Is AleAnna (NASDAQ:ANNA) In A Good Position To Invest In Growth?

There's no doubt that money can be made by owning shares of unprofitable businesses. For example, biotech and mining exploration companies often lose money for years before finding success with a new treatment or mineral discovery. But while history lauds those rare successes, those that fail are often forgotten; who remembers Pets.com?

Given this risk, we thought we'd take a look at whether AleAnna (NASDAQ:ANNA) shareholders should be worried about its cash burn. For the purposes of this article, cash burn is the annual rate at which an unprofitable company spends cash to fund its growth; its negative free cash flow. Let's start with an examination of the business' cash, relative to its cash burn.

This technology could replace computers: discover the 20 stocks are working to make quantum computing a reality.

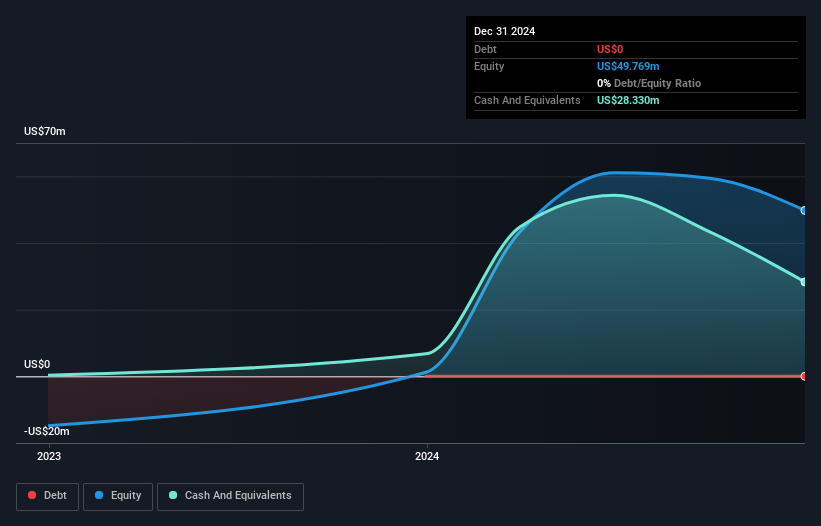

Does AleAnna Have A Long Cash Runway?

A company's cash runway is the amount of time it would take to burn through its cash reserves at its current cash burn rate. When AleAnna last reported its December 2024 balance sheet in March 2025, it had zero debt and cash worth US$28m. In the last year, its cash burn was US$40m. That means it had a cash runway of around 9 months as of December 2024. To be frank, this kind of short runway puts us on edge, as it indicates the company must reduce its cash burn significantly, or else raise cash imminently. Depicted below, you can see how its cash holdings have changed over time.

See our latest analysis for AleAnna

How Is AleAnna's Cash Burn Changing Over Time?

Whilst it's great to see that AleAnna has already begun generating revenue from operations, last year it only produced US$1.4m, so we don't think it is generating significant revenue, at this point. Therefore, for the purposes of this analysis we'll focus on how the cash burn is tracking. In fact, it ramped its spending strongly over the last year, increasing cash burn by 172%. That sort of spending growth rate can't continue for very long before it causes balance sheet weakness, generally speaking. Of course, we've only taken a quick look at the stock's growth metrics, here. This graph of historic earnings and revenue shows how AleAnna is building its business over time.

Can AleAnna Raise More Cash Easily?

Given its cash burn trajectory, AleAnna shareholders should already be thinking about how easy it might be for it to raise further cash in the future. Issuing new shares, or taking on debt, are the most common ways for a listed company to raise more money for its business. Commonly, a business will sell new shares in itself to raise cash and drive growth. By looking at a company's cash burn relative to its market capitalisation, we gain insight on how much shareholders would be diluted if the company needed to raise enough cash to cover another year's cash burn.

Since it has a market capitalisation of US$541m, AleAnna's US$40m in cash burn equates to about 7.4% of its market value. That's a low proportion, so we figure the company would be able to raise more cash to fund growth, with a little dilution, or even to simply borrow some money.

Is AleAnna's Cash Burn A Worry?

On this analysis of AleAnna's cash burn, we think its cash burn relative to its market cap was reassuring, while its increasing cash burn has us a bit worried. Summing up, we think the AleAnna's cash burn is a risk, based on the factors we mentioned in this article. On another note, AleAnna has 3 warning signs (and 2 which are a bit concerning) we think you should know about.

Of course, you might find a fantastic investment by looking elsewhere. So take a peek at this free list of interesting companies, and this list of stocks growth stocks (according to analyst forecasts)

If you're looking to trade AleAnna, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency• Be alerted to new Warning Signs or Risks via email or mobile• Track the Fair Value of your stocks

Try a Demo Portfolio for FreeHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

Most Discussed

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10