KeyCorp (NYSE:KEY) Has Announced A Dividend Of $0.205

KeyCorp (NYSE:KEY) will pay a dividend of $0.205 on the 14th of March. This makes the dividend yield 4.5%, which will augment investor returns quite nicely.

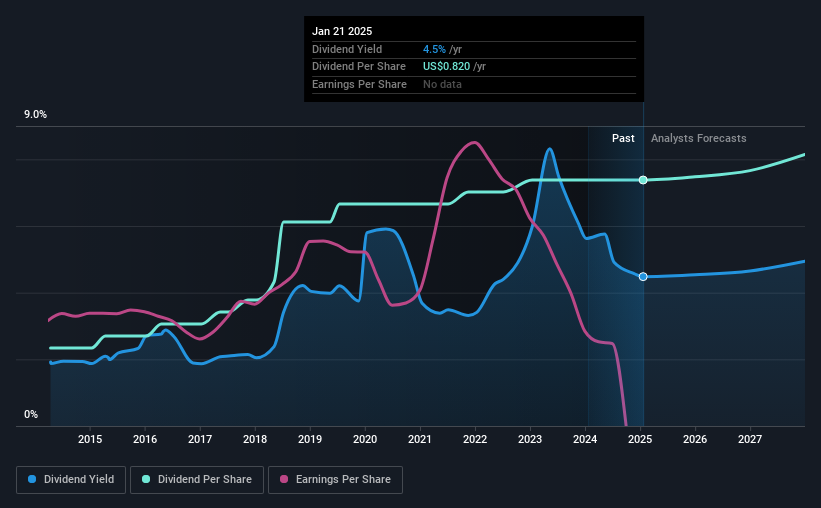

See our latest analysis for KeyCorp

KeyCorp's Earnings Will Easily Cover The Distributions

We like to see robust dividend yields, but that doesn't matter if the payment isn't sustainable.

KeyCorp has a long history of paying out dividends, with its current track record at a minimum of 10 years. Despite this history however, the company's latest earnings report actually shows that it didn't have enough earnings to cover its dividends. This is very worrying for shareholders, as this shows that KeyCorp will not be able to sustain its dividend at its current rate.

According to analysts, EPS should be several times higher in the next 3 years. They also estimate that the future payout ratio could reach 50% in the same time horizon, which is in a comfortable range for us.

KeyCorp Has A Solid Track Record

The company has a sustained record of paying dividends with very little fluctuation. Since 2015, the annual payment back then was $0.26, compared to the most recent full-year payment of $0.82. This implies that the company grew its distributions at a yearly rate of about 12% over that duration. We can see that payments have shown some very nice upward momentum without faltering, which provides some reassurance that future payments will also be reliable.

Dividend Growth Potential Is Shaky

The company's investors will be pleased to have been receiving dividend income for some time. However, things aren't all that rosy. Earnings per share has been sinking by 72% over the last five years. Such rapid declines definitely have the potential to constrain dividend payments if the trend continues into the future. However, the next year is actually looking up, with earnings set to rise. We would just wait until it becomes a pattern before getting too excited.

We should note that KeyCorp has issued stock equal to 18% of shares outstanding. Regularly doing this can be detrimental - it's hard to grow dividends per share when new shares are regularly being created.

In Summary

Overall, we don't think this company makes a great dividend stock, even though the dividend wasn't cut this year. We can't deny that the payments have been very stable, but we are a little bit worried about the very high payout ratio. We would be a touch cautious of relying on this stock primarily for the dividend income.

Companies possessing a stable dividend policy will likely enjoy greater investor interest than those suffering from a more inconsistent approach. Still, investors need to consider a host of other factors, apart from dividend payments, when analysing a company. Taking the debate a bit further, we've identified 4 warning signs for KeyCorp that investors need to be conscious of moving forward. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

Valuation is complex, but we're here to simplify it.

Discover if KeyCorp might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

免责声明:投资有风险,本文并非投资建议,以上内容不应被视为任何金融产品的购买或出售要约、建议或邀请,作者或其他用户的任何相关讨论、评论或帖子也不应被视为此类内容。本文仅供一般参考,不考虑您的个人投资目标、财务状况或需求。TTM对信息的准确性和完整性不承担任何责任或保证,投资者应自行研究并在投资前寻求专业建议。

热议股票

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10