ATRenew Reports Strong Q3 Earnings, Growth Likely To Continue

- ATRenew's 3Q 2024 earnings report shows a 24.4% sales increase and a shift from operational loss to profit, driven by cost optimizations and lower amortization expenses.

- The company's multi-category recycling business surged by 270% YOY, and its 1P-to-consumer sales increased by 120% YOY, indicating strong market demand.

- ATRenew's strong cash and debt fundamentals, along with sustainable sales growth, suggest potential for future net GAAP profitability and stock appreciation.

- The growing popularity of the circular economy in China and government support provide significant upside factors for ATRenew's continued success.

Tomasz Śmigla

ATRenew (NYSE:RERE) has just reported its 3Q 2024 earnings. As usual, the company has published better results compared to the same period a year ago. The management's outlook remains positive.

Previous Article About ATRenew

In my previous article, I also covered ATRenew's quarterly earnings. The company reported very sound results for Q2 2024. At the time, ATRenew's sales increased by 27.4% year-over-year.

I also wrote that the company's balance sheet was strong while its operating losses declined, which suggests that the company has a very strong and healthy cash flow.

In fact, the recently reported 3Q 2024 sales improved compared to 3Q 2023 and even the previous successful 2Q 2024. The 3Q 2024 was the best quarter over more than three years' time in terms of sales revenues. But let me give you some more details.

Quarterly Earnings Report

As I have just mentioned above, the sales revenues and profitability figures have demonstrated sustainable progress. But here is a more detailed summary of ATRenew's financial performance:

- Total sales increased by 24.4% to RMB4.05 billion, or $577.3 million, versus RMB3.26 billion in the 3Q 2023.

- ATRenew's income from operations totaled RMB24.9 million, or $3.5 million, versus the operational loss of RMB28.1 million in 3Q 2023.

- Adjusted income from operations (non-GAAP, that is) totaled RMB104.0 million, or $14.8 million, versus the RMB73.8 million in 3Q 2023.

- The quantity of consumer products transacted totaled 9.1 million versus 8.2 million in 3Q 2023.

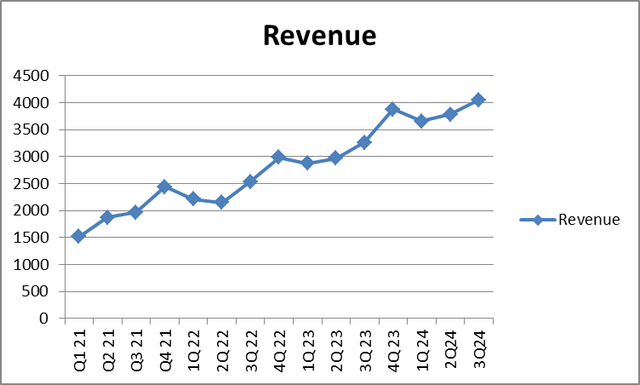

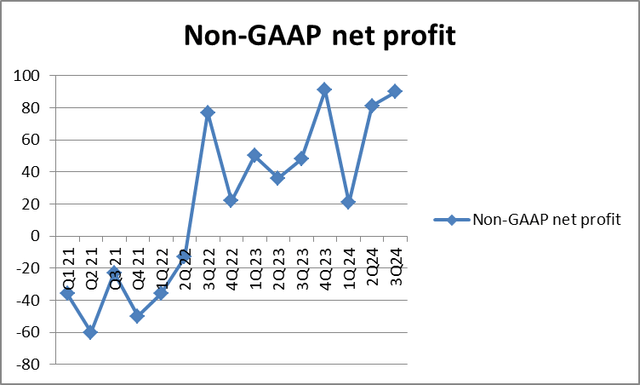

Below I have prepared a quarterly sales and earnings table and also several diagrams to show ATRenew's progress. Obviously, apart from the brilliant revenues, we can also see that the non-GAAP net profit was also higher compared to the RMB81 million reported in the previous quarter.

RERE quarterly earnings (in RMB million)

Prepared by the author based on ATRenew's data

As can be seen from the diagrams below, ATRenew's sales are rising sustainably at a reasonably fast pace. The non-GAAP net profit has been staying at a reasonable level since 3Q 2022. Also, the RMB90 million in non-GAAP profit is higher than the RMB77 million recorded two years ago.

Prepared by the author based on ATRenew's data Prepared by the author based on ATRenew's data

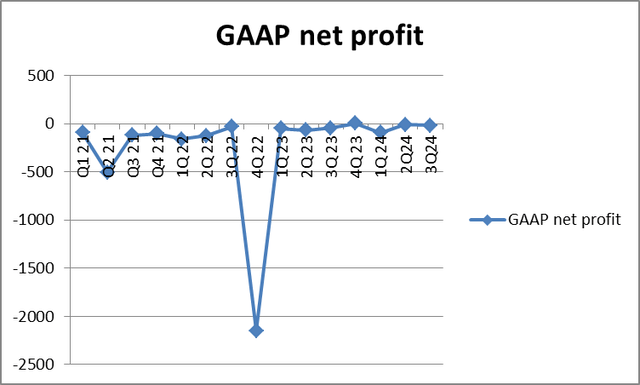

Only the GAAP net profit has stayed almost unchanged since 1Q 2023.

Prepared by the author based on ATRenew's data

According to Rex Chen, ATRenew's CFO, the company's results are due to cost optimizations and lower amortization expenses. The company also bought back more than $12 million worth of its own shares during the quarter. This also demonstrates that ATRenew places a strong emphasis on shareholder returns.

The Management's Outlook

For the next quarter, ATRenew's management expects that sales will total between RMB4.74 billion and RMB4.84 billion, representing a rise of 22.4% to 24.9% YOY. But let me go into more detail about the management's business forecasts.

First, let us talk about the market for pre-owned smartphones, which is ATRenew's main source of income.

Although ATRenew has not directly benefited from the government's subsidy policies just yet, under the national trade-in initiative, the company's cross-category trade-in capabilities have allowed ATRenew to better capture consumer-end recycling sources. Also, the company has its own technologies to improve pre-owned product quality, thus boosting sales. Thanks to the fact that the company is more effective at identifying products suitable for reconditioning, its revenues have been increasing on both a quarterly and annual basis.

As concerns retail distribution, ATRenew's 1P-to-consumer sales increased by 120% year-over-year. Sales from AHS offline stores and official websites rose by more than 300% year on year. According to the management, cheaper products are getting more popular among the mass market consumers. So, even more growth is expected next quarter and also next year.

Now moving on to the multi-category recycling business. It is an asset-light platform business model. The segment's purpose is to give a second life to luxury goods, including gold, jewelry, exclusive alcohol, and similar items. In the past quarter, the value of this business surged by 270% year-over-year and generated 30 million in service revenue. This business segment is

Of ATRenew's 769 self-operated AHS stores, 587 currently offer multi-category recycling services that are able to serve many customers in first- and second-tier Chinese cities. But more is yet to come as ATRenew is expanding its network.

Business Fundamentals

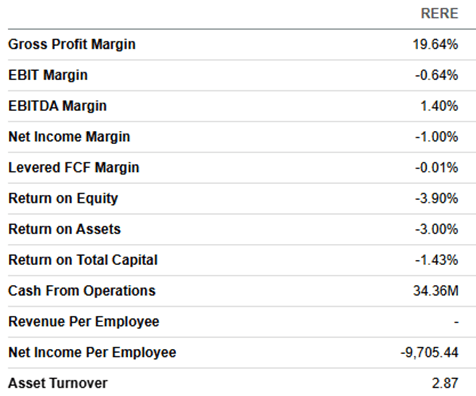

As concerns ATRenew's business fundamentals, it has a sound gross profit margin but a negative net profit margin. But it is currently better than it used to be before. And if the company's sales and income from operations keep growing, its net income will finally turn positive.

Seeking Alpha

Much better are the company's cash and debt fundamentals. ATRenew's net debt is negative, which means that its debt is lower than its cash reserves.

Also, the company's current ratio and quick ratios are reasonable, suggesting enough cash on hand to carry out its day-to-day operations.

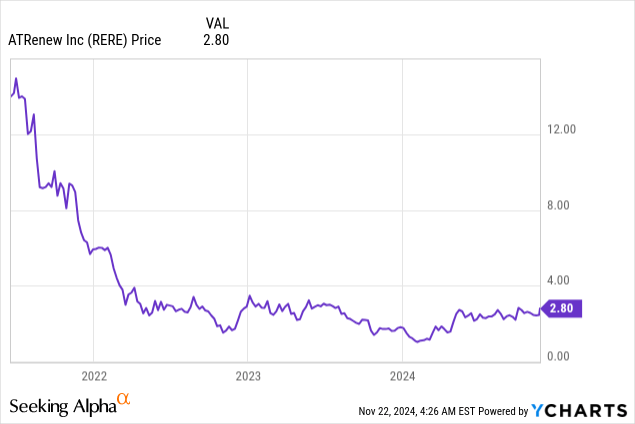

Valuations

As concerns ATRenew's valuations, the company's stock is trading at 52-week highs. However, it is still very low compared to its post-IPO price of about $15 per share.

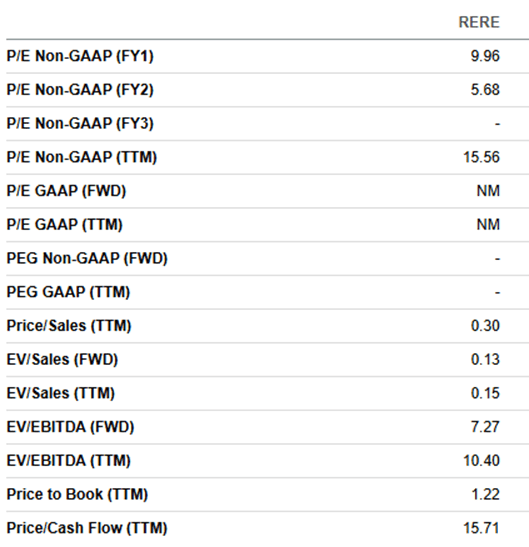

ATRenew does not record any positive GAAP net profits. But its non-GAAP price-to-earnings (P/E) ratios are reasonable. A P/E ratio below 20 is generally considered reasonable.

Seeking Alpha

The price-to-sales and price-to-book ratios are very moderate. Both of these indicators are typically within the 1-to-3 range.

Upside Factors

ATRenew has very sustainable sales growth despite the fact that it is not currently recording a net profit. However, as I have mentioned above, ATRenew's operating and net profits have been improving, and it seems likely the company would report a positive net GAAP profit. As soon as it happens, RERE stock would likely appreciate over and above the current levels.

The concept of the "circular economy" is gaining popularity in China. Therefore, consumer behavior is changing. This means that responsible consumption and recycling are getting more popular. This could further stimulate demand for ATRenew's products. Moreover, the Chinese government is also facilitating the development of China's circular economy. This should create additional market opportunities for green enterprises.

Also, ATRenew's direct-to-consumer sales have been very strong because of consumers' high demand for pre-owned products. Various distribution channels enable ATRenew to meet the growing consumer demand for pre-owned electronic goods. In the past quarter, 1PtoC product revenue through Paipai on JD.com, AHS Recycle official websites and stores, and new media retail channels increased by 87.4%, 301.3%, and 114.6% YOY, respectively.

Risks

Conservative US-based investors might prefer to buy stocks of highly profitable American companies. They might feel skeptical about ATRenew because it is a Chinese company and does not have a sound net profitability track record. However, ATRenew has a sustainable track record of improving revenues and earnings. Moreover, ATRenew's business is unlikely to be impacted by deteriorating US-China relations because the company's operations are based in China and target Chinese consumers.

Also, some stockholders might prefer the company to pay dividends instead of buying back its own shares. Although I fully agree with them, it is likely ATRenew would start paying dividends when its profitability improves.

Conclusion

Overall, we can safely say that ATRenew is making very good progress. The market for recycled goods is growing, the company's sales are rising too, its cash and debt metrics remain very sound. Given ATRenew's rising sales, the company is likely to start recording net profits and paying dividends soon. Its partnership with JD.com and also the Chinese government's circular economy concept are also significant upside factors.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

Most Discussed

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10