Estee Lauder returned $10 billion in cash to shareholders between 2013 and 2022 via share buybacks.

Investment Thesis

As consumers of beauty products upgrade for supposedly higher-quality ingredients, efficacy, and services, Estee Lauder, a leading supplier of high-end beauty products, is anticipated to profit from premiumization trends. Thanks to well-known brands like La Mer and Estee Lauder, the company has a strong presence in Europe and Asia, where skin care accounts for 50% of premium beauty spending. Only half of Estee's 20+ brands are available in major emerging markets like China, India, and Brazil, demonstrating the company's effective brand expansion strategy. In order to preserve its brand prominence and guarantee easy accessibility for beauty users, the company is anticipated to make investments in digital channels.But there are dangers ahead, like the premium pure-play's increased susceptibility to macro-cyclicality in comparison to its rival L'Oreal. Estee might need some time to update its line of cosmetics, which could leave the company open to losing market share to competitors like LVMH and L'Oreal. The firm and the Lauder family are expected to manage these changes and position the company for long-term growth, but investor anxiety over the unknowns surrounding new management and expanded restructuring is also anticipated.

- Warning! GuruFocus has detected 5 Warning Signs with EL.

Notable Guru Holdings

Investment Upside

The premiumization trend, which is anticipated to continue for some time, is consistent with Estee's premium-only brand positioning. Estee is over-indexed in China, so the weakness was mostly limited there even though sales fell 10% and 2% in fiscal 2023 and 2024. 93% of Estee's recent sales declines were attributable to the nation. Nevertheless, Estee only lost 10 basis points and 80 basis points of market share between 2021 and 2023, maintaining its prestige in China's high teens skin care and makeup market. The new management team is eager to use its portfolio of powerful brands to expand its exposure in emerging Asia outside of China. The company should be able to respond to local consumption upgrade preferences more quickly thanks to its recently opened manufacturing and distribution facilities in Japan. With an emphasis on skin science research and cross-channel integrated marketing, Estee is retaining its position in North America and Western Europe. Because brand differentiation is predicated on perceived efficacy in important areas like brightening and anti-aging, the pricing environment in the beauty industry, particularly in skin care, has remained favorable. The enduring bond between consumers and their preferred beauty brands is further exacerbated by risk aversion to new brands due to concerns about skin irritations. Private-label penetration is almost nonexistent in the premium market and only in the low single digits for mass beauty. Customers are willing to pay more for Estee's prestige products because of their perceived quality attributes and social currencies, as evidenced by the company's high gross margins, which have averaged 74% over the last five years. By fiscal 2027, gross margins should return to the mid-70s level as macro headwinds subside and demand improves.

Estee's competitive position in both digital and physical channels has been reinforced by its flexible channel strategies. By using in-store promotions, retailer-only product releases, gifts with purchase, and advertising campaigns to increase store traffic and customer purchases, the company has made a name for itself as a major partner for high-end retailers in the beauty sector. Even though the channel mix is rapidly shifting to digital, Estee thinks that physical relationships are still crucial for in-person beauty product discovery and testing. To increase productivity and lessen exposure to structural declines in underperforming department chains, Estee has trimmed department store counters and freestanding retail doors. In order to maintain its prestige brand positioning, it has also made greater investments in cultivating closer ties with renowned luxury department stores in North America, Europe, and Asia. Estee's cooperation with specialty multibrand retailers in the fields of merchandising and data analytics should be strengthened by the recent hiring of a senior executive with substantial experience at Ulta and Sephora to lead its US operation. Estee's broad economic moat rating is also supported by its competitive cost structure. Due to its substantial scale ($15 billion in sales, second only to L'Oreal), the company enjoys substantial advantages in manufacturing, distribution, and procurement. With an annual budget of $4 billion, Estee ranks among the top 30 advertisers of consumer goods worldwide, giving the company significant negotiating leverage over its smaller competitors.

Intrinsic Valuation

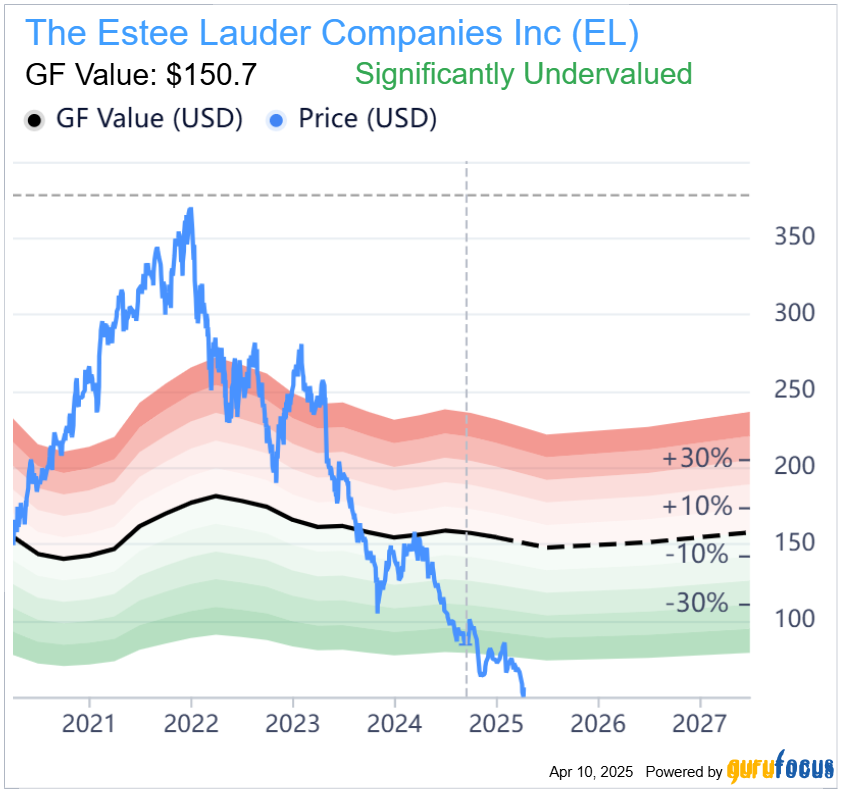

Because of the expected protracted problems in China, increased investments, and a more extensive restructuring that might postpone the recovery of the company's top line and operating margins, Estee Lauder's true intrinsic value is estimated to be $150.7. An enterprise value/adjusted EBITDA multiple of 32 times is now implied by the updated intrinsic valuation for fiscal 2026. Despite $4.0 billion in sales and $0.62 adjusted EPS for the second quarter, the company's core skincare segment saw a 12% drop in sales and a 320-basis-point contraction in operating margins to 15.9%. Adjusted EPS guidance from the new management ranged from 69% to 79% on a decline in organic sales of 8% to 10%. The company projects a 4% yearly growth in sales over the next ten years, with its core skincare segment accounting for 50% of total sales. Estee's ability to resume strong performance once demand in China stabilizes and stable global beauty sales are anticipated to be the main drivers of this growth. It is anticipated that annual sales growth for makeup and fragrances will be 3% and 6%, respectively.In terms of profitability, the company anticipates that the gross margin line will be the primary driver of operating margin growth, which will reach 15.9% at the end of the 10-year forecast period. Improvements in manufacturing efficiency, supply chain cost reductions, and a better channel mix are expected to boost the profitability metric to 75.4% by 2034. The company is also anticipated to increase its research expenditures in order to strengthen its competitive position and produce innovation that consumers value. By 2034, it is anticipated that advertising expenditures will increase to 25.7% of total sales.

Investment Downside

Global beauty product manufacturer Estee may encounter difficulties as a result of China's macroeconomic headwinds and a lack of transparency regarding restructuring. With centralized manufacturing in the US, Europe, and Japan, the company distributes its goods in more than 150 countries and depends on reliable trade regulations and international supply chains to ensure prompt and economical delivery. Its financial performance could be hampered by any significant reversal of open trade policies and transportation disruptions. The beauty industry has been upended by the rise of digital marketing and online marketplaces, which have reduced entry barriers and sped up the commercialization of novel ideas, especially in makeup. To support customer activation and retention across channels, Estee has made investments in technology, content, and distribution infrastructure. However, because social media and mobile phones are so common, the company's well-known premium brands are continuously being scrutinized. Any consumer experience, sustainability, social, or brand messaging practices that are thought to be at odds with the company's positioning could be highlighted, which could harm the brand and have an effect on pricing power and volume demand.

Portfolio Management

The luxury cosmetics company Estee Lauder has encountered difficulties in recent makeup acquisitions, such as the $1.5 billion acquisition of Too Faced in 2017 and smaller agreements with BECCA and Smashbox. Although the goal of these acquisitions was to increase Estee's market share at Sephora and Ulta, the company had to incur $2 billion in impairment charges between 2019 and 2021 as a result of lower-than-expected performance and a less optimistic outlook for these brands. The underperformance can be partially attributed to structural issues in makeup, which were made worse by the pandemic. These issues include lower entry barriers and increased fashion risks. Similar charges were also disclosed by L'Oreal in relation to its own makeup acquisitions.Estee completed its biggest transaction to date in April 2023 when it paid $2.3 billion to acquire the high-end fashion and cosmetics company Tom Ford. Because of its well-established distribution and strong brand equity in high-end makeup and fragrance, Tom Ford has achieved high double-digit sales growth every year for the past ten years. Although Estee has been increasing dividends consistently over the last ten years, declining operating performance is anticipated to result in a 47% reduction in quarterly dividends in October 2024.

This article first appeared on GuruFocus.Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

Most Discussed

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10