Huaneng Power International (SEHK:902) Faces Earnings Decline; Strategic Alliances Key to Recovery

Huaneng Power International (SEHK:902) recently announced its earnings for the first nine months of 2024, revealing a decline in both sales and net income compared to the previous year, while maintaining a steady earnings per share from continuing operations. Despite these challenges, the company has strategically increased its electricity sales and is poised to leverage its significant debt financing capabilities to fuel future growth, with a focus on energy-efficient innovations and strategic partnerships. As the company navigates its financial hurdles, stakeholders should anticipate discussions on balancing growth opportunities with external economic threats and maintaining financial stability in the upcoming earnings call.

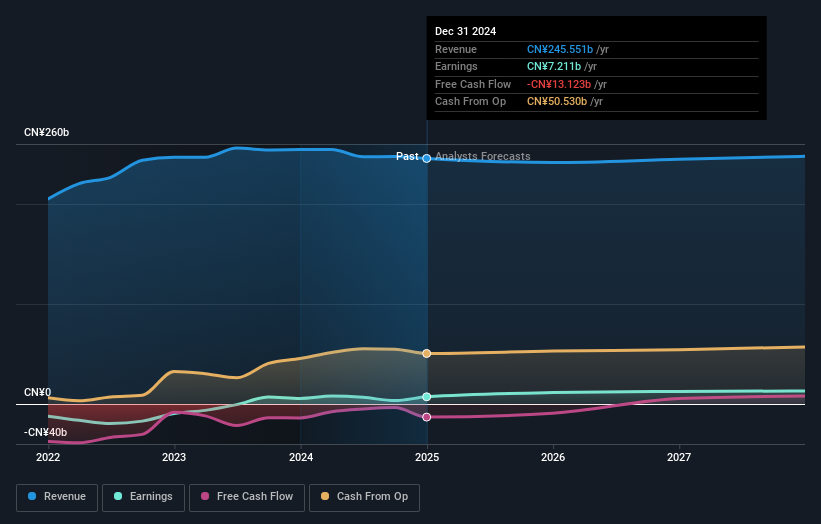

Get an in-depth perspective on Huaneng Power International's performance by reading our analysis here.

Unique Capabilities Enhancing Huaneng Power International's Market Position

With earnings projected to grow at an impressive 35.81% annually, the company demonstrates significant potential for future profitability. This positive outlook is bolstered by its current trading status, which is 91.2% below the estimated fair value, suggesting substantial upside potential. Strategic alliances and product-related announcements, such as the successful launch of energy-efficient models, underscore the company's commitment to innovation and customer satisfaction. These initiatives not only enhance market positioning but also contribute to sustained revenue growth, as evidenced by the 15% revenue increase reported earlier this year.

To gain deeper insights into Huaneng Power International's historical performance, explore our detailed analysis of past performance.Vulnerabilities Impacting Huaneng Power International

However, challenges persist, particularly with a forecasted Return on Equity of just 9.2% over the next three years. The company's revenue growth, anticipated at only 2.4% annually, lags behind the Hong Kong market average of 7.8%. This slower pace, coupled with negative earnings growth and a low net profit margin of 1.4%, highlights areas for improvement. Additionally, the board's relatively short tenure of 2.2 years may impact strategic decision-making. The high dividend payout ratio of 95.6%, not well covered by earnings, further complicates financial stability.

Learn about Huaneng Power International's dividend strategy and how it impacts shareholder returns and financial stability.Growth Avenues Awaiting Huaneng Power International

Despite these weaknesses, opportunities abound. The potential for significant earnings growth over the next three years presents a promising avenue for recovery. If managed effectively, the company could see a resurgence in profit margins and overall financial health. Strategic alliances and product innovation remain key drivers in capitalizing on emerging market opportunities, potentially enhancing the company's competitive edge.

Explore the current health of Huaneng Power International and how it reflects on its financial stability and growth potential.External Factors Threatening Huaneng Power International

Nevertheless, external threats loom large. High debt levels, inadequately covered by operating cash flow, pose a significant risk. The presence of large one-off losses could undermine investor confidence, while the unsustainable dividend may deter income-focused investors. Additionally, economic headwinds and intense market competition necessitate a careful navigation of pricing strategies and supply chain management to maintain market share and operational efficiency.

See what the latest analyst reports say about Huaneng Power International's future prospects and potential market movements.Conclusion

Huaneng Power International exhibits promising potential for future profitability, with projected earnings growth of 35.81% annually and a significant upside indicated by its trading status being 91.2% below estimated fair value. However, the company's challenges, such as a low forecasted Return on Equity of 9.2% and revenue growth trailing the market average, highlight the need for strategic improvements. Opportunities for recovery lie in leveraging strategic alliances and product innovations to boost profit margins and financial health. Yet, external threats, including high debt levels and economic headwinds, necessitate prudent financial management and strategic decision-making to ensure sustainable growth and investor confidence, particularly given the absence of a specific valuation summary to guide expectations.

Summing It All Up

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

Valuation is complex, but we're here to simplify it.

Discover if Huaneng Power International might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Simply Wall St and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

Most Discussed

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10