HUYA Inc.: Regulatory Challenges And Valuation Concerns Loom Large

- HUYA Inc. is down over 86% in five years, nearing its 52-week low, and has a declining Quant Rating, now at a Sell.

- The company faces high costs in a saturated market, with low switching costs for users and ongoing share dilution impacting value.

- HUYA Inc. has had retained earnings losses for eight straight years, with rising expenses outpacing net profit, and free cash flow per share in decline.

- Despite potential support from parent company Tencent, HUYA Inc.'s strategy to reduce costs and improve margins raises concerns about its long-term profitability.

whitebalance.oatt/E+ via Getty Images

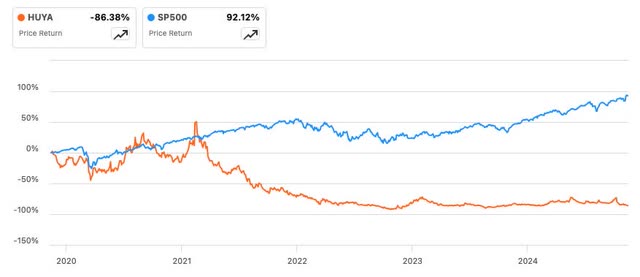

When I looked at historical returns for HUYA Inc. (NYSE:HUYA) I thought I might find a stock that had been oversold and present me with a buying opportunity. HUYA Inc. is down more than 86% over the last five years and is nearing its 52-week low of $2.93. HUYA Inc. just closed at $3.08 and has three Wall Street Analysts giving the stock a "Buy" rating and six giving it a "Strong Buy".

HUYA Inc. vs. S&P 500 (5-Year) (Seeking Alpha)

When I took a closer look, what I saw was a mediocre business that continues to lose money year after year. HUYA Inc. delivered Q3 2024 Quarterly Earnings on November 12, 2024, that beat analyst's expectations on revenue and EPS, and yet the stock not only fell over 5% in midday trading, the company was issued a "high risk" warning by Seeking Alpha on that same day.

I believe HUYA Inc. is in an incredibly saturated market with little upside for the future. Switching costs are low for their users, expenses will continue to rise year after year to maintain streamers and esports tournaments, and the company continues to dilute the value of their shares with repeated stock issuances.

Company Overview

HUYA Inc. was founded in 2014 with headquarters in Guangzhou, China. The company operates several live-streaming platforms in China and other markets. Its platforms allow users to broadcast and viewers to interact during live streams. Although HUYA Inc.'s primary focus is gaming, the company also covers life and other entertainment content like talent shows, outdoor activities, anime, live chats, and online theater. Further, it operates Nimo TV, a game live-streaming platform that serves international markets.

In addition, the company sells online advertising, internet value software development, and creative and cultural services. HUYA Inc. is a subsidiary of Tencent Holdings Limited (OTCPK:TCEHY).

Business Analysis

HUYA Inc. is the largest live-streaming platform in China with 84.1 million monthly active users (MAUs) according to the company's 2023 Annual Report. The company has maintained its live-streaming lead by signing exclusive licensing deals with eSports tournaments. In my view, the company believes these licensing deals enhance user loyalty to their platform. However, competition for these tournaments is fierce, and I believe the costs of these licensing deals will only continue to rise in the future.

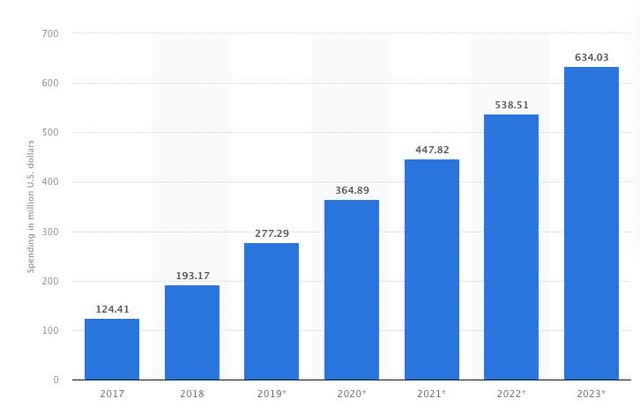

The chart below shows companies spending on eSports Advertising & Sponsorships Worldwide from 2017 to 2023.

eSports Spending Advertising & Sponsorships (Statista)

Advertising and Sponsorship payments have risen since 2017, and I believe this trend will only continue as companies compete for top-tier streamers and tournaments. This trend will put more pressure on HUYA Inc. to generate larger returns on each dollar they spend on tournaments and top talent.

Generating a return on those dollars might become more difficult in the future. Kellogg School of Management at Northwestern University recently published a report that shows just how hard it is to generate returns on streaming. The article highlighted an estimate put out by The Wall Street Journal suggesting that Activision Blizzard and Electronic Arts have spent an estimated $50,000 per hour for top talent on Twitch.

More interestingly, the question is asked if that kind of investment is typically worth it. According to research by Ilya Morozov, an assistant professor of marketing at the Kellogg School, it usually isn't worth the investment. Morozov was quoted saying, "For most of the games in our data, [sponsored streams] are not effective at all-the return on investment is deeply negative".

A Flashing Red Quant Rating

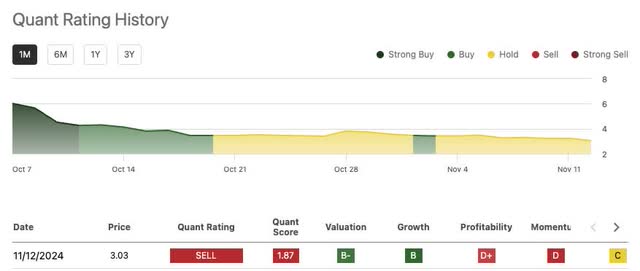

The Quant Rating for HUYA Inc. is in free fall. On October 7, 2024, HUYA Inc.'s Quant Rating was 4.70, a Strong Buy. But the rating has been on a downhill slope ever since. On November 12, 2024, the company hit a one-year low of 1.87, a Sell. The company hasn't been in a Quant Rating Sell since October 10, 2023, which is more than one year ago.

Quant Rating History (Seeking Alpha)

Quant Rankings are a measure used by Seeking Alpha to compare the stock to others in a similar sector based on an objective and quantitative view. The rankings are determined by an instant summary of information and data including the company's financial results, available data about the stock, and sell-side analyst's estimates of future earnings and revenue.

Free Cash Flow/Share Is In Free Fall

When I want to know how much money a company has to spend to keep the business running, I like to look at Free Cash Flow Per Share (FCF). FCF is how much cash a business generates per share after dividends have been paid. For a business like HUYA, I believe that their model for paying high costs for high-profile eSports tournaments is going to take a lot of expenses to maintain and is going to continue to be competitive as other companies attempt to bid for high-profile eSports tournaments.

In December of 2019, the company's FCF was $1.25 per share. In December 2023, it was -$0.09 per share.

More Shares More Problems

As a value investor, I want to own companies that increase in value over time. The stock market is filled with companies that lose value every year. Declining revenue, declining net profit, and even declining net profit margin can fluctuate up and down even for successful companies. Still, in my view, the number of shares outstanding is a financial tool that automatically dilutes the value of the company except in scarce circumstances.

Warren Buffett has often stated how much he values share buybacks (which reduce the number of shares outstanding) and in his 2022 letter to shareholders he said anyone criticizing stock buybacks is "either an economic illiterate or a silver-tongued demagogue".

HUYA Inc. has issued additional stock every single year since 2016.

HUYA Inc.'s Issuance of Stock (Seeking Alpha)

This has put a strain on the company's value even when Revenues may be growing, value is being swallowed up by putting more shares on the market. This strain shows up in the Retained Earnings for HUYA Inc.

Retained Earnings Negative For Eight Straight Years

Retained Earnings are a company's cumulative net profit after the company has paid its dividend. In essence, it is the profit left over after expenses have been paid and shareholders have been paid their dividends. I like this number as a deep look inside of a company's financial picture because it accounts for expenses that a business has to account for but that can often be overlooked by investors when evaluating top-line metrics, like revenue, or EPS.

HUYA Inc. has had a Retained Earnings loss for eight straight years.

HUYA Inc.'s Retained Earnings (Seeking Alpha)

One of the reasons I think this is happening is because the expenses to maintain streamers and eSports tournaments far outweigh the net profit that HUYA is generating. In addition, when the company continues to issue stock diluting the net profit, it is becoming increasingly difficult for HUYA to retain any of those earnings.

Capital Expenditures have ballooned from $5.7 million in 2017 to $22.7 million in 2023. Shares Outstanding have swelled from $100 million in 2016 to $223.9 in 2023, while net income has bounced around from a loss of $90.1 million to a loss of $28.8 million in 2023.

Regulatory Challenges

China has shown interest in recent years in trying to curb time spent on gaming, especially among younger consumers, highlighting concerns of addiction. In December 2023, the Chinese regulators announced they would be placing limits on how much users can spend on online games.

If this concern continues among regulators and the Chinese government, this poses a vast risk for HUYA because their business model is central to the streaming community spending time participating in and watching live streams. HUYA's growth model is central to getting more users to watch live streams and spend money on live-streaming. If regulators continue to implement rules to curb online gaming, this could limit HUYA Inc.'s ability to grow.

In August 2024, China announced it would begin considering transfers of cryptocurrencies inside games as money laundering activity. Regulators stated that the rise of criminal activity has led them to crack down on this kind of transaction, potentially limiting spending inside online games. This highlights the Chinese government's willingness to take action on creating regulations even when it may interfere with online gaming companies.

Valuation Concerns

In my view, HUYA Inc.'s valuation is a concern, especially in comparison to its peer group. The company's Price / Cash Flow (FWD) is 42.52 while the sector median is 8.41. As I highlighted earlier, Free Cash Flow / Share has been in decline, which is not a good sign, but looking towards the future, the Price / Free Cash Flow on a forward basis is much higher than the sector median.

In addition, Valuation Factor Grades from Seeking have declined to a C+ after being an A+ 3 months ago and an A+ six months ago. In comparison, competitors DoubleDown Interactive Co., Ltd. (DDI) ranks an A for valuation, PLAYSTUDIOS, Inc. (MYPS) is an A, and Sohu.com Limited (SOHU) is a B-, all higher than HUYA Inc.

Potential Risks

HUYA Inc. is a subsidiary of Tencent Holding Limited. Tencent Holding Limited is a juggernaut in the Chinese market and currently holds $24.27 billion in cash on its balance sheet. If HUYA Inc. were to continue with losses into the foreseeable future, few companies have the luxury of a parent company with the size and strength of Tencent.

If HUYA Inc. needed a cash infusion or any kind of bailout, Tencent would be able to easily support any financial trouble HUYA Inc. may encounter with their enormous war chest of cash.

In addition, the streaming business is still growing and is expected to continue to grow in the foreseeable future. According to market insights by Statista, revenue in eSports is expected to maintain an annual growth rate (CAGR 2024-2029) of 6.59%. This will grow to a projected market volume of $5.9 billion by 2029. There is a large market of opportunity out there for HUYA Inc. and if they can find a way to capture more of this revenue they will have a chance to grow.

Conclusion

In HUYA Inc.'s Q3 Earnings Call, acting Co-CEO and SVP, Jun Hong Huang was asked a question about plans for expanding Huya's market presence. He responded by saying, "We plan to deepen collaborations with content creators and industry partners, expand our game distribution services, and explore broader cooperation with game developers to unlock new commercialization opportunities and support long-term business development."

In addition, in his opening remarks Junhong Huang outlined plans to reduce costs and improve margins by saying, "We entered into a second supplemental license agreement for a series of League of Legends matches that decreased the license fee, which, we believe, will help us further reduce our overall eSports license costs this year and in 2025."

In my view, this is a concerning strategy considering it dilutes the value of the core product of live-streaming, and I believe is another indication that the company is struggling to garner strong profit from exclusive eSports tournaments.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

Most Discussed

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10