Should You Buy Tesla Stock Before April 2?

-

Tesla stock has plunged by 53% from its record high, which was set in December last year.

-

The company has an exciting product pipeline featuring self-driving cars and humanoid robots, but its electric vehicle (EV) business is in trouble.

-

Tesla's upcoming quarterly delivery numbers (expected on April 2) could disappoint investors, due to recent sales declines across the globe.

Shares of Tesla (TSLA -0.08%) soared to a record high of $479 at the end of 2024, shortly after President Trump won the election. Investors were optimistic about the possibility of friendlier regulations that could help Tesla fast-track its autonomous driving and robotics platforms. They could add trillions of dollars to the company's valuation, according to some Wall Street analysts and CEO Elon Musk.

But the stock has since plummeted 53% from its all-time high. The company still draws 79% of its revenue from passenger electric vehicles (EVs), and some reports during the early stages of 2025 suggest demand might be falling off a cliff.

Management usually reports its production and delivery numbers for the first quarter of the year (ended March 31) on April 2. Since its stock has already been cut in half over the last few months, could this be a buying opportunity ahead of the report on deliveries? Let's find out.

Tesla's sales appear to be plunging worldwide

Tesla delivered 1.78 million cars during 2024, which was a 1% drop compared to 2023. It was the first annual sales decline since the company launched its flagship Model S in 2011, and it put a big dent in Elon Musk's desire to grow production by 50% per year.

Unfortunately, 2025 is shaping up to be even worse because sales plummeted by 43% across Europe during January and February compared to the same months in 2024. That included a whopping 70% decline in Germany, 48% in Denmark, and 45% in Sweden and Portugal. Sales also fell by 33% in Australia during January, before the decline accelerated to 70% in February.

Reports suggest there could also be a decline in China during the first quarter of 2025. The country is one of Tesla's most important markets, regularly accounting for a third of its total sales.

The demand problem is multifaceted. Since sales of EVs overall continue to climb in most countries, it appears the company is simply bleeding market share to its competitors at a rapid pace.

China-based brands like BYD and Great Wall Motors already sell their base model EVs for under $15,000 in their domestic market, and they are quickly expanding globally. Tesla simply can't compete at that price point in any of the countries in which it operates.

Musk himself also appears to be creating some headwinds for the brand due to his involvement in both American and global politics. On Wednesday, the Associated Press reported on the growing instances of vandalism to Tesla dealerships and privately owned vehicles, not just in the U.S., but also overseas.

Whether you agree with Musk's politics or not, there is no doubt these events have many consumers thinking twice before buying one of the company's EVs.

Image source: Tesla.

Self-driving cars and robotics could be game changers for Tesla

Rather than trying to manufacture ultra-cheap EVs to compete with some of the Chinese brands I mentioned earlier, Musk is pivoting Tesla toward two new frontiers: autonomous driving and robotics.

Last October, it unveiled its Cybercab robotaxi, which will run entirely on its full self-driving (FSD) software. It is designed to haul passengers and even make commercial deliveries around the clock, creating lucrative new revenue streams for the company.

Supervised FSD has been available in Tesla's passenger EVs in beta mode for a few years, but Musk thinks unsupervised versions will receive the green light for public use in Texas and California this year.

Cathie Wood's ARK Investment Management thinks FSD and the Cybercab could propel Tesla to an $8 trillion valuation by 2029, thanks to the sizable opportunity in new industries like autonomous ride-hailing. The company's valuation is just $700 billion as of this writing, so ARK's forecast implies growth of more than 11 times.

But I think some of ARK's predictions are overly ambitious. For example, the firm believes FSD and the Cybercab will be generating $756 billion in annual revenue by 2029. Since Tesla only generated $97.6 billion in total revenue last year, it's unrealistic to expect two new products to scale up that quickly -- especially since they haven't launched yet, and we don't know how consumers will respond to them.

Musk actually thinks the Optimus humanoid robot represents an even bigger financial opportunity than autonomous driving. He believes humanoids could outnumber humans by 2040, meaning they could be in every household and factory in the world, assisting with the tasks most of us don't want to do. In a recent conference call with investors, Musk said Optimus could generate $10 trillion in revenue over the long term.

In fact, he thinks the robot will help set the stage for Tesla to become the most valuable company in the world one day.

Should you buy Tesla stock before April 2?

Before investors dive in to buy the stock based on forecasts from ARK and Musk himself, it's important to consider its valuation. Since the company slashed prices on most of its EVs to spur demand last year and still suffered a sales decline, its earnings per share (EPS) plummeted by 53% compared to 2023, coming in at $2.04.

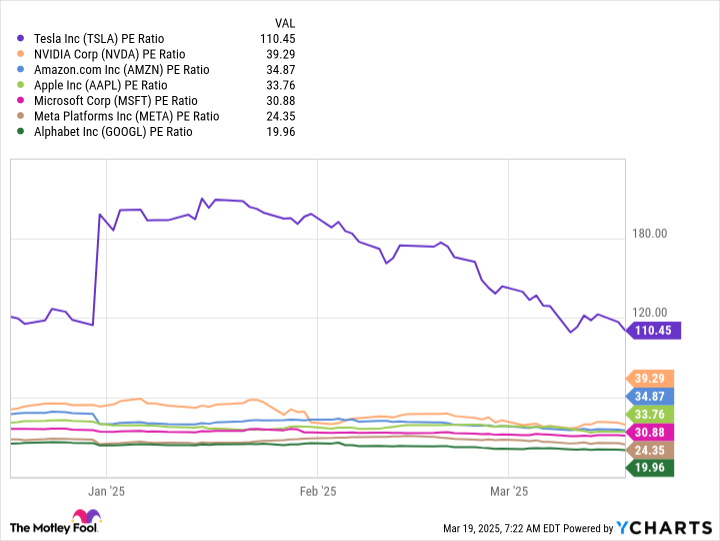

That places the stock at an eye-popping price-to-earnings ratio (P/E) of 110.4, making it the most expensive name among the "Magnificent Seven" tech giants by a large margin:

TSLA PE Ratio data by YCharts.

The Cybercab isn't expected to go into mass production until 2026, and it could take even longer for Optimus to scale up. In other words, Tesla's financial results will be driven by its passenger EV sales for at least the next year. Due to the sales declines I highlighted earlier, the company's EPS could erode further in 2025, which makes its stock appear even more expensive on a forward basis.

Simply put, the company's issues will take far longer than one quarter to solve, and its valuation doesn't afford it any room for error. As a result, I don't think the upcoming first-quarter production and deliveries report on April 2 will be a positive catalyst for the stock, so I would steer clear for now. If the Tesla does fail to generate growth this year, I think its stock could be headed for further downside of 50% or more.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

Most Discussed

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10