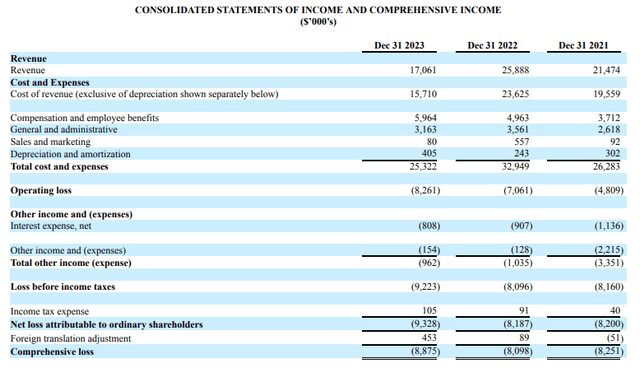

To get a better view of earnings, the most recent results are the annual results. Those results show that revenues declined as the company focused on profitable volumes rather than having a focus on overall volumes, and there was spot price pressure. The cost of revenues decreased in line with the revenue decrease. Compensation and employee benefits increased by 20.2% due to increased stock compensation costs and new hiring while general and administrative costs decreased due to lower legal fees. Sales and marketing costs have decreased as the company is no longer working with the company that provides the marketing. Depreciation and amortization increased due to the completion of the Fr8Tech platform resulting in increased amortization of software.

This has led to an operating loss of $8.26 million, which is worse than the $7.1 million loss in the year prior. The company had cash and cash equivalents of $1.6 million by the end of 2023 while its operating cash burn was $5.8 million and $0.3 million in capitalization of software development costs.

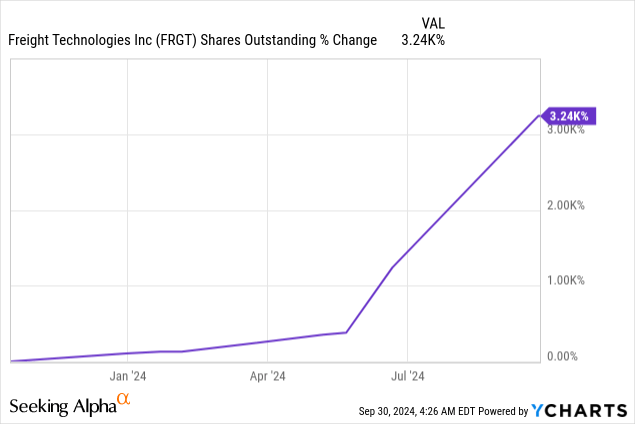

So, the company needs $5 million to $6 million to operate, and currently the company does not have that. Fr8Tech can borrow money as it borrowed $18.9 million in short-term borrowings and $7.675 million in convertible notes in 2023, but dilution risk is definitely prominent as we saw that the company converted $7.1 million of convertible notes to preferred stock and a total of $2.4 million was converted into ordinary shares. Over a 1-year period, the number of shares outstanding rose by 3.240% while the share price dropped 98%.

Conclusion: Freight Technologies Does Not Offer A Compelling Investment Case

With the dilution risk being evident and there being no sign that the company can, in fact, be profitable this year, I don't see any reason why anyone would buy let alone hold this name. I do believe that there are significant opportunities ahead, but we do need to see some firm evidence that the company actually can capitalize on digital transformation trends and cover at the very least increase its operating cash flow before I would consider any investment in this freight technology provider. As a result, I currently mark the stock as a sell as it has never been profitable and requires additional cash to cover its cash burn.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

Most Discussed

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10