Singapore’s leading banks DBS Group (SGX: D05), OCBC Ltd (SGX: O39), and United Overseas Bank Ltd (SGX: U11) have delivered another year of record earnings and increased dividends.

However, with share prices hovering near or at all-time highs, is it still a good time to invest?

To answer this, we need to weigh the potential rewards against the inherent risks.

Why it might not be too late to invest

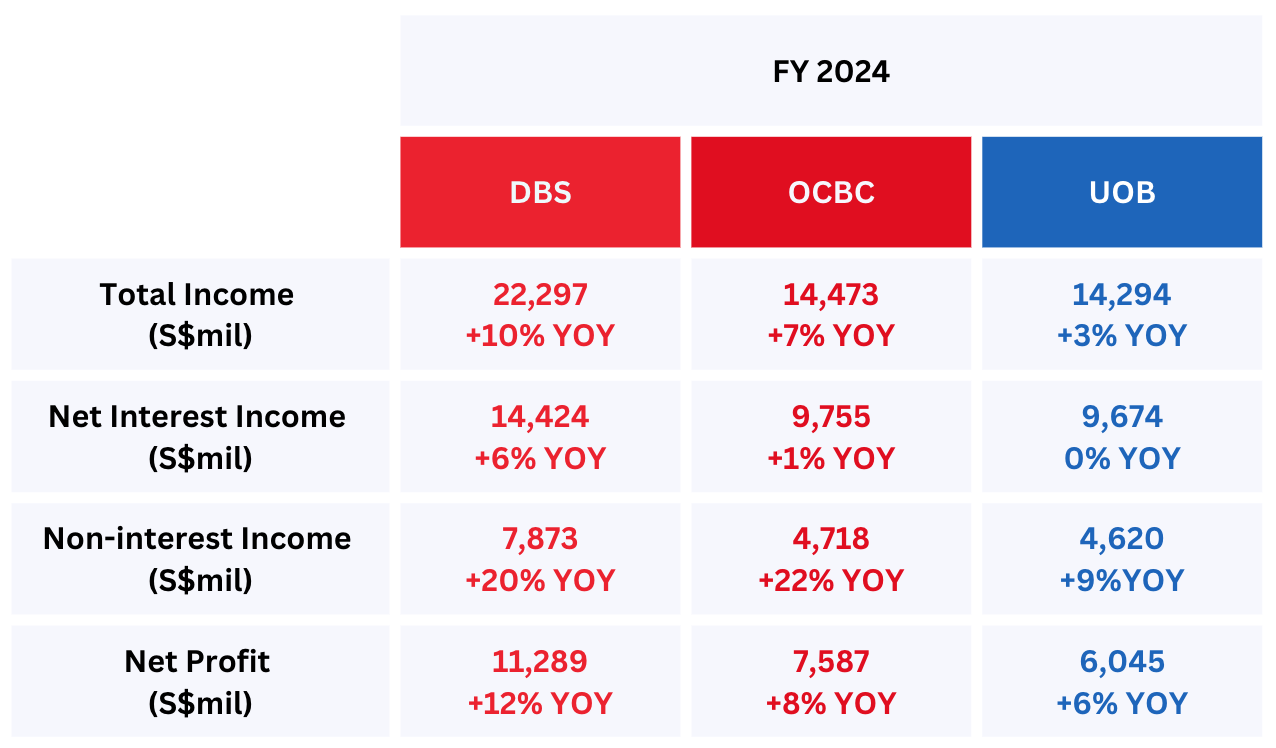

Source: DBS, OCBC, UOB FY 2024 results, compiled by the author

The banks’ continued growth offers a compelling argument for investment.

Even with US interest rates unchanged for much of 2024, the trio has demonstrated remarkable resilience, maintaining robust net interest income.

This strength is further amplified by a significant surge in non-interest income, particularly evident in DBS and OCBC, highlighting their diversified revenue streams.

Furthermore, despite the Fed’s one percentage point rate cut since last September, the banks’ growth has not faltered.

Indeed, during Q4 2024, DBS, OCBC, and UOB each reported strong year-on-year (YOY) net profit growth of 10%, 4%, and 9%, respectively.

Looking forward, the banks remain optimistic about expanding their loan books and non-interest income in FY 2025.

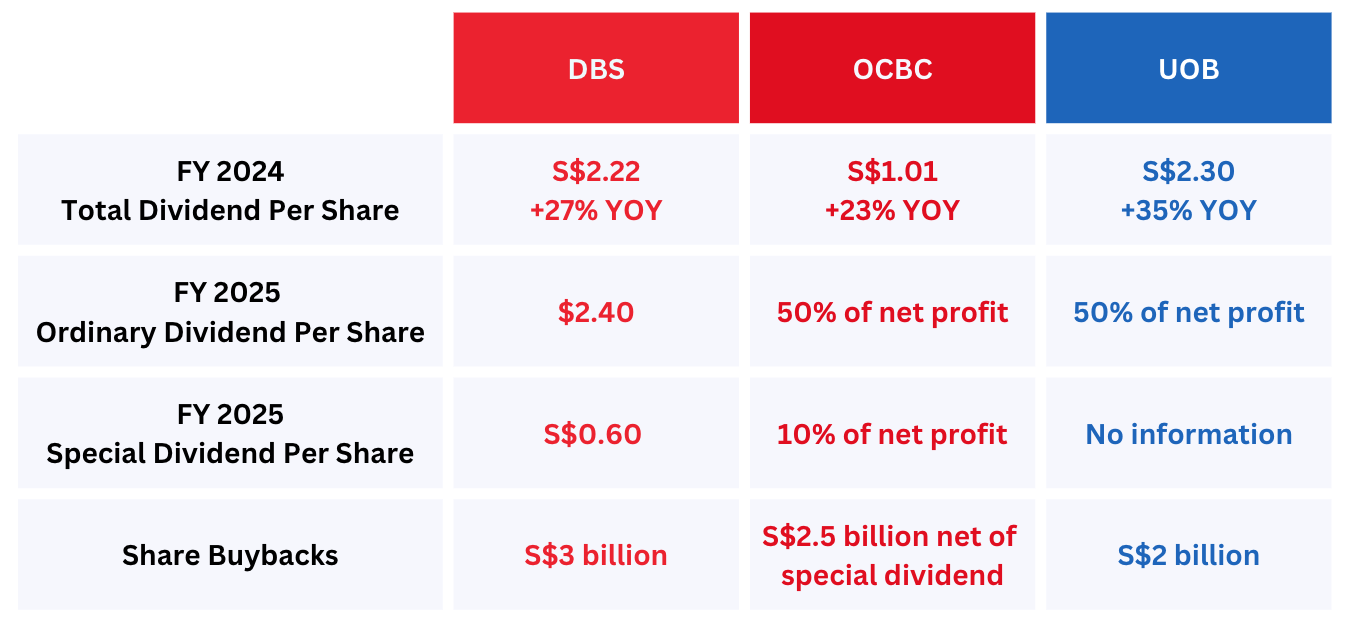

Source: DBS, OCBC, UOB FY 2024 results, compiled by the author

The banks’ strong financial results, coupled with capital management driven by Basel III, have led to notable dividend increases.

The FY 2024 total dividend figures, as shown in the table, reflected these special distributions, with significant YOY growth across all three banks.

In addition to these dividend payouts, the banks are also undertaking substantial share buybacks and outlining future dividend plans for FY 2025.

This proactive approach to capital return contributes to the attractive dividend yields of approximately 6% for all three stocks, despite the elevated share prices.

Reasons to proceed with caution

So, what have we learned so far?

The banks’ robust performances are undeniable, and their immediate outlooks remain positive in spite of rising geopolitical complexities.

Is there anything to worry about, though?

In my view, it’s crucial to acknowledge several key factors that can quickly change the bank’s’ outlook.

For instance, a sudden and significant drop in interest rates would directly impact net interest income, potentially leading to reduced profits and subsequent dividend reductions.

Furthermore, the substantial appreciation of share prices over the past year has resulted in elevated valuations, meaning these stocks are no longer screaming buys.

Consequently, this increased valuation risk makes them highly susceptible to even minor negative news, which could trigger a swift shift in market sentiment and a subsequent decline in share prices.

Get Smart: Look beyond the current year

Given the inherent unpredictability of short-term market fluctuations, the decision to invest in Singapore’s banks ultimately hinges on your long-term conviction in their business models.

If you believe the banks possess the capability and capacity to scale operations and achieve sustained growth over the next five to 10 years, then the current price may indeed represent a favourable entry point relative to their potential future value.

Beyond your long-term conviction, it’s prudent to assess your portfolio’s existing exposure to the banks.

If it is already heavily weighted towards bank stocks, you might just want to maintain existing positions and capitalise on the high dividend yields.

For those with minimal exposure, building positions in tranches over the coming years, could offer a balanced strategy to navigate potential market volatility, while capitalising on the banks’ long-term growth potential.

Which SGX companies will reach S$100 billion next? Our latest FREE report provides detailed financial analysis and growth prospects of 5 potential candidates. The results? Surprising. You’ll want to grab a copy now and see whether what everyone else says is true. Click here to download now.

Follow us on Facebook and Telegram for the latest investing news and analyses!

Disclosure: Chan Kin Chuah owns shares of DBS, OCBC and UOB.