TAN: Trump Nor Harris Will Save Solar - It Is Up To Jerome Powell

Bilanol/iStock via Getty Images

Solar stocks surged Wednesday morning following the presidential debate between Kamala Harris and Donald Trump. The Invesco Solar ETF (NYSEARCA:TAN) rose by around 5%, with First Solar, Inc. (FSLR) leading at a ~11% gain. Other beaten-down companies like Canadian Solar Inc. (CSIQ) performed well, with a 16.7% return over the past five days. Enphase Energy, Inc. (ENPH) and SolarEdge Technologies, Inc. (SEDG) also gapped up significantly Wednesday morning, but as of Thursday morning, they are unchanged over the past week.

The solar industry arguably faces the most significant exposure to the 2024 election. While there is certainly debate regarding who "won" the debate, betting markets have sided with Harris. Trump's odds of winning, according to PolyMarket, declined from around 54% earlier this week to 49%. From the PredictIt market, Harris's odds rose from 51% to 55% from September 8th to the 11th. Though the debate did not give either a clear advantage, it did result in a slight but notable shift in favor of Kamala Harris, bringing the overall odds to about 50-50, with no clear leader.

Most see the Democratic candidate as pro-solar and anti-fossil fuels. In reality, it is not clear, as Harris has not provided definitive energy policies. Though her website's comments on energy policy are unclear, with a general focus on energy affordability and clean power, it seems likely that the focus will continue those seen in the Biden administration. This year, the Biden administration announced tariffs on Chinese solar products and tax credits for US clean energy companies.

Notably, Canadian Solar Inc. (CSIQ) (which, operationally, is a Chinese company) and roughly 16% of TAN's holdings are situated in China, meaning not all of the ETF may be positively exposed to the current administration's policies. Canadian Solar has run into trouble by trying to circumvent tariffs.

Although I would not say Harris' potential solar policies are as supportive for the industry as many may expect, such as in the Obama era, Trump's are probably not supportive. Most notably, his focus on ending the Inflation Reduction Act policies, which extended the solar tax credit. That said, Trump has said he is a "big fan" of solar, while also complaining about its land requirements.

Trump supports fossil fuel deregulation, which may indirectly hamper solar if natural gas or coal supply and demand increase. That said, the market may be overreacting to this news. Neither candidate has provided detailed policies that should significantly change the solar market. Instead, I argue TAN and its constituents are primarily impacted by interest rates, cyclical economic trends, and state-level policies, which are currently not supportive of the industry.

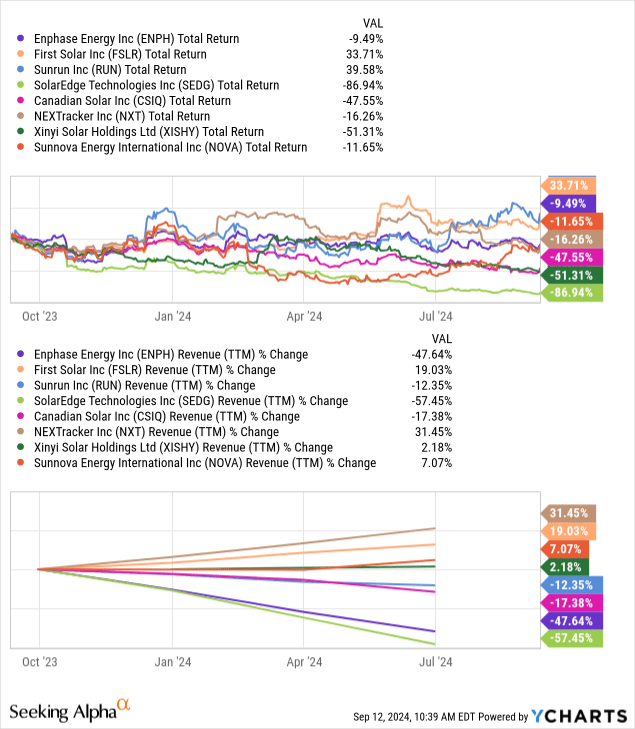

Solar Stocks Deliver Diverging Performance

This year, I've had a bearish outlook on most solar stocks. This is not because I don't believe in solar as an energy solution but because of the industry's poor economics. I became bearish on SolarEdge Technologies, Inc. (SEDG) in May, seeing the company losing its competitive position against Enphase Energy, Inc. (ENPH) amid the industry slowdown. SEDG has declined by 63% since then and 13.3% since I updated my outlook last month. More recently, SolarEdge's CEO stepped down, exacerbating investor concerns.

I also published a bearish article regarding Canadian Solar last year, with CSIQ losing 28% of its value since. I believe that the companies' significant presence in China gave US investors poor legal protection. Further, the company would face falling profits as the solar panel market fell into a glut amid falling demand and skyrocketing Chinese production. Those two stocks are in TAN, though they're no longer in the top 10 due to their falling market capitalization. Instead, more stable companies like Enphase, First Solar, and Sunrun Inc. (RUN) have seen their exposure rise.

TAN's performance over the past year has been poor, with a 28% loss YoY. The ETF has reversed most of its pandemic-era gains and is now back at its pre-2020 price level. Of course, its constituent exposure has changed dramatically, as it will usually buy top performers as their market capitalization increases and sell losers as they devalue, creating a potential "buy high sell low" flaw in the ETF, given many solar stocks have been range-bound.

Most of the top companies in TAN have declined over the past year, with most seeing significant declines in sales. See below:

This set includes the two solar companies I've covered recently, CSIQ and SEDG, which represent less than 3% of the fund. The others are TAN's top ten companies with reportable data in USD terms, as many are foreign companies.

First Solar and Nextracker Inc. (NXT) are the major leaders, having not seen their sales decline over the past year. Nextracker sells solar portfolio energy-tracking hardware and has had robust and resilient sales growth despite industry headwinds. First Solar is particularly unique because it is a US-based solar manufacturer and benefits significantly from the Inflation Reduction Act that has policies that benefit domestic manufacturing and tariffs on its cheaper overseas competitors. FSLR is the most negatively exposed to a Trump victory, if Trump plans on ending IRA solar provisions. Thus, it's up ~14% this week following the debate. I feel FSLR may be overvalued because I do not think it would be profitable in a freely competitive market, which China would typically dominate due to lower manufacturing costs. Regardless of who wins, it is also exposed to the solar panel glut issue.

Lower Rates May Alleviate The Solar Glut

Solar and wind are the best investments when interest rates are low, whereas fossil fuel power plants are better when interest rates are higher. This is because solar and wind have higher upfront costs, compounded when rates are high, whereas fossil fuel plants typically have lower upfront costs but higher labor overhead.

I did the math in my last SEDG article and found that residential solar, in a typical US state and home, would provide monthly savings only if one can borrow below 5%. For example, a $20K loan (accounting for the 30% Fed tax credit) with a 20-year maturity below 5% might have a payment of around $150, about the same as most homeowners pay for electricity (outside of California, etc.). However, now that solar loans are around 10%, there are no monthly savings from solar, limiting demand to those few people with significant excess spending power who want to help the environment today.

Obviously, the US residential market is just one aspect of TAN's total exposure. We should also include Europe and US utilities. However, when we look at key renewable utility companies like NextEra Energy Partners, LP (NEP), we can see a significant shift away from capital investments in solar due to higher interest rates. The European market appears similar; despite having more government support for solar, demand is faltering amid higher rates and weaker economic fundamentals.

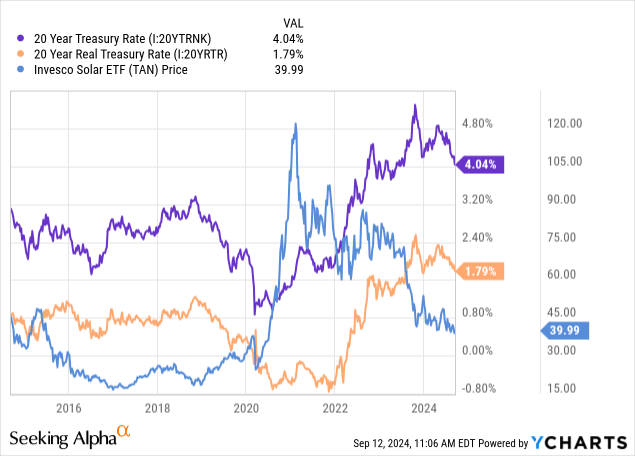

In my view, when thinking about solar, it is best to focus on interest rates because that will be the driving factor for both utilities and homeowners. Usually, these loans may be similar to the 20-year Treasury rate plus a spread of around 3% to 10%, depending on risk. I am not accounting for extremes, such as ultra-low rates in "buy down" solar loans with inflated loan amounts. Realistically, TAN may perform best when real interest rates, or rates adjusted for expected inflation, are below 0%. See below:

Monthly cost is a critical factor for solar, but utilities and homeowners will also likely consider expected increases in electricity prices. That will often correspond to inflation over a long period. Thus, the closer one can borrow to the expected inflation rate, the higher the long-term ROI of solar. As seen above, TAN rose dramatically when the 20-year real interest rate fell below zero in 2020, making solar a no-brainer investment for many.

However, solar companies have increased production since then to meet higher demand, while demand has declined due to much higher real interest rates. Production growth has been substantial in China, causing the US and Europe to face significant supply gluts in solar modules. The US saw a massive buildup of Chinese solar imports before the tariff waiver ended in June, which may alleviate the US glut. That said, without cheap solar imports from China, solar maybe even less economical. Many of the companies in TAN are Chinese, and even more are solar accessory companies like Enphase and Nextracker that sell hardware needed for solar, but not panels.

Thus, I'd argue that the tariffs benefit First Solar but hurt most of the others in TAN and should negatively impact the US market. If interest rates decline, higher import costs may make solar less feasible for years. Real rates are declining on long-term debt, but not fast enough to aid the market quickly. Additionally, homeowners may not be in the ideal financial environment to make significant home investments, even if they are economical, due to various recession signs in the consumer economy, seen in higher defaults.

The Bottom Line

TAN has a weighted-average "P/E" ratio of 521X TTM and potentially 21X forward, though I am uncertain how Invesco arrived at that estimate. Most of its holdings are unprofitable or at the cusp of profitability, which has been true throughout its history. Its SEC dividend yield is 73 bps, and its twelve-month distribution rate is 12 bps, indicating little to be found from dividends. The ETF's expense ratio is also moderate at 67 bps.

Investors and speculators interested in the political exposure with solar may want to keep an eye on First Solar. In my view, the company's profitability depends mainly on the US government's solar stimulus and anti-competitive efforts against Chinese imports. Both Trump and Harris seemingly favor solar tariffs (given Biden's record and Trump's on tariffs in general), but Trump may end policies that provide added stimulus.

In my view, their decisions regarding fossil fuels are unlikely to affect solar companies significantly. I highly doubt Kamala Harris will block fossil fuels to a degree that raises electricity costs so much that solar becomes more viable since Biden has not pursued that approach. Further, unless Trump can raise today's meager natural gas prices and relatively low oil prices, I do not expect oil and gas companies to boost production anytime soon. Regardless, electricity prices have more to do with labor costs for maintaining utility systems.

To me, Jerome Powell and Fed's interest rate decisions significantly impact solar stocks in TAN because they will ultimately drive solar cost savings. Rate cuts should benefit solar unless they coincide with a substantial economic recession that hampers solar demand (which may be likely). Rate cuts may also fail to benefit solar if solar panel prices rise due to higher import costs from tariffs. Overall, tariffs seem to be a net negative for most companies in TAN, and neither candidate appears opposed to solar tariffs.

For now, I am bearish on TAN and expect it and most of its constituents will decline due to ongoing weakness in solar demand in North America and Europe. Although TAN's price is back at pre-2020 levels, the ETF will often buy solar stocks in a "pump" phase and sell after a "dump" due to its market-cap weighting system. Thus, I think TAN systematically underperforms and would be much better using more of an equal-weight strategy. TAN may rise if either candidate proposes more supportive measures or if interest rates decline in a "soft landing" where a recession is avoided.

免责声明:投资有风险,本文并非投资建议,以上内容不应被视为任何金融产品的购买或出售要约、建议或邀请,作者或其他用户的任何相关讨论、评论或帖子也不应被视为此类内容。本文仅供一般参考,不考虑您的个人投资目标、财务状况或需求。TTM对信息的准确性和完整性不承担任何责任或保证,投资者应自行研究并在投资前寻求专业建议。

热议股票

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10