Hello Group (NASDAQ:MOMO) Will Be Hoping To Turn Its Returns On Capital Around

Ignoring the stock price of a company, what are the underlying trends that tell us a business is past the growth phase? Typically, we'll see the trend of both return on capital employed (ROCE) declining and this usually coincides with a decreasing amount of capital employed. Ultimately this means that the company is earning less per dollar invested and on top of that, it's shrinking its base of capital employed. On that note, looking into Hello Group (NASDAQ:MOMO), we weren't too upbeat about how things were going.

This technology could replace computers: discover the 20 stocks are working to make quantum computing a reality.

Understanding Return On Capital Employed (ROCE)

Just to clarify if you're unsure, ROCE is a metric for evaluating how much pre-tax income (in percentage terms) a company earns on the capital invested in its business. The formula for this calculation on Hello Group is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.13 = CN¥1.5b ÷ (CN¥18b - CN¥6.4b) (Based on the trailing twelve months to December 2024).

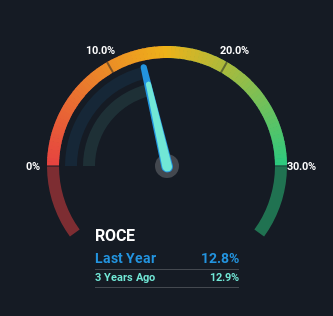

Therefore, Hello Group has an ROCE of 13%. In absolute terms, that's a satisfactory return, but compared to the Interactive Media and Services industry average of 7.4% it's much better.

View our latest analysis for Hello Group

Above you can see how the current ROCE for Hello Group compares to its prior returns on capital, but there's only so much you can tell from the past. If you'd like, you can check out the forecasts from the analysts covering Hello Group for free.

So How Is Hello Group's ROCE Trending?

We are a bit anxious about the trends of ROCE at Hello Group. To be more specific, today's ROCE was 18% five years ago but has since fallen to 13%. On top of that, the business is utilizing 40% less capital within its operations. The combination of lower ROCE and less capital employed can indicate that a business is likely to be facing some competitive headwinds or seeing an erosion to its moat. If these underlying trends continue, we wouldn't be too optimistic going forward.

On a side note, Hello Group's current liabilities have increased over the last five years to 35% of total assets, effectively distorting the ROCE to some degree. Without this increase, it's likely that ROCE would be even lower than 13%. Keep an eye on this ratio, because the business could encounter some new risks if this metric gets too high.

In Conclusion...

In summary, it's unfortunate that Hello Group is shrinking its capital base and also generating lower returns. Investors haven't taken kindly to these developments, since the stock has declined 61% from where it was five years ago. That being the case, unless the underlying trends revert to a more positive trajectory, we'd consider looking elsewhere.

Like most companies, Hello Group does come with some risks, and we've found 2 warning signs that you should be aware of.

While Hello Group may not currently earn the highest returns, we've compiled a list of companies that currently earn more than 25% return on equity. Check out this free list here.

If you're looking to trade Hello Group, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Hello Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

Most Discussed

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10