Autohome: Questionable Value Amid Industry Disintermediation

- Autohome's 3Q24 performance is hindered by China's weak advertising environment and macroeconomic challenges, affecting consumer spending and OEM profitability.

- ATHM's vertical-focused advertising model faces competition from platforms like Douyin, Little Redbook, and DTC channels, risking further disintermediation.

- The Space Store model's value-add is questionable, as most car buyers conduct initial research online, reducing the need for ATHM's offline services.

- Given the deteriorating fundamentals and uncertain stimulus measures, ATHM's dividend sustainability and share price outlook remain negative, advising investors to avoid the stock.

Hispanolistic/E+ via Getty Images

Autohome’s (NYSE:ATHM) 3Q24 financial performance highlighted that the company continues to be negatively impacted by a combination of macro and fundamental challenges.

On the macro side, China’s advertising environment remains challenging as both OEMs and dealerships rethink their advertising strategy and focus more on ROI. In addition, stagnating wage growth, weak employment prospects and diminishing wealth effects from the weak properties market are forcing consumers to rethink their large discretionary purchases. Finally, the hyper-competitive price war among the automakers that has been ongoing for the past two years has been weighing on the profitability of the OEMs, thereby negatively impacting the marketing budget.

On the micro side, China’s weak advertising environment is giving ATHM very limited room to pivot and drive revenue growth. The company essentially has to accept the gradual erosion of its fundamentals until there is a clear policy stimulus to drive consumer spending, something that remains uncertain in the wake of the underwhelming RMB 10 trillion stimulus that was announced recently. Although the company is attempting to pursue new models such as the Space Store, this model does not address any of the demand challenges faced by the OEMs or the dealerships, and its value to the consumers remains questionable.

On a more structural basis, ATHM’s vertical-focused advertising model is starting to become debatable as a number of alternative platforms such as Douyin/TikTok, Little Red Book, and DTC channels that OEMs and dealers can rely on for customer acquisition and retention. While we believe that ATHM continues to have some value and remain relevant in the foreseeable future, we believe the disintermediation of advertising verticals is a key risk that ATHM investors should be mindful of.

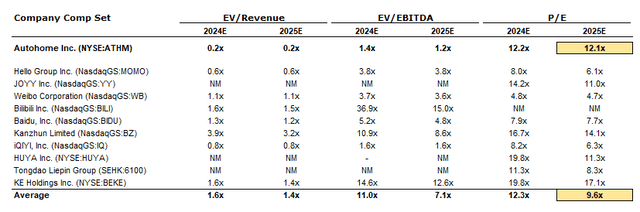

ATHM is currently trading at 12x 2015E earnings, with consensus expecting almost no EPS growth for the year. The current valuation is close to the company’s cash value per share, which may imply an attractive margin of safety when factoring in the RMB 1.5bn (or US$210mn) annual cash dividend that implies a 6.2% dividend yield.

Capital IQ, Astrada Advisors

However, we question the sustainability of the dividend payout when looking at the cash inflow and outflow. We note that the company is expected to generate around RMB 2bn in operating cash flow for 2015E, netting out an estimated RMB 200mn in annual capex and the RMB 1.5bn in cash dividend would translate to RMB 300mn in annual net cash increase.

We do not believe that this RMB 300mn annualized cash increase is a sufficient buffer if ATHM's topline continues to decline and capex increases due to the expansion of the offline locations, which could easily result in net cash decline thereby negatively impacting the current cash holdings and potentially force the management to rethink the existing dividend policy. Without a clear stimulus measure to drive discretionary consumption, we believe that ATHM share price could further de-rate in 2025 and lead to multiple contraction despite the dividend payout and large cash level.

Weak macro continues to weigh on revenue growth.

Consistent with the narrative for the past year, China’s weak macro environment has driven consumers to pull back on large ticket discretionary spending, such as automotive, and this resulted in OEMs and dealerships resorting to aggressive price competition to stimulate demand. The declining profitability among OEMs and dealerships has made them rethink their advertising strategy, therefore pulling back on ad budget allocation for vertical-focused platforms such as ATHM.

We note that for the first nine months of the year, the average profit margin for the auto industry was only 4.6% compared with the industrial enterprise profit margin of 6.1% over the same period.

The declining profitability amongst the OEMs has made them pull back on ad allocation, which negatively impacted ATHM’s media service business, which relies on branded advertisements from the OEMs. The dealership landscape is equally competitive. According to the China Automobile Dealers Association report, dealerships are also facing high operating pressure with less than 30% of auto dealers accomplishing their sales target in 1H24, which led to many dealerships sacrificing price to drive volume. This systemic price war increased the proportion of dealers operating under loss to over 50%. Given the aggressive price war, many OEMs and dealerships have shifted towards more performance-based advertising given the relocation of budget.

Space Stores’ value-add remains debatable.

ATHM is looking to find a new revenue growth model with the introduction of its Space Stores, a chain of offline locations that offer a one-stop shop for EV purchases and used car transactions. Key features of the Space Store are an integration of the online and offline channels and offer consumers the convenience of comparing different models and brands.

The value-add behind this strategy is to find new growth drivers in the offline segment as online advertising is likely to decline in the near term, position ATHM as a middleman helping consumers with their purchasing decision process, and simplifying the car purchase process by saving the consumers time and effort of visiting multiple dealerships.

In theory, this model seems to have some value-add, but we question this model's actual relevance among consumers and its scalability.

We understand that car buyers often become indecisive on which model or brand to purchase, coupled with the inconvenience of doing multiple dealership runs, test drives and price haggling to get the ideal car. However, we wonder if ATHM management has overestimated the demand originating from this scenario given that many car buyers would have conducted initial due diligence on the model and brand and usually have a preference towards one or two brands before hitting the offline location (i.e. dealerships). For ATHM to offer recommendations and avoid the need to visit multiple dealerships seems to be a service catered to a potential buyer that did very limit to no initial homework on the car they wish to purchase. This scenario seems very unlikely, in our view, given automotive is no small purchase and every buyer usually conducts some sort of online due diligence before pivoting to an offline experience. Therefore, we question the actual value of ATHM’s new online offline strategy.

The questionable value of advertising vertical

A notable theme within China’s automotive advertising space is that OEMs, dealerships, and influencers are increasingly connecting with consumers directly through reviews and test drives, thereby diminishing the relevance of traditional vertical-focused platforms such as ATHM.

Worth noting that ATHM’s original value-add was to connect OEMs and dealerships with potential buyers. However, given the disintermediation of vertical ad platforms, consumers can easily access relevant automotive information and connect with OEMs and dealerships through platforms such as Little Red Book, Douyin/TikTok, OEM’s DTC channels and dealerships’ social media sites, in addition to ATHM.

The proliferation of content platforms resulted in higher conversion costs within the traditional lead generation platforms such as ATHM, making content-driven platforms more attractive to the OEMs and the dealerships given their easier integration with social media and lower user acquisition cost. We note that user acquisition cost was only a few hundred RMB pre-2020 but has surged to over RMB2,200 in 2023. On the other hand, Douyin’s user acquisition cost is only RMB25.

Not only is ATHM losing relevance in lead generation and user acquisition, but it is also losing to Tencent in terms of lead management. Often we see OEMs and dealerships connect with potential consumers over WeChat, which allows advertisers to engage consumers through familiar and trusted channels such as public accounts and live-streaming, thereby further diminishing ATHM’s relevance in terms of consumer mind share.

In conclusion, we are negative on ATHM and believe that investors should avoid this stock given its exposure to China's soft ad environment and hyper-competitive auto segment that is seeing advertisers relocating their budget due to declining profitability. We do not find its cash position and dividend to provide an attractive margin of safety for investors, as a prolonged economic slump may not result in dividend sustainability due to weakening cash flow generation.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

Most Discussed

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10