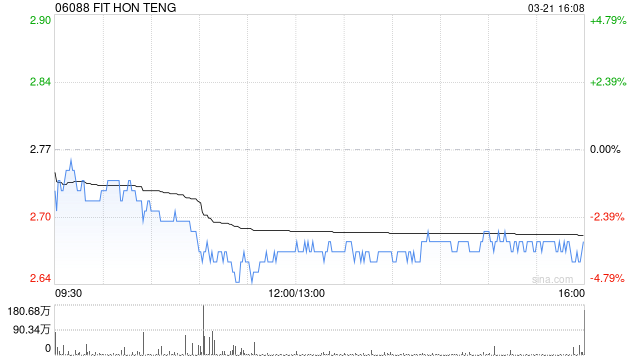

FIT HON TENG(鸿腾精密)将于3月中旬披露去年第四季及全年业绩,该行料其去年收入及纯利分别为45.55亿及1.79亿美元,同比分别增长9%及39%,去年第四季收入与纯利同比增长5%及6%,至13.13亿与7,840万美元,大致符合公司指引及市场预期。

海量资讯、精准解读,尽在新浪财经APP

责任编辑:史丽君

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.