This Is Why Butn Limited's (ASX:BTN) CEO Compensation Looks Appropriate

Key Insights

- Butn to hold its Annual General Meeting on 14th of November

- CEO Walter Rapoport's total compensation includes salary of AU$273.0k

- The total compensation is 34% less than the average for the industry

- Butn's EPS grew by 88% over the past three years while total shareholder loss over the past three years was 79%

The performance at Butn Limited (ASX:BTN) has been rather lacklustre of late and shareholders may be wondering what CEO Walter Rapoport is planning to do about this. One way they can exercise their influence on management is through voting on resolutions, such as executive remuneration at the next AGM, coming up on 14th of November. It has been shown that setting appropriate executive remuneration incentivises the management to act in the interests of shareholders. We have prepared some analysis below to show that CEO compensation looks to be reasonable.

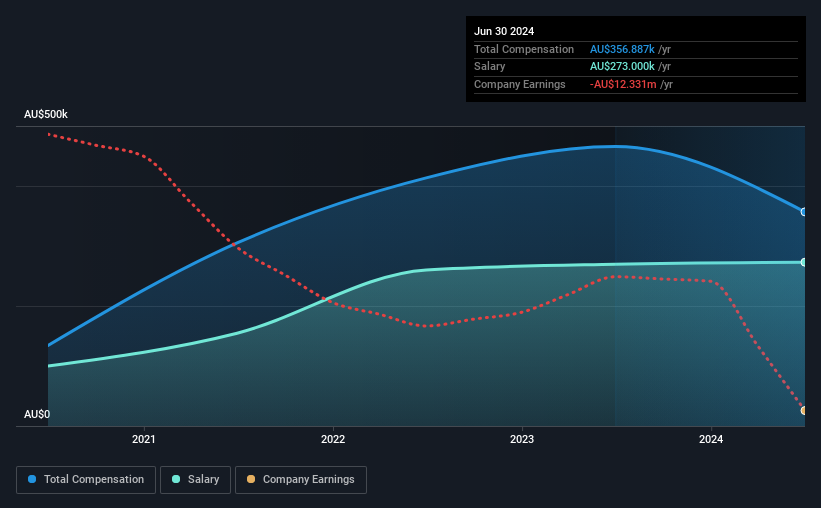

View our latest analysis for Butn

How Does Total Compensation For Walter Rapoport Compare With Other Companies In The Industry?

According to our data, Butn Limited has a market capitalization of AU$17m, and paid its CEO total annual compensation worth AU$357k over the year to June 2024. Notably, that's a decrease of 23% over the year before. In particular, the salary of AU$273.0k, makes up a huge portion of the total compensation being paid to the CEO.

For comparison, other companies in the Australian Diversified Financial industry with market capitalizations below AU$302m, reported a median total CEO compensation of AU$543k. Accordingly, Butn pays its CEO under the industry median. Moreover, Walter Rapoport also holds AU$2.4m worth of Butn stock directly under their own name, which reveals to us that they have a significant personal stake in the company.

| Component | 2024 | 2023 | Proportion (2024) |

| Salary | AU$273k | AU$270k | 76% |

| Other | AU$84k | AU$196k | 24% |

| Total Compensation | AU$357k | AU$466k | 100% |

Talking in terms of the industry, salary represented approximately 67% of total compensation out of all the companies we analyzed, while other remuneration made up 33% of the pie. It's interesting to note that Butn pays out a greater portion of remuneration through salary, compared to the industry. If salary dominates total compensation, it suggests that CEO compensation is leaning less towards the variable component, which is usually linked with performance.

Butn Limited's Growth

Butn Limited has seen its earnings per share (EPS) increase by 88% a year over the past three years. In the last year, its revenue is up 8.5%.

This demonstrates that the company has been improving recently and is good news for the shareholders. It's also good to see modest revenue growth, suggesting the underlying business is healthy. We don't have analyst forecasts, but you could get a better understanding of its growth by checking out this more detailed historical graph of earnings, revenue and cash flow.

Has Butn Limited Been A Good Investment?

Few Butn Limited shareholders would feel satisfied with the return of -79% over three years. Therefore, it might be upsetting for shareholders if the CEO were paid generously.

To Conclude...

The fact that shareholders have earned a negative share price return is certainly disconcerting. The share price trend has diverged with the robust growth in EPS however, suggesting there may be other factors that could be driving the price performance. A key focus for the board and management will be how to align the share price with fundamentals. In the upcoming AGM, shareholders should take this opportunity to raise these concerns with the board and revisit their investment thesis with regards to the company.

We can learn a lot about a company by studying its CEO compensation trends, along with looking at other aspects of the business. We did our research and identified 4 warning signs (and 2 which make us uncomfortable) in Butn we think you should know about.

Switching gears from Butn, if you're hunting for a pristine balance sheet and premium returns, this free list of high return, low debt companies is a great place to look.

Valuation is complex, but we're here to simplify it.

Discover if Butn might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

Most Discussed

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10