Here's Why We Think Shift4 Payments (NYSE:FOUR) Might Deserve Your Attention Today

Investors are often guided by the idea of discovering 'the next big thing', even if that means buying 'story stocks' without any revenue, let alone profit. Unfortunately, these high risk investments often have little probability of ever paying off, and many investors pay a price to learn their lesson. Loss-making companies are always racing against time to reach financial sustainability, so investors in these companies may be taking on more risk than they should.

Despite being in the age of tech-stock blue-sky investing, many investors still adopt a more traditional strategy; buying shares in profitable companies like Shift4 Payments (NYSE:FOUR). Now this is not to say that the company presents the best investment opportunity around, but profitability is a key component to success in business.

AI is about to change healthcare. These 20 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10bn in marketcap - there is still time to get in early.

Shift4 Payments' Improving Profits

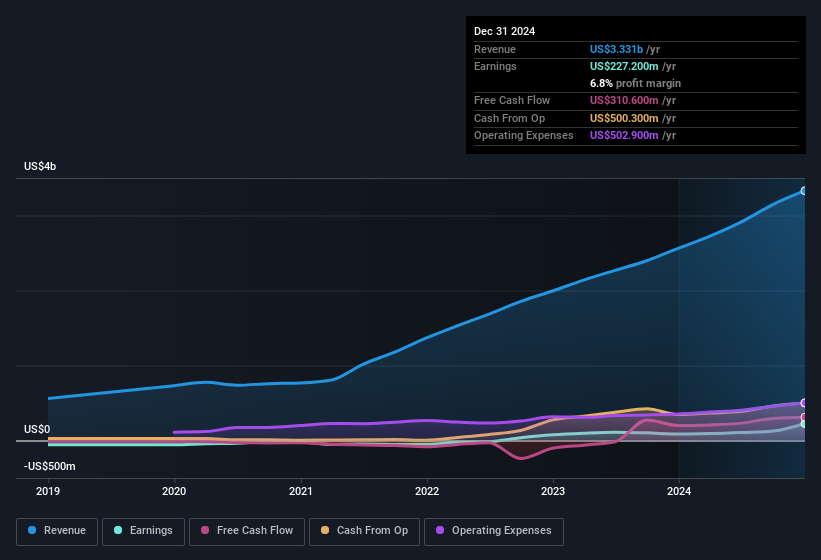

Shift4 Payments has undergone a massive growth in earnings per share over the last three years. So much so that this three year growth rate wouldn't be a fair assessment of the company's future. As a result, we'll zoom in on growth over the last year, instead. In impressive fashion, Shift4 Payments' EPS grew from US$1.44 to US$3.28, over the previous 12 months. It's a rarity to see 127% year-on-year growth like that. The best case scenario? That the business has hit a true inflection point.

Top-line growth is a great indicator that growth is sustainable, and combined with a high earnings before interest and taxation (EBIT) margin, it's a great way for a company to maintain a competitive advantage in the market. EBIT margins for Shift4 Payments remained fairly unchanged over the last year, however the company should be pleased to report its revenue growth for the period of 30% to US$3.3b. That's a real positive.

The chart below shows how the company's bottom and top lines have progressed over time. Click on the chart to see the exact numbers.

Check out our latest analysis for Shift4 Payments

Fortunately, we've got access to analyst forecasts of Shift4 Payments' future profits. You can do your own forecasts without looking, or you can take a peek at what the professionals are predicting .

Are Shift4 Payments Insiders Aligned With All Shareholders?

Investors are always searching for a vote of confidence in the companies they hold and insider buying is one of the key indicators for optimism on the market. That's because insider buying often indicates that those closest to the company have confidence that the share price will perform well. Of course, we can never be sure what insiders are thinking, we can only judge their actions.

While there was some insider selling, that pales in comparison to the US$11m that the Founder, Jared Isaacman spent acquiring shares. The average price paid was about US$66.96. It's not often you see purchases like this and so it should be on the radar of everyone who follows Shift4 Payments.

On top of the insider buying, it's good to see that Shift4 Payments insiders have a valuable investment in the business. Notably, they have an enviable stake in the company, worth US$198m. This suggests that leadership will be very mindful of shareholders' interests when making decisions!

Does Shift4 Payments Deserve A Spot On Your Watchlist?

Shift4 Payments' earnings per share have been soaring, with growth rates sky high. The icing on the cake is that insiders own a large chunk of the company and one has even been buying more shares. This quick rundown suggests that the business may be of good quality, and also at an inflection point, so maybe Shift4 Payments deserves timely attention. What about risks? Every company has them, and we've spotted 2 warning signs for Shift4 Payments (of which 1 is a bit unpleasant!) you should know about.

There are plenty of other companies that have insiders buying up shares. So if you like the sound of Shift4 Payments, you'll probably love this curated collection of companies in the US that have an attractive valuation alongside insider buying in the last three months.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency• Be alerted to new Warning Signs or Risks via email or mobile• Track the Fair Value of your stocks

Try a Demo Portfolio for FreeHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

Most Discussed

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10