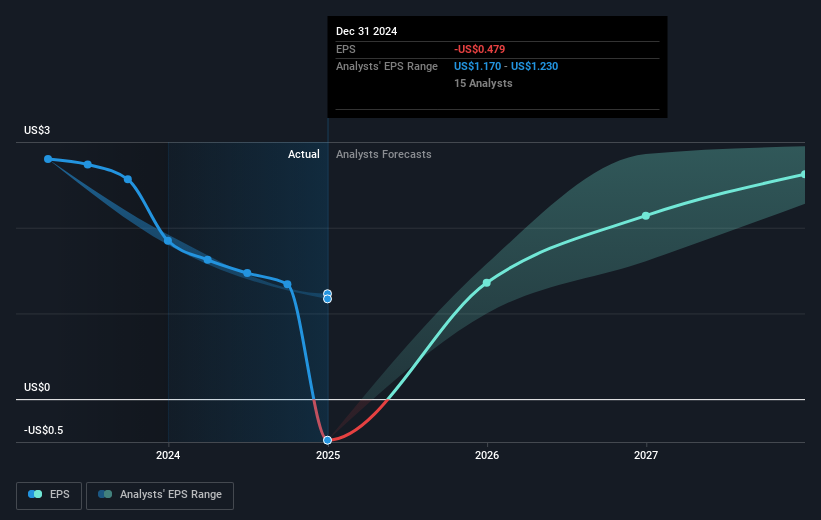

GlobalFoundries (NasdaqGS:GFS) Stock Sheds 2% After 2024 Net Loss Of US$265 Million

GlobalFoundries (NasdaqGS:GFS) recently announced a disappointing financial performance for 2024, posting a net loss of $265 million and a drop in sales to $6.75 billion. The announcement of a $935 million impairment charge to realign its manufacturing strategy coincided with leadership changes, including the appointment of Tim Breen as the incoming CEO. Against a broader market backdrop of declines, with the market falling 3.9% over the past month, GlobalFoundries' share price movement of 2.47% appears consistent with trends. Despite optimistic guidance for Q1 2025, including expected net revenue of up to $1.6 billion, and the potential benefits from executive reshuffling, investor sentiment seems cautious amid uncertain economic conditions. Broader market concerns affecting tech stocks could have also influenced GFS's performance, with significant external financial results, like Nvidia's, holding sway over tech-oriented investor decisions.

See the full analysis report here for a deeper understanding of GlobalFoundries.

GlobalFoundries (GFS) experienced a total return decline of 24.04% over the past year. This performance falls short compared to the broader US market, which saw a return of 17.8%, and the US Semiconductor industry, which realized a 31.3% return. Several factors may have influenced this performance. The significant $935 million impairment charge announced on February 11, 2025, addressed legacy investments but impacted investor confidence. Additionally, the downward trend in sales from US$7.39 billion in 2023 to US$6.75 billion in 2024 reflected revenue pressures.

Furthermore, on January 17, 2025, GlobalFoundries announced a US$575 million investment in a new facility, aimed at bolstering U.S. semiconductor capabilities. While the collaboration with BAE Systems in June 2024 suggested potential for innovation, the broader financial performance, coupled with leadership transitions, likely contributed to the cautious investor outlook over the analyzing period. These events underscored challenges and strategic shifts within the company, impacting its long-term shareholder returns.

- Get the full picture of GlobalFoundries' valuation metrics and investment prospects—click to explore.

- Analyze the downside risks for GlobalFoundries and understand their potential impact—click to learn more.

- Is GlobalFoundries part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency• Be alerted to new Warning Signs or Risks via email or mobile• Track the Fair Value of your stocks

Try a Demo Portfolio for FreeHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

免责声明:投资有风险,本文并非投资建议,以上内容不应被视为任何金融产品的购买或出售要约、建议或邀请,作者或其他用户的任何相关讨论、评论或帖子也不应被视为此类内容。本文仅供一般参考,不考虑您的个人投资目标、财务状况或需求。TTM对信息的准确性和完整性不承担任何责任或保证,投资者应自行研究并在投资前寻求专业建议。

热议股票

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10