VNQ: Active Approach Prevails, But Passive Investors May Benefit

everythingpossible/iStock via Getty Images

Vanguard Real Estate Index Fund ETF Shares (NYSEARCA:VNQ) is an answer for investors seeking exposition to the broad real estate market without spending time for detailed analysis of various market segments or representatives. It's understandable why investors are leaning towards such a solution, as it's time-saving and can still provide attractive income and total return.

Investment Thesis

As an investor heavily focused on the REIT sector, I prefer to cherry-pick my investments. I have long-standing experience in the area and a background in finance, and I find it relatively easy to compare metrics across different REITs. Therefore, I prefer to stick with my approach and have never had a position in VNQ.

However, as I recognise that not everyone is willing to put in the time to analyse such things, I believe that VNQ is a valid option to build passive and reliable exposure to the real estate market. This ETF features:

- Maybe modest (by the standards of some real estate sectors), but still attractive dividend yield of 3.6%

- Diversification across various property sectors

- A reasonable 0.13% expense ratio

- Positive market dynamic accompanying further appreciation

While VNQ can be considered a 'buy' for passive investors willing to have exposure to the real estate market, which will likely be supported by noticeable tailwinds in the upcoming years, I will put that on 'hold', as I believe that REIT sector offers relatively easy cherry-picking processes. By the end of this article, I'll provide a few examples of why I believe cherry-picking within the REIT sector is a more attractive approach for me and maybe potentially for you.

Frankly, if you are completely uninterested in taking a more active approach to the real estate market, feel free to stick to VNQ and continue to accumulate, as this ETF has a solid value proposition. However, if you are willing to give it a go with cherry-picking, more power to you - let me invite you to put VNQ on 'hold' and allocate elsewhere.

Let's Unwrap VNQ

Vanguard.com

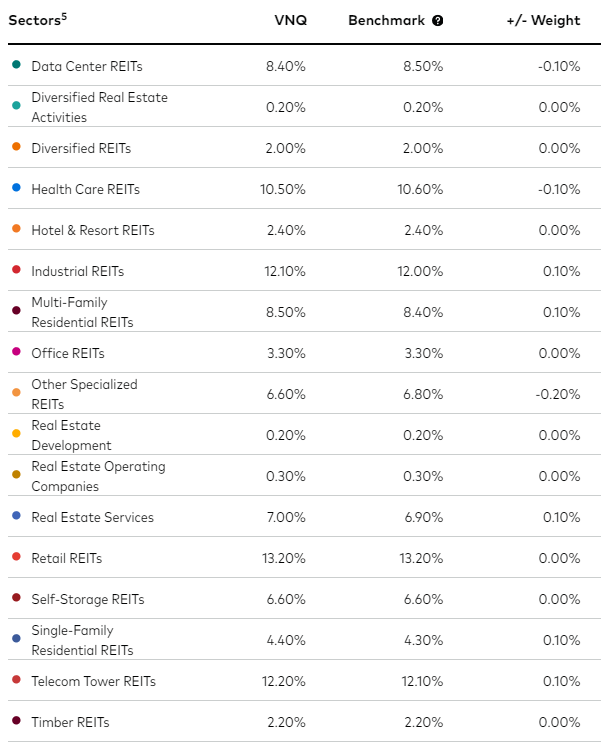

Four property sectors hold a double-digit share in the VNQ's composition:

- Retail REITs with a 13.2% share

- Telecom Tower REITs with a 12.2% share

- Industrial REITs with a 12.1% share

- Health Care REITs with a 10.5% share

The ETF also gives exposition to data centre REITs, residential REITs, self-storage, etc.

As a result of the VNQ purchase and its composition, investors gain exposure to 155 REITs, with (naturally) some dominating over others. VNQ's Top-10 holdings consist of (excl. Vanguard Real Estate II Index Fund Institutional):

- Prologis (PLD)

- American Tower (AMT)

- Equinix (EQIX)

- Welltower (WELL)

- Simon Property Group (SPG)

- $Public Storage(PSA-N)$ (PSA)

- Realty Income (O)

- Digital Realty Trust (DLR)

- Crown Castle (CCI)

- Extra Space Storage (EXR)

The abovementioned holdings stand for a 37.9% share of VNQ, excluding the impact of Vanguard Real Estate II Index Fund Institutional, which further increases their respective share.

There's no denying that each entity mentioned above is a top-quality pick in its respective field; however, I don't like the prominent exposure to data centre REITs or the fact that one of the best sectors to currently invest in the broad REIT sector—the industrial property segment—remains so heavily represented by just one holding (6.7% without factoring in the institutional ETF out of 12.1% represented by just one holding).

Tailwinds supporting VNQ

Different factors and market dynamics accompany various property sectors. For instance, the industrial property sector has been facing oversupply issues since mid-2022, net lease REITs heavily relying on acquisitions battle lower transactional market activity, and AI-driven tailwinds accompany data centre REITs.

However, one specific factor heavily impacts the broad REIT sector regardless of the specific property segment: the interest rate environment.

The rising interest rate environment since around the beginning of 2022 constituted a major headwind for the REIT sector for a few reasons:

- Firstly, it increased the cost of debt through higher floating-rated debt costs and higher costs upon refinancing. When REITs wanted to refinance their previous debt (pay down debt using new debt), they typically paid down lower-cost debt with higher-cost debt due to the higher interest rate environment.

- Secondly, it lowered the transactional market activity. Under the high-interest rate environment, the valuation gap between buyers' and sellers' expectations is relatively wide, leading to worse deal-sourcing capabilities and a lower potential of securing attractive investments. That's a crucial factor for REITs as their growth is determined mainly by their investment activities.

- Thirdly, with many investors leaving REITs for 'safer' instruments (e.g., tbonds) and lowered growth potential through limited investment activities, most REITs' valuations decreased noticeably. As a result, their costs of equity increased, magnifying the issues listed before.

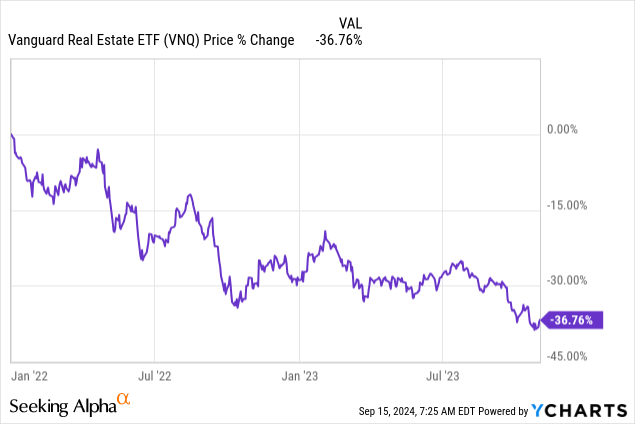

As a result, VNQ recorded a 36.8% price decrease in the 2022 - 2023. However, that has changed with VNQ's performance YTD, and I believe this reversed tendency will persist in the upcoming couple of years.

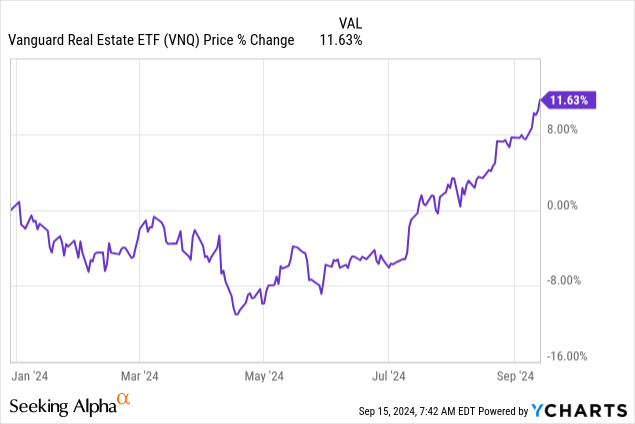

In 2024 YTD, VNQ delivered an 11.6% price increase, but still has a lot to catch up before matching its levels recorded pre-interest rate hikes. What facilitates and will continue to facilitate that turn-around?

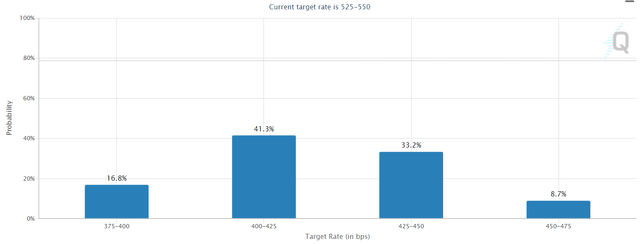

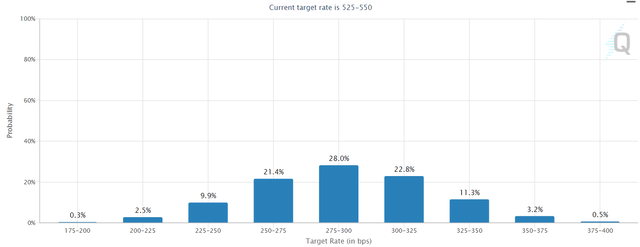

According to CME Group's FedWatch tool, the Fed is likely to loosen its monetary policy, and the market expects interest rates to go down significantly by the end of 2024 and within the upcoming 12 months.

CME Group - December 2024 CME Group - July 2025

The potential turnaround will facilitate the transactional market, which has already witnessed some positive shifts. For example, the retail property sector - Agree Realty (ADC) and Essential Properties Realty Trust (EPRT) realized higher investment volumes during Q2 2024 than in Q1 2024. Moreover, ADC updated its 2024 investment volume guidance upwards. These developments suggest that the gap between buyers and sellers has already narrowed. REITs are returning to investors' grace, improving their equity and overall cost of capital, leading to higher capabilities of securing positive investment spreads.

Monetary easing will further facilitate the development of leading REITs and, thus, VNQ.

Valuation Outlook and Risk Factors

Each stock market investment is accompanied by market and instrument-specific risk factors, which in the case of VNQ may include:

- uncertainty regarding the interest rate environment

- limited ability to adjust portfolio according to specific market trends accompanying various property sectors if one relies solely on VNQ

- the index relies heavily on a relatively small group of entities, leaving out smaller market players, which often offer better risk-to-reward ratios and stronger performance (e.g. EPR Properties (EPR), Rexford Industrial (REXR), First Industrial Realty (FR), Agree Realty, etc.)

- income-oriented investors may construct a higher-yielding portfolio with a similar margin of safety by cherry-picking investments

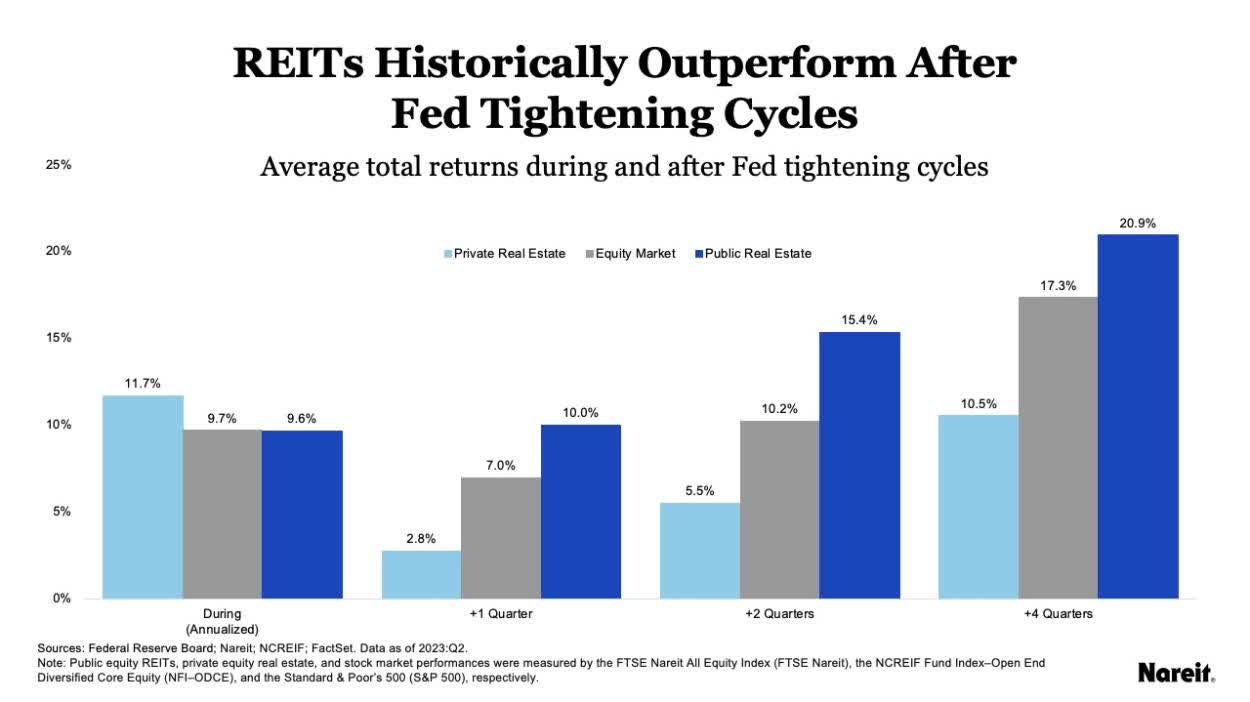

Nevertheless, I expect VNQ's price to increase in the upcoming quarters/years thanks to the major turnaround regarding the interest rate environment, which supports each and every one of the fund's holdings. While the upside potential has already been noticeably realised, there's still some meat on the bone to reach double-digit total return. Especially given the fact that REITs tend to outperform after FED tightening cycles:

reit.com

Additional Takeaway: Consider Cherry-picking

Due to increased volatility and some macroeconomic headwinds, the last couple of years have presented numerous opportunities in the REIT market. Even though I started my journey on Seeking Alpha in May 2024, I've already been able to present many well-performing opportunities.

Most of them are heavily underrepresented in VNQ, so I'll focus on them. Naturally, take this with a grain of salt, and if that's not your piece of bread, feel free to stick to VNQ or other ETFs that facilitate your passive approach to seeking financial freedom. Not a single path leads to a common goal.

Nevertheless, let me present three of the many choices I shared on Seeking Alpha. I took my own advice on each, so you can be sure I have my skin in the game.

Case #1 - Agree Realty

My first article on ADC aged pretty well:

Agree Realty Corporation: Elite-Level Business Metrics With Room To Further Outperform

Since then, the Company has delivered an outstanding total return of over 30%, significantly outperforming most REITs, even those operating within the same property sector. It even beat Realty Income, which is very well represented in VNQ. ADC also pays monthly dividends and operates as a triple net lease REIT oriented around retail/service properties, but it features higher portfolio quality and stronger business and credit metrics.

Agree Realty stands for just ~0.4% of VNQ's exposition.

Seeking Alpha

Case #2 - EPR Properties

This one is one of my all-time favourites regarding the REIT sector. The market has clearly overestimated the risk factors accompanying EPR, leaving their valuation multiple detached from their long-term ability to generate cash flows and a clear turn-around strategy. EPR was my debut article on Seeking Alpha:

EPR Properties: One Of The Best Risk-To-Reward Ratios In The Industry

Since then, the Company has delivered an attractive 14.6% total return and also enabled investors to secure a high 7-8% dividend yield.

EPR stands for just ~0.2% of VNQ's exposition.

Seeking Alpha

Case #3 - VICI Properties (VICI)

VICI Properties operates within a specific gaming niche, accompanied by unique value drivers. Its tenants have limited ability to switch locations or negotiate better deal terms, which ensures VICI's cash flow stability and predictability. It also supports their outstanding business metrics featuring a 100% occupancy rate and one of the highest (or the highest) WALTs in the REIT sector.

VICI is one of my largest REIT holdings. Since my coverage, the Company delivered a 19.8% total return, leaving below-average REITs far behind.

VICI Properties: Undervalued Despite Elite Business Metrics; I'm Buying.

Seeking Alpha

免责声明:投资有风险,本文并非投资建议,以上内容不应被视为任何金融产品的购买或出售要约、建议或邀请,作者或其他用户的任何相关讨论、评论或帖子也不应被视为此类内容。本文仅供一般参考,不考虑您的个人投资目标、财务状况或需求。TTM对信息的准确性和完整性不承担任何责任或保证,投资者应自行研究并在投资前寻求专业建议。

热议股票

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10