The E.W. Scripps Company (NASDAQ:SSP) institutional owners may be pleased with recent gains after 68% loss over the past year

Key Insights

- Given the large stake in the stock by institutions, E.W. Scripps' stock price might be vulnerable to their trading decisions

- The top 22 shareholders own 51% of the company

- Insiders have bought recently

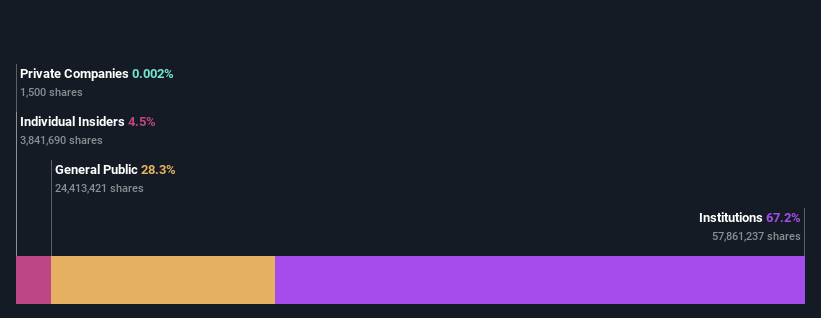

Every investor in The E.W. Scripps Company (NASDAQ:SSP) should be aware of the most powerful shareholder groups. The group holding the most number of shares in the company, around 67% to be precise, is institutions. Put another way, the group faces the maximum upside potential (or downside risk).

Institutional investors would probably welcome last week's 16% increase in the share price after a year of 68% losses as a sign that returns may to begin trending higher.

Let's delve deeper into each type of owner of E.W. Scripps, beginning with the chart below.

Check out our latest analysis for E.W. Scripps

What Does The Institutional Ownership Tell Us About E.W. Scripps?

Institutional investors commonly compare their own returns to the returns of a commonly followed index. So they generally do consider buying larger companies that are included in the relevant benchmark index.

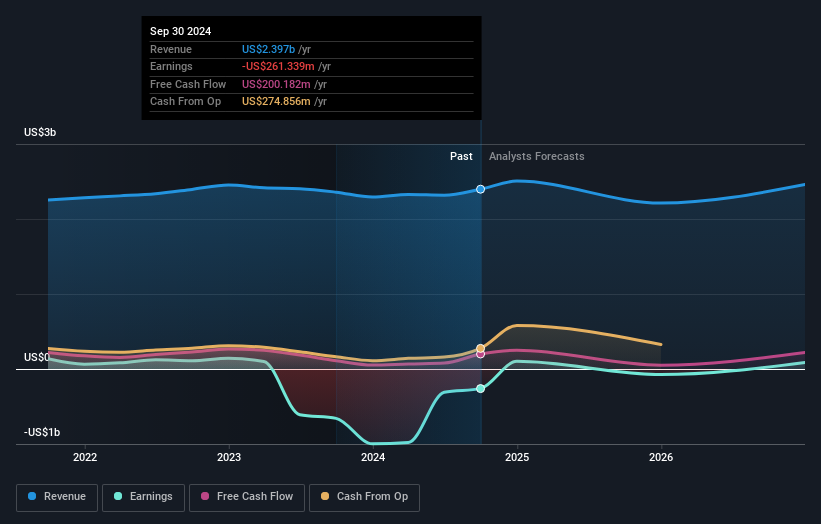

We can see that E.W. Scripps does have institutional investors; and they hold a good portion of the company's stock. This implies the analysts working for those institutions have looked at the stock and they like it. But just like anyone else, they could be wrong. When multiple institutions own a stock, there's always a risk that they are in a 'crowded trade'. When such a trade goes wrong, multiple parties may compete to sell stock fast. This risk is higher in a company without a history of growth. You can see E.W. Scripps' historic earnings and revenue below, but keep in mind there's always more to the story.

Since institutional investors own more than half the issued stock, the board will likely have to pay attention to their preferences. We note that hedge funds don't have a meaningful investment in E.W. Scripps. BlackRock, Inc. is currently the largest shareholder, with 6.2% of shares outstanding. For context, the second largest shareholder holds about 5.3% of the shares outstanding, followed by an ownership of 4.7% by the third-largest shareholder. Furthermore, CEO Adam Symson is the owner of 0.6% of the company's shares.

A closer look at our ownership figures suggests that the top 22 shareholders have a combined ownership of 51% implying that no single shareholder has a majority.

While studying institutional ownership for a company can add value to your research, it is also a good practice to research analyst recommendations to get a deeper understand of a stock's expected performance. Quite a few analysts cover the stock, so you could look into forecast growth quite easily.

Insider Ownership Of E.W. Scripps

The definition of company insiders can be subjective and does vary between jurisdictions. Our data reflects individual insiders, capturing board members at the very least. Management ultimately answers to the board. However, it is not uncommon for managers to be executive board members, especially if they are a founder or the CEO.

I generally consider insider ownership to be a good thing. However, on some occasions it makes it more difficult for other shareholders to hold the board accountable for decisions.

Shareholders would probably be interested to learn that insiders own shares in The E.W. Scripps Company. It has a market capitalization of just US$195m, and insiders have US$8.7m worth of shares, in their own names. This shows at least some alignment, but we usually like to see larger insider holdings. You can click here to see if those insiders have been buying or selling.

General Public Ownership

The general public-- including retail investors -- own 28% stake in the company, and hence can't easily be ignored. This size of ownership, while considerable, may not be enough to change company policy if the decision is not in sync with other large shareholders.

Next Steps:

I find it very interesting to look at who exactly owns a company. But to truly gain insight, we need to consider other information, too. To that end, you should be aware of the 1 warning sign we've spotted with E.W. Scripps .

But ultimately it is the future, not the past, that will determine how well the owners of this business will do. Therefore we think it advisable to take a look at this free report showing whether analysts are predicting a brighter future.

NB: Figures in this article are calculated using data from the last twelve months, which refer to the 12-month period ending on the last date of the month the financial statement is dated. This may not be consistent with full year annual report figures.

Valuation is complex, but we're here to simplify it.

Discover if E.W. Scripps might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

Most Discussed

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10