TFLO: Major Oil Roadblock To Inflation May Be Overcome

Wipada Wipawin

The iShares Treasury Floating Rate Bond ETF (NYSEARCA:TFLO) could be headed for lower yields and weaker performance as a key factor make rate cuts more likely. Things have changed since our last coverage. There is less inflation pressure on global commodities due to China's slowdown. This is being seen in oil. On the flip side, expectations are still too high for inflation, and the employment data which, we believe, is critical is not particularly supportive to inflation declines. Nonetheless, things are clearly moving in the correct direction in terms of inflation even if it's taking too long.

TFLO Breakdown

TFLO is a low expense ratio ETF at 0.15%. It has the same expense ratio as iShares Floating Rate Bond ETF (FLOT) which accomplishes much of the same as TFLO. The difference is that TFLO has absolutely no credit risk, and follows the spot prevailing rates, essentially whatever the Fed funds rate is. The effective duration is of course negligible by design, and there is really no capital gains consideration for this ETF, it's all about what you're getting in run-rate interest. The question is therefore where will rates go.

They won't go higher, but they could persist for longer than expected at current levels. Jobs data was mixed. Unemployment rate has fallen a bit, which by Phillips Curve logic is inflationary or at least supports current rates. Hiring did slow, but there isn't the shock needed to slow down the wheel of inflation. Inflation expectations are still above policy bands. Expectations tend to be the best reflection of rates will actually go because they are also causative of inflation. Also, some key elements of inflation remain strong like rent, which dominates consumer consciousness.

On the other hand, there are quite a lot of oil price declines lately, almost 10% last week. The reason is demand. China industrial demand is weaker than expected and there hasn't been a promising recovery in those markets. US ISM data was also showing some deceleration in US producer fixed and working capital investment. Despite OPEC+ pushing back supply cut phaseouts till December instead of October, prices are not rallying. Maintenance season coming up now in US refineries could also keep demand low and help re-anchor expectations for the public about oil prices. This may be the clinching factor that will give space for the Fed to push down rates after all.

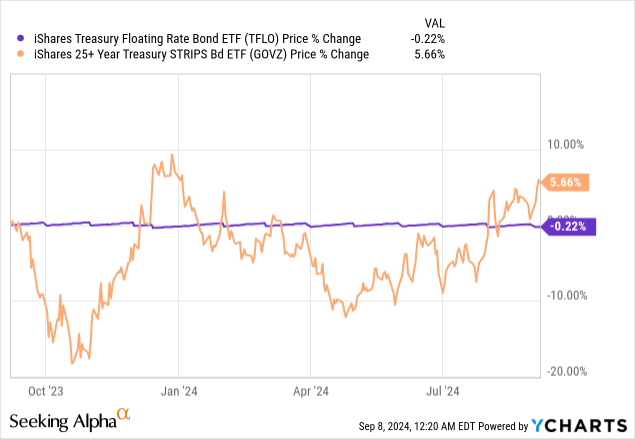

Bottom Line

Comparing TFLO price performance with an ETF with significant duration we can see that duration bets have picked up considerably since the beginning of July. The performance of duration bets from July signals about an expectation of 1% more cuts than previously expected. We believe that means that a lot of the upside from duration is currently priced in, as we still see roadblocks to inflation and a 1% cut would be quite dramatic. However, the decline in oil, particularly if prices persist at these lower levels, make some cut rather likely at this point. The high oil prices until now were a significant barrier to rate cuts. We think TFLO is still a fine approach to fixed income at this point, but some amount of duration exposure probably is beginning to make some sense.

免责声明:投资有风险,本文并非投资建议,以上内容不应被视为任何金融产品的购买或出售要约、建议或邀请,作者或其他用户的任何相关讨论、评论或帖子也不应被视为此类内容。本文仅供一般参考,不考虑您的个人投资目标、财务状况或需求。TTM对信息的准确性和完整性不承担任何责任或保证,投资者应自行研究并在投资前寻求专业建议。

热议股票

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10