TLTW: Covered Call ETF Focusing On Long-Term Treasuries, Strong 14.9% Yield, Risks Abound

agshotime

I've covered the iShares 20+ Year Treasury Bond Buywrite Strategy ETF (BATS:TLTW) several times in the past. I've been bearish, as the fund's above-average duration was excessively risky during a period of rising rates and had led to underperformance in the past. With interest rates finally stabilizing, thought to have another look at the fund.

TLTW invests in long-term treasuries and sells covered calls on its holdings. This results in a massive 14.9% distribution yield, moderate upside potential, significant downside potential, and consistent capital losses and distribution cuts. Although the fund's risks and downsides are massive, I believe it should outperform during a period of slightly declining long-term interest rates. I rate the fund a buy, but this is something of a macro call, so lots of investors might disagree.

TLTW - Quick Overview

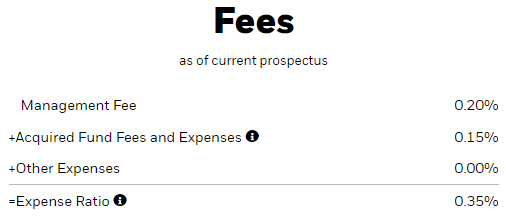

TLTW invests in long-term treasuries, through an investment in the iShares 20+ Year Treasury Bond ETF (TLT). Expenses equal 0.35%, a reasonable figure for a bond ETF, although there are definitely cheaper choices.

TLTW

TLTW sells one-month covered calls on the entirety of its holdings. These are 2.0% out of the money when written. TLTW receives significant cash, through option premiums, from this strategy. Said cash is entirely distributed to shareholders.

TLTW's covered call strategy is effectively equivalent to selling most potential capital gains for increased distributions. In the short-term, TLTW should outperform when bond prices are rising / interest rate are decreasing, and vice versa. The same is arguably true in the long-term as well, but the frequency and magnitude of gains and losses matter too, as do option prices.

TLTW's broad strategy seems clear enough. Let's have a look at some of the fund's positives and negatives, starting with the positives.

TLTW - Positives

Strong 14.9% Distribution Yield

TLTW's treasury investments and covered call strategy both generate significant income, resulting in a 14.9% distribution yield for the fund. It is an incredibly strong yield on an absolute basis, and much higher than that of most bonds and bond sub-asset classes.

TLTW's distribution yield is 11.3% higher than that of TLT, so it seems that the fund's treasuries generate around 3.6% in income, its covered call strategy the other 11.3%.

TLTW's distributions are almost certainly covered by underlying generation of income / option premiums, although it is impossible for me to be certain. Still, ETFs tend to distribute any and all income to shareholders and nothing else, so yields do tend to reflect underlying income, in the long-term at least.

Potential Outperformance

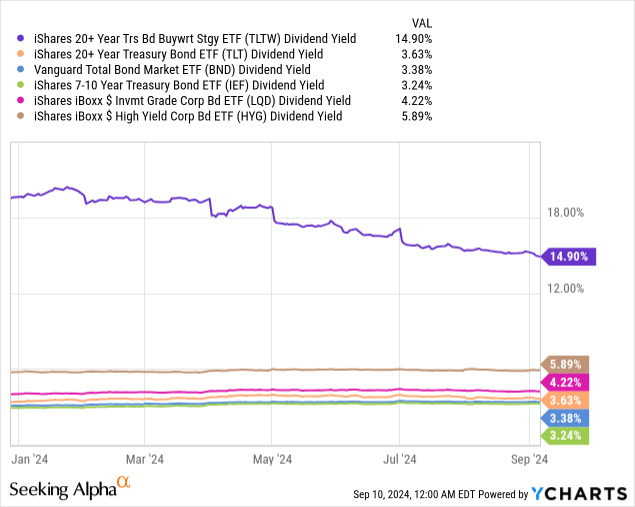

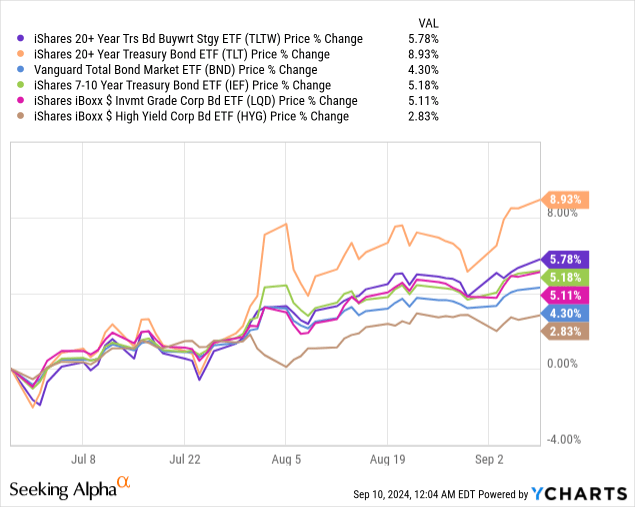

TLTW's strong distributions directly increase shareholder returns and should lead to outperformance during certain scenarios. Specifically, the distributions are of particular importance when interest rates and bond prices are flat. As an example, TLTW has outperformed TLT YTD:

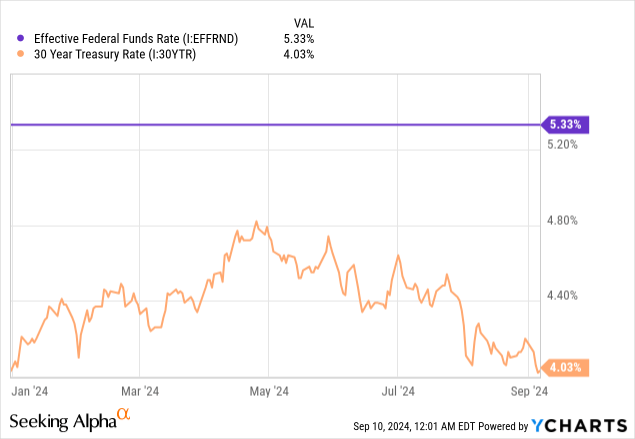

During which both Fed rates and 30y treasury rates, of particular importance for long-term treasury ETFs, are flat:

Best-case scenario for the fund is one in which interest rates drift downwards at a slow, but steady pace. TLTW should see double-digit distributions, moderate capital gains, and significant outperformance when this occurs. TLTW should continue to outperform when interest rates are flat, or drifting upwards slowly, although absolute returns should be lower. As the fund focuses on long-term treasuries, it is long-term treasury rates that matter. These are influenced by Fed rates but are not equivalent to these, nor do they necessarily move in the same direction.

Notwithstanding the above, interest rate volatility and timing both play an important role in the fund's performance and could cause performance to materially differ from the above. Covered call funds are sometimes a bit finicky, and that includes TLTW.

With the above in mind, let's have a look at TLTW's negatives.

TLTW - Negatives and Risks

High Interest Rate Risk

TLTW focuses on long-term treasuries, with an average duration of 16.7 years. It is an incredibly high duration on an absolute basis, and higher than that of most bonds and bond sub-asset classes.

Fund Filings - Table by Author

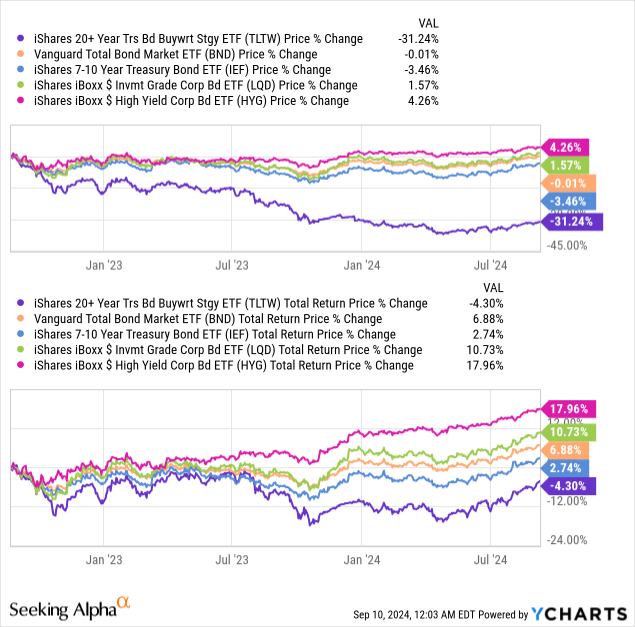

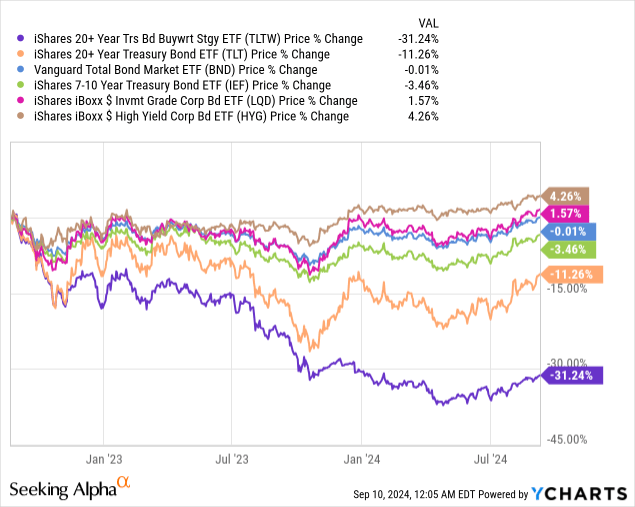

TLTW's duration should lead to significant, above-average capital losses and underperformance when interest rates increase, as has been the case since the fund's inception in late 2022. TLTW's share price is down a whopping 31.2% since inception, with most bond ETF share prices flat since the same. Losses would have been much higher if the fund had been created before the Fed started to hike, instead of in the middle of its hiking cycle.

TLTW's high interest rate risk increases risk, volatility, and losses when interest rates rise, all straightforward negatives for the fund and its shareholders.

Funds with high duration tend to see significant capital gains when interest rates decrease, but this isn't quite true for TLTW. As mentioned previously, the fund's covered call strategy caps its capital gains, which generally means any capital gains are moderate instead of high. As an example, the fund's share price is up 5.8% since July, compared to 8.9% for long-term treasuries, 5.2% for treasuries overall. Capital gains are definitely good, but lower than those of TLT.

Long-Term Capital Losses

TLTW's interest rate risk sometimes leads to significant capital losses, while its covered call strategy somewhat limits any capital gains. This should almost certainly result in long-term capital losses, as has been the case since inception.

As can be seen above, TLTW's share price is down 31.2% since inception. Around 11.3% of these losses were due to the fund's interest rate risk, as evidenced by TLT's losses. Around 19.9%, the remainder, was due to its covered call strategy limiting gains.

TLTW should almost certainly see long-term capital losses, and these are effectively irrecoverable. This is because the fund's capital gains are capped, and because capital losses erode the fund's asset base, making any potential recovery more difficult.

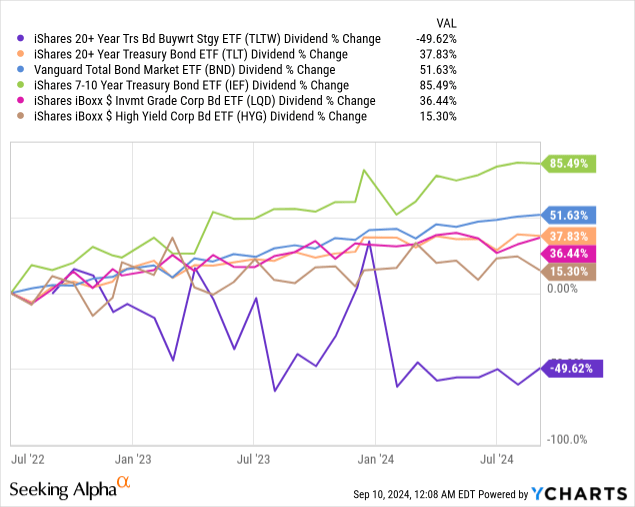

Declining Distributions

TLTW's distributions are dependent on many factors, including assets or assets per share. More assets mean more options can be written, which means more option income and higher distributions. For ETFs, assets per share are equivalent to share prices, so distributions are somewhat dependent on share prices themselves, among other factors.

As TLTW's share price should decline long-term, its distributions should too, as has been the case since the fund's inception. Unlike TLTW, almost all bond ETFs have seen significant dividend growth these past few years, due to Fed hikes.

TLTW's distributions are also dependent on option prices, which are, in turn, dependent on bond volatility. As interest rates have stabilized option prices have decreased, (partly) leading to the declining distributions seen above. Long-term, share prices are fundamental, but option prices and volatility could have an outsized short-term effect.

TLTW - Macro Conditions

TLTW's interest rate risk, consistent capital losses and distribution cuts, are all significant negatives for the fund, and were deal-breakers for me in the past. Improved macroeconomic conditions have turned me a bit bullish, though.

As conditions and rates stabilize, the fund's duration is less of a risk. Investing in a fund with a duration of 16.7 years was excessively risky when inflation was sky-high and the Fed was hiking rates, but is less of a concern right now. Do note that this means that option prices, and hence distributions, are lower, but I do think that the reduced risk is of greater importance.

At the same time, the odds of significant increases to interest rates seem extremely low. The Fed has guided for several cuts in the coming months, and I don't really see any catalysts or evidence for these turning into hikes. Market interest rates seem reasonable enough, so I don't expect these to increase a lot either. The situation was much different when inflation was higher, and when the market was pricing-in significant, imminent cuts.

Overall, I expect the Fed to cut rates in the coming months and years, and for bond prices to remain broadly stable, cuts being priced-in already. Under these conditions, TLTW should outperform, so I rate the fund a buy. I somewhat dislike this call, as I do have misgivings about the fund's strategy and long-term performance. Still, the situation does call for a buy rating.

Do consider the fund's negatives before investing. Investors should strongly consider re-investing a significant portion of the fund's distribution somewhere, income and asset levels would decline otherwise, and fast.

In general, very dovish investors might prefer TLT or similar funds, as these should outperform if the Fed were to cut rates significantly. I don't personally think the expected set of rate cuts qualifies. At the same time, more hawkish investors might prefer short-term or variable rate ETFs, as these should outperform if the Fed were to hike rates, even cut by less than expected. Significant interest rate volatility might cause significant, permanent capital losses for the fund, those expecting that might wish to avoid TLTW as well.

Conclusion

TLTW's covered call strategy should outperform during a period of bond price stability, which, I believe, is likely. I rate the fund a buy, but this is something of a macro call, so lots of investors might disagree.

免责声明:投资有风险,本文并非投资建议,以上内容不应被视为任何金融产品的购买或出售要约、建议或邀请,作者或其他用户的任何相关讨论、评论或帖子也不应被视为此类内容。本文仅供一般参考,不考虑您的个人投资目标、财务状况或需求。TTM对信息的准确性和完整性不承担任何责任或保证,投资者应自行研究并在投资前寻求专业建议。

热议股票

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10