China Taiping Insurance Holdings' (HKG:966) Upcoming Dividend Will Be Larger Than Last Year's

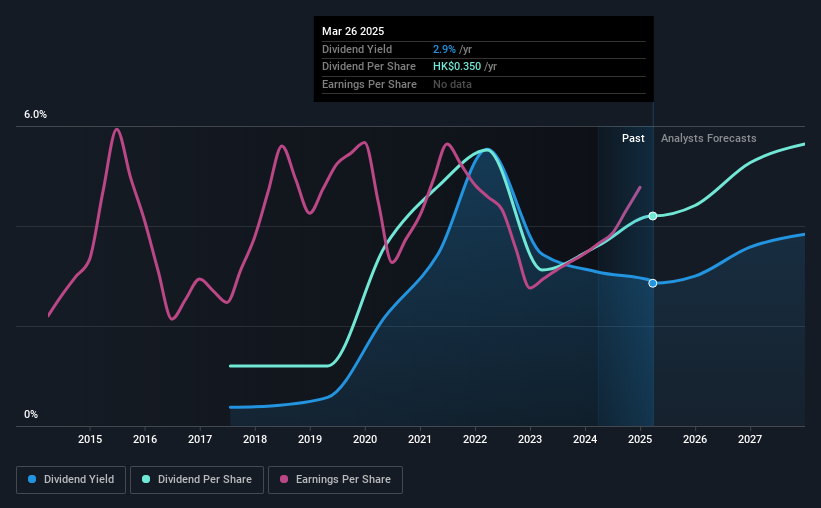

China Taiping Insurance Holdings Company Limited (HKG:966) will increase its dividend from last year's comparable payment on the 22nd of July to HK$0.35. Despite this raise, the dividend yield of 2.9% is only a modest boost to shareholder returns.

China Taiping Insurance Holdings' Projected Earnings Seem Likely To Cover Future Distributions

The dividend yield is a little bit low, but sustainability of the payments is also an important part of evaluating an income stock. However, prior to this announcement, China Taiping Insurance Holdings' dividend was comfortably covered by both cash flow and earnings. This means that most of its earnings are being retained to grow the business.

Looking forward, earnings per share is forecast to rise by 43.9% over the next year. If the dividend continues along recent trends, we estimate the payout ratio will be 14%, which is in the range that makes us comfortable with the sustainability of the dividend.

View our latest analysis for China Taiping Insurance Holdings

China Taiping Insurance Holdings' Dividend Has Lacked Consistency

Looking back, China Taiping Insurance Holdings' dividend hasn't been particularly consistent. Due to this, we are a little bit cautious about the dividend consistency over a full economic cycle. The annual payment during the last 8 years was HK$0.10 in 2017, and the most recent fiscal year payment was HK$0.35. This works out to be a compound annual growth rate (CAGR) of approximately 17% a year over that time. China Taiping Insurance Holdings has grown distributions at a rapid rate despite cutting the dividend at least once in the past. Companies that cut once often cut again, so we would be cautious about buying this stock solely for the dividend income.

The Dividend's Growth Prospects Are Limited

With a relatively unstable dividend, it's even more important to evaluate if earnings per share is growing, which could point to a growing dividend in the future. China Taiping Insurance Holdings has seen earnings per share falling at 3.4% per year over the last five years. If earnings continue declining, the company may have to make the difficult choice of reducing the dividend or even stopping it completely - the opposite of dividend growth. It's not all bad news though, as the earnings are predicted to rise over the next 12 months - we would just be a bit cautious until this can turn into a longer term trend.

Our Thoughts On China Taiping Insurance Holdings' Dividend

Overall, this is probably not a great income stock, even though the dividend is being raised at the moment. The payments haven't been particularly stable and we don't see huge growth potential, but with the dividend well covered by cash flows it could prove to be reliable over the short term. Overall, we don't think this company has the makings of a good income stock.

Investors generally tend to favour companies with a consistent, stable dividend policy as opposed to those operating an irregular one. Still, investors need to consider a host of other factors, apart from dividend payments, when analysing a company. Without at least some growth in earnings per share over time, the dividend will eventually come under pressure either from competition or inflation. Businesses can change though, and we think it would make sense to see what analysts are forecasting for the company. If you are a dividend investor, you might also want to look at our curated list of high yield dividend stocks.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)• Undervalued Small Caps with Insider Buying• High growth Tech and AI CompaniesOr build your own from over 50 metrics.

Explore Now for FreeHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

Most Discussed

No relevant data is available