Have Insiders Sold HITIQ Shares Recently?

We note that a HITIQ Limited (ASX:HIQ) insider, Otto Buttula, recently sold AU$156k worth of stock for AU$0.032 per share. It might not be a huge sale, but it did reduce their holding size 24%, hardly encouraging.

See our latest analysis for HITIQ

The Last 12 Months Of Insider Transactions At HITIQ

In fact, the recent sale by Otto Buttula was the biggest sale of HITIQ shares made by an insider individual in the last twelve months, according to our records. That means that an insider was selling shares at slightly below the current price (AU$0.048). As a general rule we consider it to be discouraging when insiders are selling below the current price, because it suggests they were happy with a lower valuation. While insider selling is not a positive sign, we can't be sure if it does mean insiders think the shares are fully valued, so it's only a weak sign. This single sale was just 24% of Otto Buttula's stake.

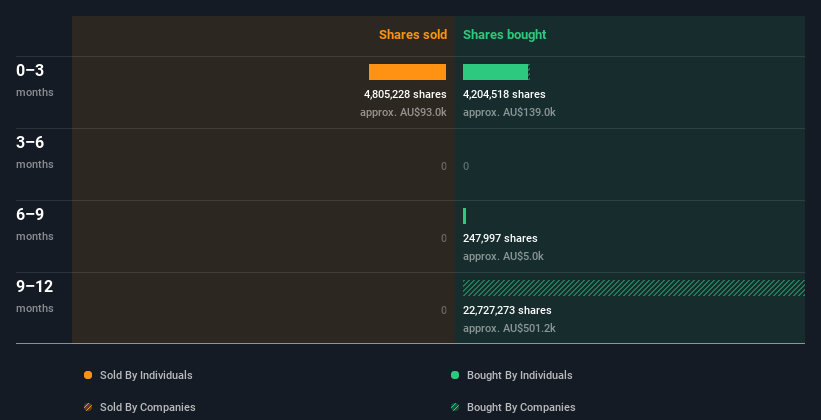

Over the last year, we can see that insiders have bought 4.31m shares worth AU$126k. But insiders sold 4.81m shares worth AU$156k. You can see the insider transactions (by companies and individuals) over the last year depicted in the chart below. By clicking on the graph below, you can see the precise details of each insider transaction!

For those who like to find hidden gems this free list of small cap companies with recent insider purchasing, could be just the ticket.

Insider Ownership Of HITIQ

I like to look at how many shares insiders own in a company, to help inform my view of how aligned they are with insiders. A high insider ownership often makes company leadership more mindful of shareholder interests. Insiders own 20% of HITIQ shares, worth about AU$3.4m. While this is a strong but not outstanding level of insider ownership, it's enough to indicate some alignment between management and smaller shareholders.

So What Does This Data Suggest About HITIQ Insiders?

Our data shows a little more insider selling than buying in the last three months. But the net divestment is not enough to concern us at all. We're a little cautious about the insider selling at HITIQ. But it's good to see that insiders own shares in the company. So these insider transactions can help us build a thesis about the stock, but it's also worthwhile knowing the risks facing this company. Be aware that HITIQ is showing 8 warning signs in our investment analysis, and 4 of those are a bit concerning...

But note: HITIQ may not be the best stock to buy. So take a peek at this free list of interesting companies with high ROE and low debt.

For the purposes of this article, insiders are those individuals who report their transactions to the relevant regulatory body. We currently account for open market transactions and private dispositions of direct interests only, but not derivative transactions or indirect interests.

Valuation is complex, but we're here to simplify it.

Discover if HITIQ might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

免责声明:投资有风险,本文并非投资建议,以上内容不应被视为任何金融产品的购买或出售要约、建议或邀请,作者或其他用户的任何相关讨论、评论或帖子也不应被视为此类内容。本文仅供一般参考,不考虑您的个人投资目标、财务状况或需求。TTM对信息的准确性和完整性不承担任何责任或保证,投资者应自行研究并在投资前寻求专业建议。

热议股票

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10