Can Stockland (ASX:SGP) Performance Keep Up Given Its Mixed Bag Of Fundamentals?

Stockland's (ASX:SGP) stock is up by 6.5% over the past three months. However, the company's financials look a bit inconsistent and market outcomes are ultimately driven by long-term fundamentals, meaning that the stock could head in either direction. Specifically, we decided to study Stockland's ROE in this article.

Return on Equity or ROE is a test of how effectively a company is growing its value and managing investors’ money. In simpler terms, it measures the profitability of a company in relation to shareholder's equity.

View our latest analysis for Stockland

How Is ROE Calculated?

Return on equity can be calculated by using the formula:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Stockland is:

3.1% = AU$305m ÷ AU$9.9b (Based on the trailing twelve months to June 2024).

The 'return' is the profit over the last twelve months. Another way to think of that is that for every A$1 worth of equity, the company was able to earn A$0.03 in profit.

What Is The Relationship Between ROE And Earnings Growth?

We have already established that ROE serves as an efficient profit-generating gauge for a company's future earnings. We now need to evaluate how much profit the company reinvests or "retains" for future growth which then gives us an idea about the growth potential of the company. Generally speaking, other things being equal, firms with a high return on equity and profit retention, have a higher growth rate than firms that don’t share these attributes.

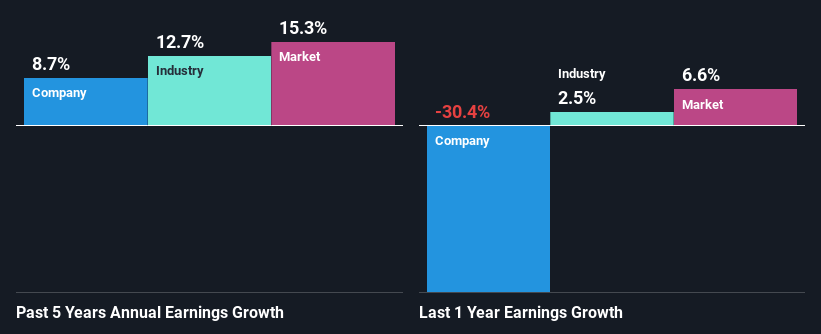

A Side By Side comparison of Stockland's Earnings Growth And 3.1% ROE

As you can see, Stockland's ROE looks pretty weak. Not just that, even compared to the industry average of 6.9%, the company's ROE is entirely unremarkable. Stockland was still able to see a decent net income growth of 8.7% over the past five years. We reckon that there could be other factors at play here. Such as - high earnings retention or an efficient management in place.

Next, on comparing with the industry net income growth, we found that Stockland's reported growth was lower than the industry growth of 13% over the last few years, which is not something we like to see.

Earnings growth is an important metric to consider when valuing a stock. The investor should try to establish if the expected growth or decline in earnings, whichever the case may be, is priced in. By doing so, they will have an idea if the stock is headed into clear blue waters or if swampy waters await. Is SGP fairly valued? This infographic on the company's intrinsic value has everything you need to know.

Is Stockland Making Efficient Use Of Its Profits?

Stockland seems to be paying out most of its income as dividends judging by its three-year median payout ratio of 74%, meaning the company retains only 26% of its income. However, this is typical for REITs as they are often required by law to distribute most of their earnings. Despite this, the company's earnings grew moderately as we saw above.

Additionally, Stockland has paid dividends over a period of at least ten years which means that the company is pretty serious about sharing its profits with shareholders. Our latest analyst data shows that the future payout ratio of the company over the next three years is expected to be approximately 75%. Regardless, the future ROE for Stockland is predicted to rise to 8.7% despite there being not much change expected in its payout ratio.

Conclusion

In total, we're a bit ambivalent about Stockland's performance. While no doubt its earnings growth is pretty respectable, the low profit retention could mean that the company's earnings growth could have been higher, had it been paying reinvesting a higher portion of its profits. An improvement in its ROE could also help future earnings growth. With that said, the latest industry analyst forecasts reveal that the company's earnings are expected to accelerate. Are these analysts expectations based on the broad expectations for the industry, or on the company's fundamentals? Click here to be taken to our analyst's forecasts page for the company.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency• Be alerted to new Warning Signs or Risks via email or mobile• Track the Fair Value of your stocks

Try a Demo Portfolio for FreeHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

免责声明:投资有风险,本文并非投资建议,以上内容不应被视为任何金融产品的购买或出售要约、建议或邀请,作者或其他用户的任何相关讨论、评论或帖子也不应被视为此类内容。本文仅供一般参考,不考虑您的个人投资目标、财务状况或需求。TTM对信息的准确性和完整性不承担任何责任或保证,投资者应自行研究并在投资前寻求专业建议。

热议股票

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10