Here's Why Wasion Holdings (HKG:3393) Has Caught The Eye Of Investors

For beginners, it can seem like a good idea (and an exciting prospect) to buy a company that tells a good story to investors, even if it currently lacks a track record of revenue and profit. Sometimes these stories can cloud the minds of investors, leading them to invest with their emotions rather than on the merit of good company fundamentals. While a well funded company may sustain losses for years, it will need to generate a profit eventually, or else investors will move on and the company will wither away.

So if this idea of high risk and high reward doesn't suit, you might be more interested in profitable, growing companies, like Wasion Holdings (HKG:3393). Even if this company is fairly valued by the market, investors would agree that generating consistent profits will continue to provide Wasion Holdings with the means to add long-term value to shareholders.

See our latest analysis for Wasion Holdings

Wasion Holdings' Earnings Per Share Are Growing

If a company can keep growing earnings per share (EPS) long enough, its share price should eventually follow. So it makes sense that experienced investors pay close attention to company EPS when undertaking investment research. Wasion Holdings' shareholders have have plenty to be happy about as their annual EPS growth for the last 3 years was 38%. That sort of growth rarely ever lasts long, but it is well worth paying attention to when it happens.

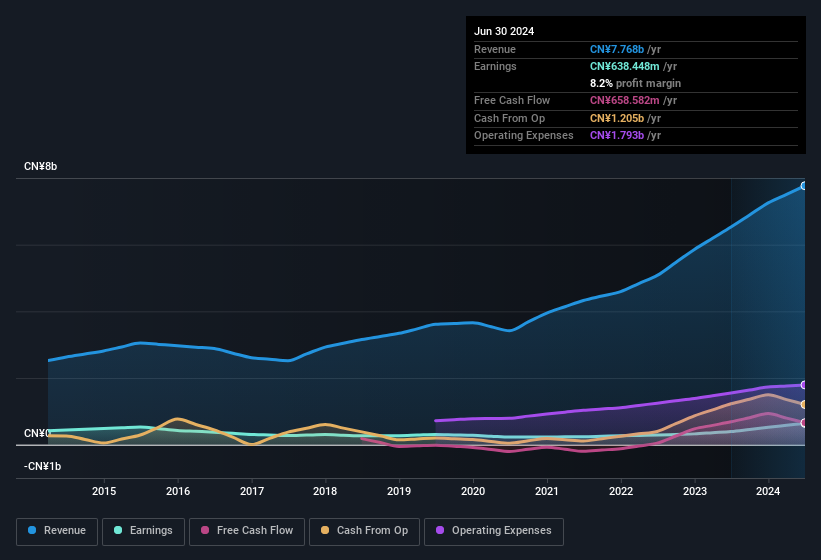

One way to double-check a company's growth is to look at how its revenue, and earnings before interest and tax (EBIT) margins are changing. While we note Wasion Holdings achieved similar EBIT margins to last year, revenue grew by a solid 19% to CN¥7.8b. That's progress.

The chart below shows how the company's bottom and top lines have progressed over time. To see the actual numbers, click on the chart.

The trick, as an investor, is to find companies that are going to perform well in the future, not just in the past. While crystal balls don't exist, you can check our visualization of consensus analyst forecasts for Wasion Holdings' future EPS 100% free.

Are Wasion Holdings Insiders Aligned With All Shareholders?

It's said that there's no smoke without fire. For investors, insider buying is often the smoke that indicates which stocks could set the market alight. This view is based on the possibility that stock purchases signal bullishness on behalf of the buyer. However, insiders are sometimes wrong, and we don't know the exact thinking behind their acquisitions.

The CN¥299k worth of shares that insiders sold during the last 12 months pales in comparison to the CN¥25m they spent on acquiring shares in the company. We find this encouraging because it suggests they are optimistic about Wasion Holdings'future. We also note that it was the Founder & Executive Chairman, Wei Ji, who made the biggest single acquisition, paying HK$5.1m for shares at about HK$5.08 each.

These recent buys aren't the only encouraging sign for shareholders, as a look at the shareholder registry for Wasion Holdings will reveal that insiders own a significant piece of the pie. To be exact, company insiders hold 55% of the company, so their decisions have a significant impact on their investments. This should be seen as a good thing, as it means insiders have a personal interest in delivering the best outcomes for shareholders. And their holding is extremely valuable at the current share price, totalling CN¥4.1b. That level of investment from insiders is nothing to sneeze at.

While insiders are apparently happy to hold and accumulate shares, that is just part of the big picture. The cherry on top is that the CEO, Chit Kat is paid comparatively modestly to CEOs at similar sized companies. The median total compensation for CEOs of companies similar in size to Wasion Holdings, with market caps between CN¥2.9b and CN¥12b, is around CN¥3.5m.

The Wasion Holdings CEO received total compensation of just CN¥1.6m in the year to December 2023. First impressions seem to indicate a compensation policy that is favourable to shareholders. CEO remuneration levels are not the most important metric for investors, but when the pay is modest, that does support enhanced alignment between the CEO and the ordinary shareholders. It can also be a sign of good governance, more generally.

Does Wasion Holdings Deserve A Spot On Your Watchlist?

Wasion Holdings' earnings per share growth have been climbing higher at an appreciable rate. Just as heartening; insiders both own and are buying more stock. This quick rundown suggests that the business may be of good quality, and also at an inflection point, so maybe Wasion Holdings deserves timely attention. It's still necessary to consider the ever-present spectre of investment risk. We've identified 1 warning sign with Wasion Holdings , and understanding it should be part of your investment process.

The good news is that Wasion Holdings is not the only stock with insider buying. Here's a list of small cap, undervalued companies in HK with insider buying in the last three months!

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

Valuation is complex, but we're here to simplify it.

Discover if Wasion Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

Most Discussed

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10