Most Shareholders Will Probably Agree With Australian Foundation Investment Company Limited's (ASX:AFI) CEO Compensation

Key Insights

- Australian Foundation Investment's Annual General Meeting to take place on 3rd of October

- Total pay for CEO Robert Freeman includes AU$913.5k salary

- Total compensation is 57% below industry average

- Over the past three years, Australian Foundation Investment's EPS grew by 6.9% and over the past three years, the total loss to shareholders 1.4%

The performance at Australian Foundation Investment Company Limited (ASX:AFI) has been rather lacklustre of late and shareholders may be wondering what CEO Robert Freeman is planning to do about this. They will get a chance to exercise their voting power to influence the future direction of the company in the next AGM on 3rd of October. It has been shown that setting appropriate executive remuneration incentivises the management to act in the interests of shareholders. We think CEO compensation looks appropriate given the data we have put together.

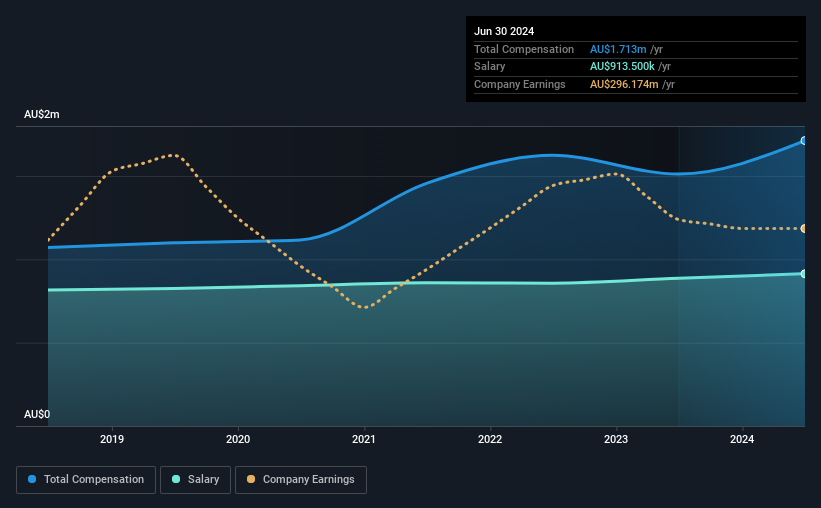

Check out our latest analysis for Australian Foundation Investment

How Does Total Compensation For Robert Freeman Compare With Other Companies In The Industry?

Our data indicates that Australian Foundation Investment Company Limited has a market capitalization of AU$9.4b, and total annual CEO compensation was reported as AU$1.7m for the year to June 2024. That's a notable increase of 13% on last year. We note that the salary of AU$913.5k makes up a sizeable portion of the total compensation received by the CEO.

In comparison with other companies in the Australian Capital Markets industry with market capitalizations ranging from AU$5.8b to AU$17b, the reported median CEO total compensation was AU$4.0m. That is to say, Robert Freeman is paid under the industry median. What's more, Robert Freeman holds AU$1.5m worth of shares in the company in their own name.

| Component | 2024 | 2023 | Proportion (2024) |

| Salary | AU$914k | AU$886k | 53% |

| Other | AU$799k | AU$626k | 47% |

| Total Compensation | AU$1.7m | AU$1.5m | 100% |

On an industry level, around 56% of total compensation represents salary and 44% is other remuneration. There isn't a significant difference between Australian Foundation Investment and the broader market, in terms of salary allocation in the overall compensation package. If salary is the major component in total compensation, it suggests that the CEO receives a higher fixed proportion of the total compensation, regardless of performance.

A Look at Australian Foundation Investment Company Limited's Growth Numbers

Over the past three years, Australian Foundation Investment Company Limited has seen its earnings per share (EPS) grow by 6.9% per year. It saw its revenue drop 3.1% over the last year.

We would prefer it if there was revenue growth, but the modest improvement in EPS is good. These two metrics are moving in different directions, so while it's hard to be confident judging performance, we think the stock is worth watching. While we don't have analyst forecasts for the company, shareholders might want to examine this detailed historical graph of earnings, revenue and cash flow.

Has Australian Foundation Investment Company Limited Been A Good Investment?

Since shareholders would have lost about 1.4% over three years, some Australian Foundation Investment Company Limited investors would surely be feeling negative emotions. So shareholders would probably want the company to be less generous with CEO compensation.

In Summary...

The lack lustre share price performance may have something to do with the flat earnings growth. In the upcoming AGM, shareholders will get the opportunity to discuss any concerns with the board and assess if the board's plan is likely to improve company performance.

While CEO pay is an important factor to be aware of, there are other areas that investors should be mindful of as well. We've identified 1 warning sign for Australian Foundation Investment that investors should be aware of in a dynamic business environment.

Important note: Australian Foundation Investment is an exciting stock, but we understand investors may be looking for an unencumbered balance sheet and blockbuster returns. You might find something better in this list of interesting companies with high ROE and low debt.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency• Be alerted to new Warning Signs or Risks via email or mobile• Track the Fair Value of your stocks

Try a Demo Portfolio for FreeHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

免责声明:投资有风险,本文并非投资建议,以上内容不应被视为任何金融产品的购买或出售要约、建议或邀请,作者或其他用户的任何相关讨论、评论或帖子也不应被视为此类内容。本文仅供一般参考,不考虑您的个人投资目标、财务状况或需求。TTM对信息的准确性和完整性不承担任何责任或保证,投资者应自行研究并在投资前寻求专业建议。

热议股票

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10