SGX Stocks That May Be Priced Below Intrinsic Value In October 2024

As of October 2024, the Singapore market has been navigating a period of cautious optimism, with investors closely monitoring economic indicators and global financial trends. In this environment, identifying stocks that may be priced below their intrinsic value can offer potential opportunities for investors seeking to capitalize on market inefficiencies.

Top 5 Undervalued Stocks Based On Cash Flows In Singapore

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Singapore Technologies Engineering (SGX:S63) | SGD4.70 | SGD7.29 | 35.5% |

| Digital Core REIT (SGX:DCRU) | US$0.585 | US$0.82 | 28.7% |

| Frasers Logistics & Commercial Trust (SGX:BUOU) | SGD1.11 | SGD1.99 | 44.2% |

| Nanofilm Technologies International (SGX:MZH) | SGD0.825 | SGD1.43 | 42.1% |

| Seatrium (SGX:5E2) | SGD1.97 | SGD3.03 | 35.1% |

Click here to see the full list of 5 stocks from our Undervalued SGX Stocks Based On Cash Flows screener.

Below we spotlight a couple of our favorites from our exclusive screener.

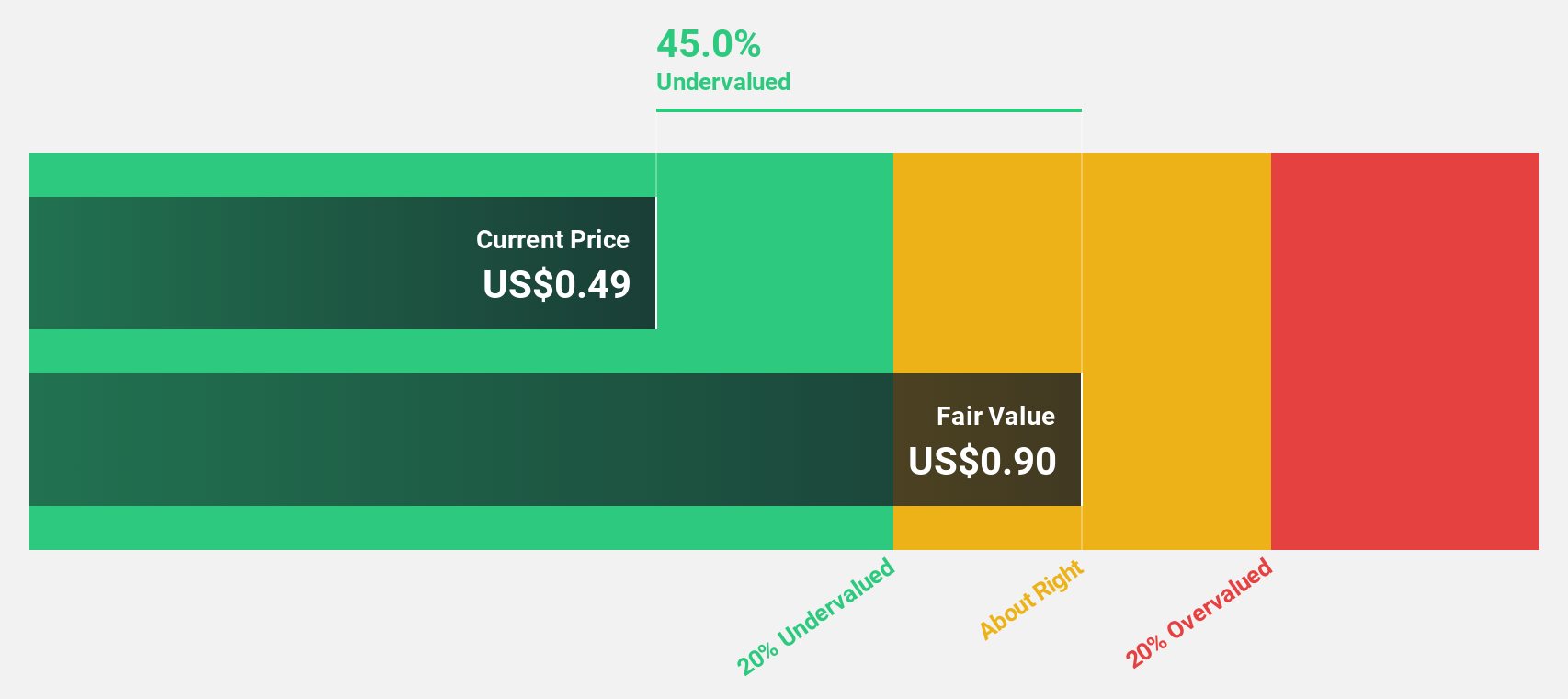

Digital Core REIT (SGX:DCRU)

Overview: Digital Core REIT (SGX: DCRU) is a Singapore-listed pure-play data centre real estate investment trust sponsored by Digital Realty, with a market cap of $759.55 million.

Operations: The company generates revenue primarily through its commercial real estate investment trust (REIT) segment, amounting to $70.76 million.

Estimated Discount To Fair Value: 28.7%

Digital Core REIT is trading at a significant discount to its estimated fair value of US$0.82, currently priced at US$0.59, which suggests potential undervaluation based on discounted cash flow analysis. Despite recent shareholder dilution and an unstable dividend track record, the REIT's earnings are projected to grow significantly by 96.09% annually, with revenue expected to increase by 12% per year—outpacing the Singapore market's growth rate. Recent financial results showed improved net income despite declining sales and revenue figures year-over-year.

- Insights from our recent growth report point to a promising forecast for Digital Core REIT's business outlook.

- Click to explore a detailed breakdown of our findings in Digital Core REIT's balance sheet health report.

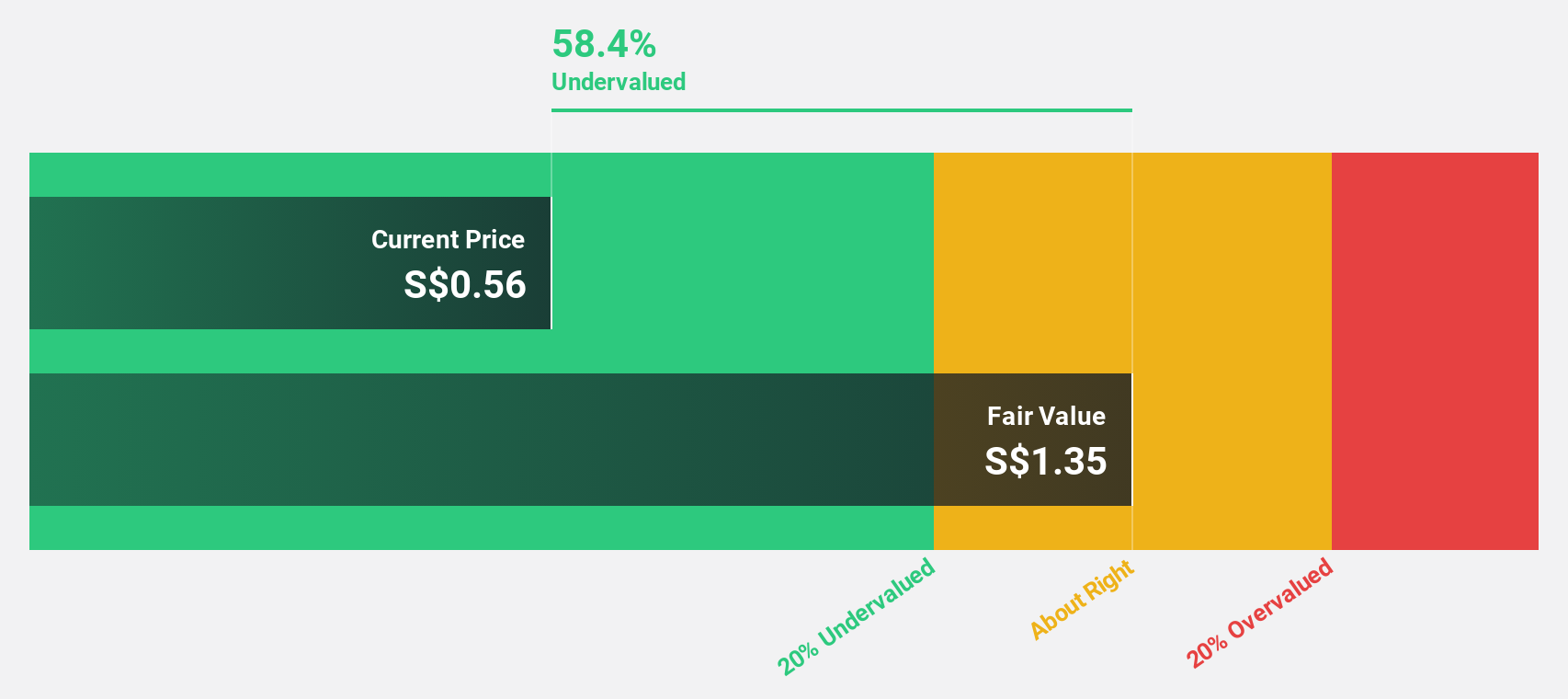

Nanofilm Technologies International (SGX:MZH)

Overview: Nanofilm Technologies International Limited, with a market cap of SGD537.14 million, offers nanotechnology solutions across Singapore, China, Japan, and Vietnam through its subsidiaries.

Operations: The company's revenue is derived from several segments, including Advanced Materials (SGD153.32 million), Industrial Equipment (SGD28.71 million), Nanofabrication (SGD18.37 million), and Sydrogen (SGD1.40 million).

Estimated Discount To Fair Value: 42.1%

Nanofilm Technologies International is trading at a substantial discount, with its current price of SGD 0.83 below the estimated fair value of SGD 1.43, highlighting potential undervaluation based on discounted cash flow analysis. Despite a net loss in the first half of 2024 and lower profit margins compared to last year, revenue growth forecasts exceed market averages at 16.1% annually, and earnings are expected to grow significantly by nearly 54% per year over the next three years.

- Our expertly prepared growth report on Nanofilm Technologies International implies its future financial outlook may be stronger than recent results.

- Click here to discover the nuances of Nanofilm Technologies International with our detailed financial health report.

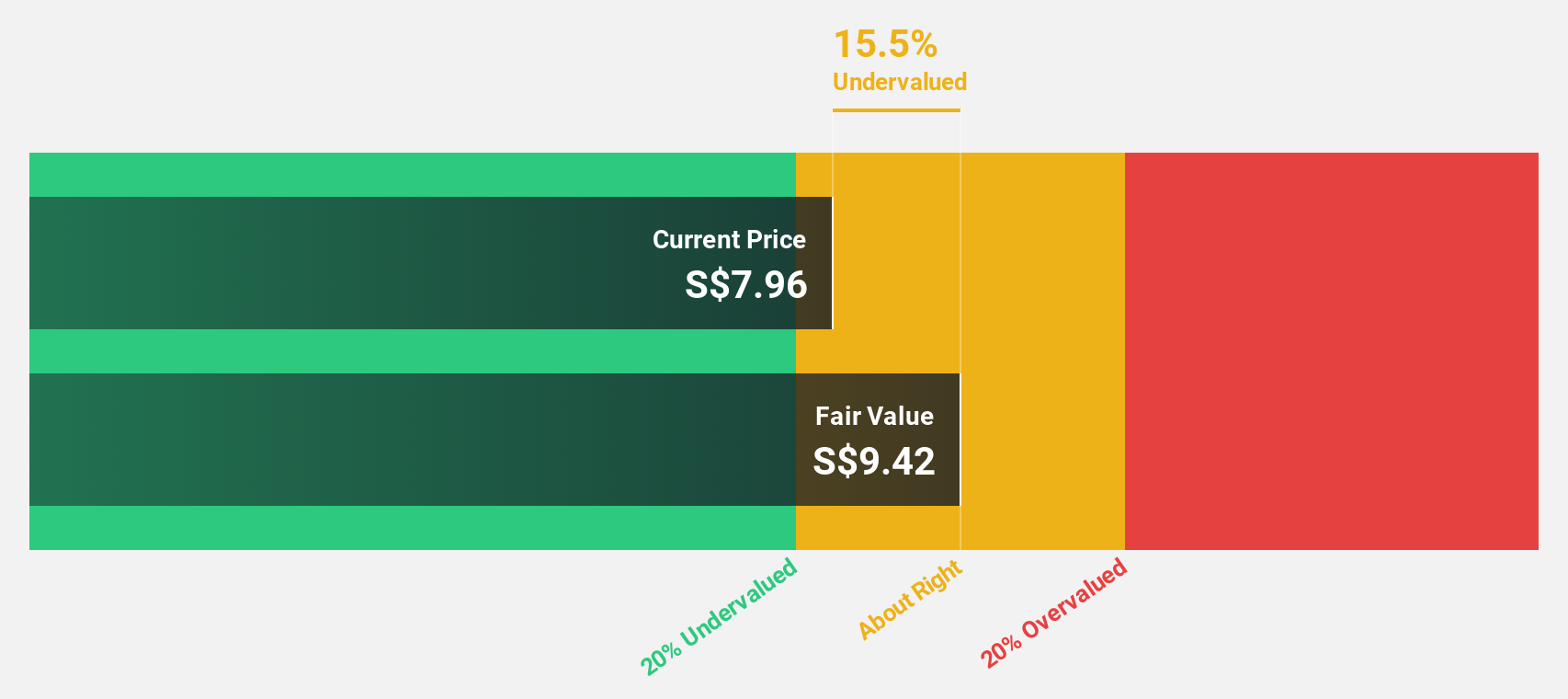

Singapore Technologies Engineering (SGX:S63)

Overview: Singapore Technologies Engineering Ltd is a global technology, defence, and engineering company with a market cap of SGD14.65 billion.

Operations: The company's revenue is primarily derived from its Defence & Public Security segment at SGD4.54 billion, followed by Commercial Aerospace at SGD4.34 billion, and Urban Solutions & Satcom at SGD2.01 billion.

Estimated Discount To Fair Value: 35.5%

Singapore Technologies Engineering is trading at a significant discount, with its current price of SGD 4.70 below the estimated fair value of SGD 7.29, suggesting undervaluation based on discounted cash flow analysis. Recent earnings for the half year show sales increasing to SGD 5.52 billion and net income rising to SGD 336.53 million, reflecting strong financial performance. However, debt coverage by operating cash flow remains a concern despite forecasted revenue growth surpassing market averages at 6.4% annually.

- According our earnings growth report, there's an indication that Singapore Technologies Engineering might be ready to expand.

- Click here and access our complete balance sheet health report to understand the dynamics of Singapore Technologies Engineering.

Turning Ideas Into Actions

- Click through to start exploring the rest of the 2 Undervalued SGX Stocks Based On Cash Flows now.

- Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

- Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Nanofilm Technologies International might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

免责声明:投资有风险,本文并非投资建议,以上内容不应被视为任何金融产品的购买或出售要约、建议或邀请,作者或其他用户的任何相关讨论、评论或帖子也不应被视为此类内容。本文仅供一般参考,不考虑您的个人投资目标、财务状况或需求。TTM对信息的准确性和完整性不承担任何责任或保证,投资者应自行研究并在投资前寻求专业建议。

热议股票

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10